American Axle’s Credit Rating Driven 5 Notches Too Low, While Equity Markets Foresee Declines

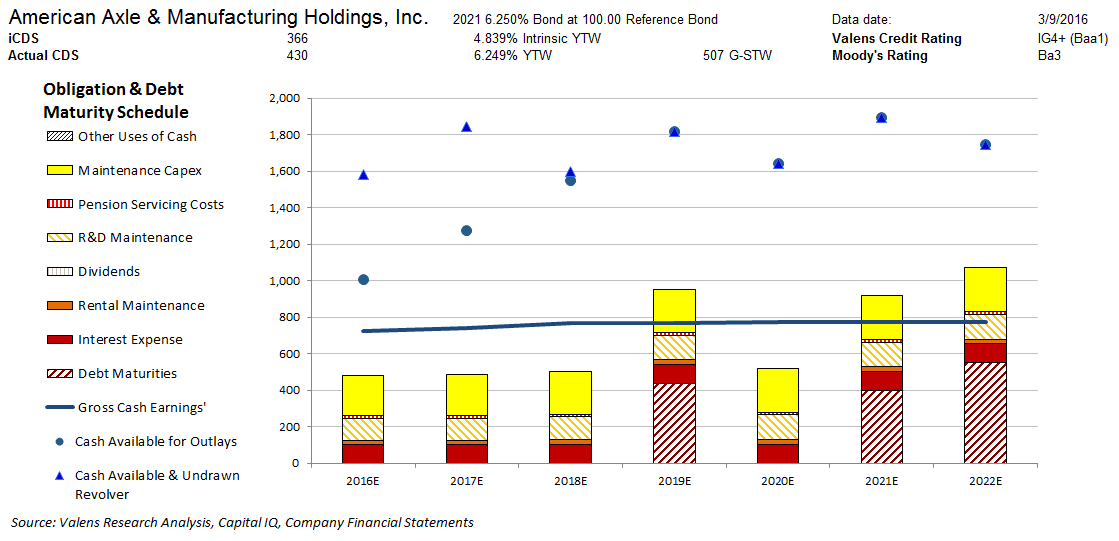

Moody’s is materially overstating the credit risk of American Axle & Manufacturing Holdings, Inc. (NYSE:AXL) with its Ba3 rating. However, Valens’ fundamental analysis highlights a much safer credit profile for AXL. The company’s cash flows easily cover all their operating obligations. Moreover, their sizable cash build should allow them to service all obligations including debt maturities in years when their cash flows fall short. Valens therefore rates AXL five notches higher at an IG4+ credit rating, or a Baa1 equivalent using Moody’s ratings scale.

In addition, cash bond markets are overstating AXL’s credit risk, with a cash bond YTW of 6.249% relative to an Intrinsic YTW of only 4.839%. Meanwhile, CDS markets are slightly overstating credit risk, with a CDS of 430bps versus an Intrinsic CDS of 366bps.

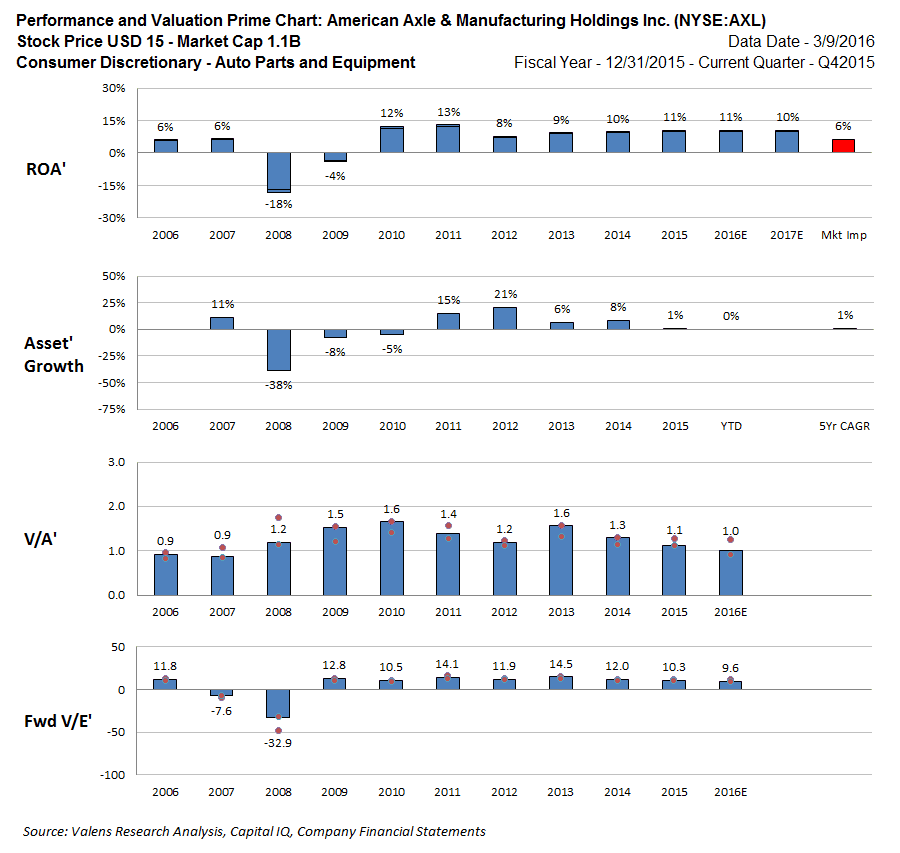

Equity markets share the bearish disposition of credit markets, with AXL trading at a 9.6x V/E’ and a 1.0x V/A’, both at the lower end of historical valuations. The market is expecting ROA’ to decrease to 6% levels, with Asset’ growth remaining at a subdued 1% a year going forward, as AXL grows at their slowest rate since their shrinkage in 2008-2010. Market expectation is lower than current consensus estimates that forecast ROA’ to maintain 10%-11% levels. Muted market expectations indicate that there could be equity upside if the company successfully delivers on consensus estimates or does not see profitability fade to levels not seen since before 2010.

Click here to read the article in its entirety at Seeking Alpha.