Good News: The New York Times’ Credit Is Investment Grade, While Equity Markets Warrant Muted Expectations

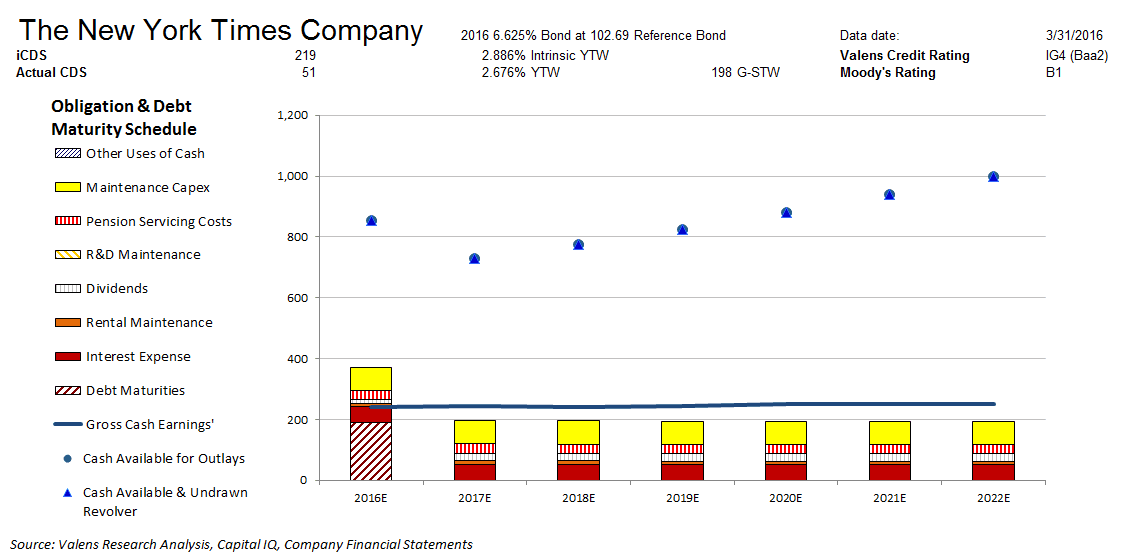

Moody’s is materially overstating the credit risk of The New York Times Company (NYSE:NYT) with its B1 rating. Our fundamental analysis highlights a much safer credit profile for NYT, whose stable cash flows cover all their obligations including debt maturities, except in 2016. Although NYT’s cash flows would fall short of their 2016 debt maturity, their sizable cash on hand should allow them to cover this as well. They also have a robust 172% recovery rate on unsecured debt, which should allow them access to credit markets if they choose to refinance their debt. We, therefore, rate NYT five notches higher at an IG4 credit rating, or a Baa2 equivalent using Moody’s ratings scale.

On the other hand, CDS markets are materially understating NYT’s credit risk with a CDS of 51bps relative to an Intrinsic CDS of 219bps, while cash bond markets are accurately stating credit risk with a cash bond YTW of 2.676% relative to an Intrinsic YTW of 2.886%.

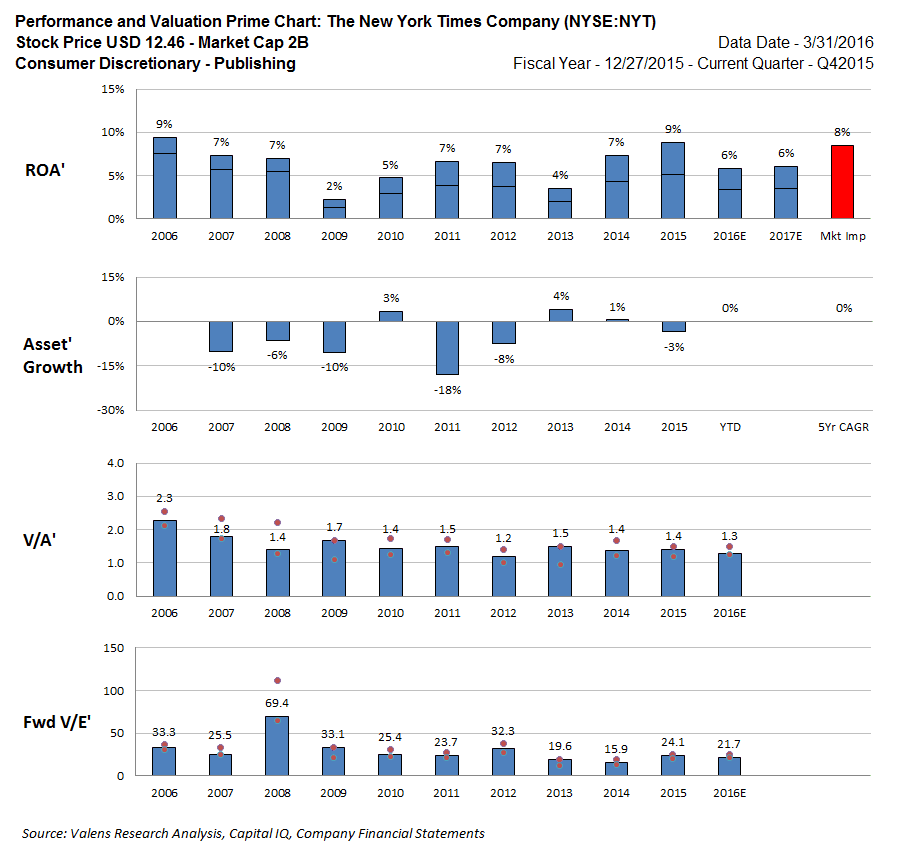

Equity markets see things with slight pessimism, with NYT trading at a historically low V/A’ of 1.2x. The market is expecting ROA’ to fade from 9% in 2015 to 8% over the next several years, with no Asset’ growth going forward. Considering the state of the newspaper industry and fundamental headwinds, muted market expectations are warranted. NYT equity is therefore likely fairly valued, with potential for equity downside if profitability fades further than markets expect.

Click here to read the article in its entirety at Seeking Alpha.