Limited Credit Risk For Investment Grade Rated L Brands, While Equity Markets Have Muted Expectations

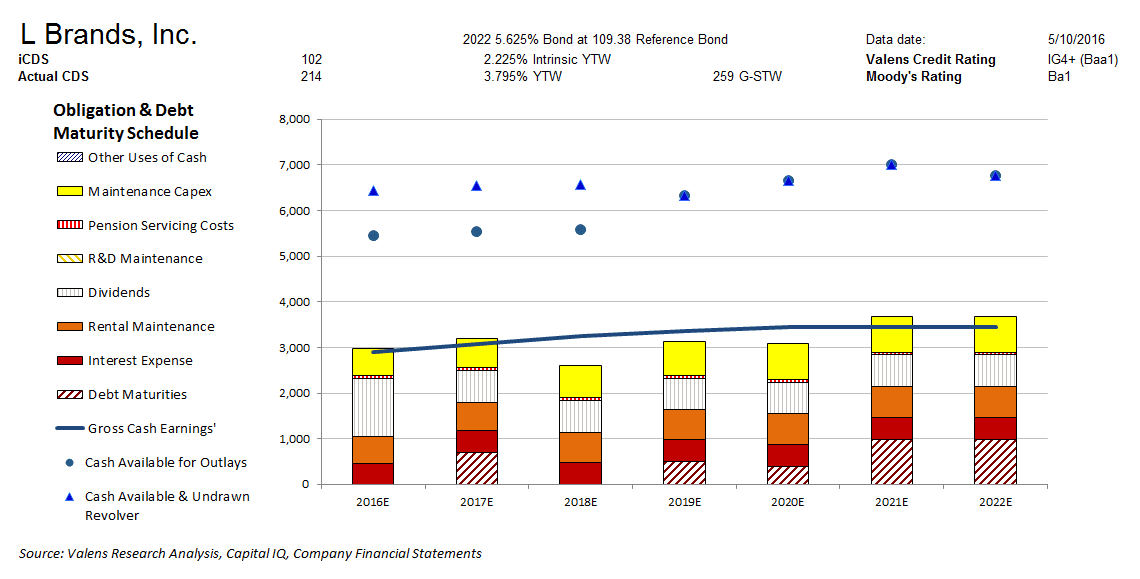

Moody’s is overstating the credit risk of L Brands, Inc. (NYSE:LB) with its Ba1 rating. Our fundamental analysis highlights a much safer credit profile for LB, whose strong cash flows cover all operating obligations going forward. Moreover, their healthy liquidity profile would allow them to service all obligations including debt maturities through 2022. We therefore rate LB three notches higher at an IG4+ credit rating, or a Baa1 equivalent using Moody’s ratings scale.

Meanwhile, cash bond markets are materially overstating the firm’s credit risk with a cash bond YTW of 3.795%, relative to an Intrinsic YTW of 2.225%, while CDS markets are overstating credit risk with a CDS of 214bps relative to an Intrinsic CDS of 102bps.

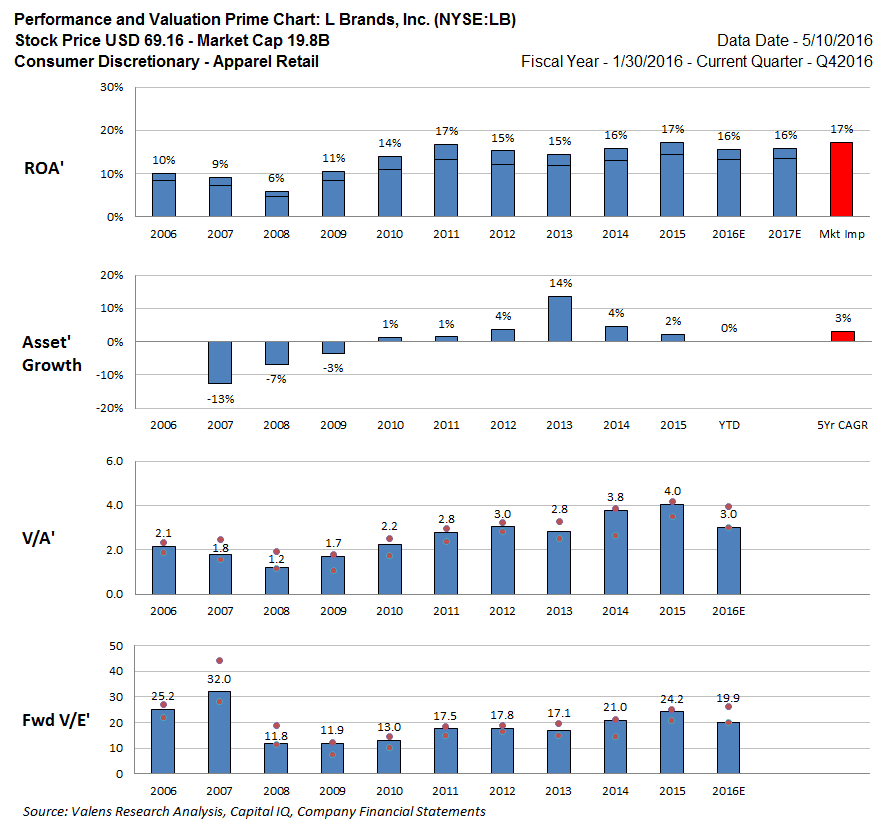

LB is trading at 19.9x V/E’, which is moderate relative to historical valuations. The market is expecting ROA’ to remain stable at 17% levels, with Asset’ growth of 3% going forward. Considering the fundamental headwinds that the firm is facing, muted market expectations appear warranted and the equity is likely fairly valued. However, if the firm struggles in the near term to replicate their record results, equity downside could be warranted.

Click here to read the article in its entirety at Seeking Alpha.