RT: Twitter Is #InvestmentGrade; #BullishEquity

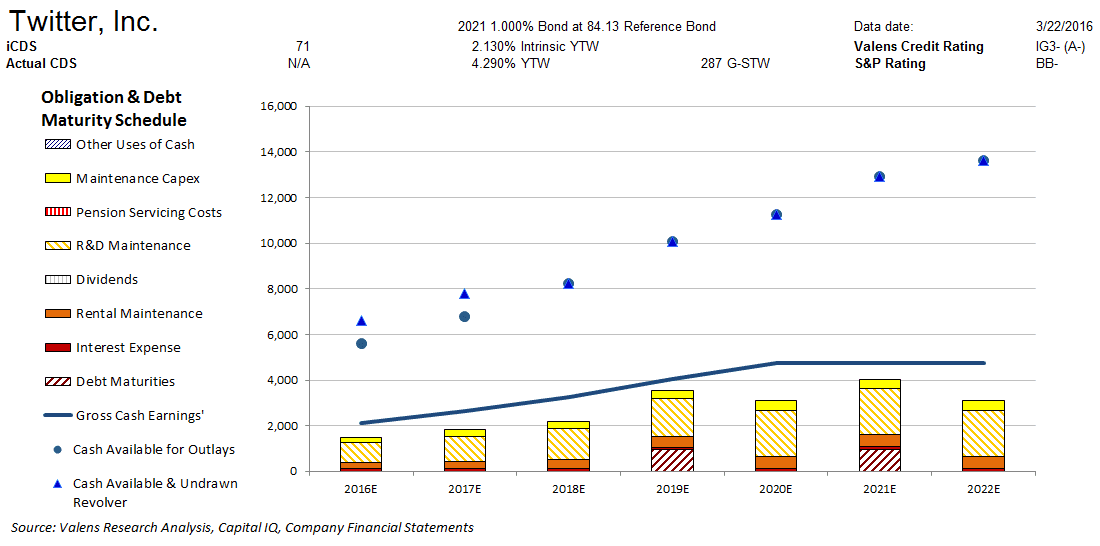

Moody’s is materially overstating the credit risk of Twitter (NYSE:TWTR) with its BB- rating. However, our fundamental analysis highlights a much safer credit profile for TWTR. The company’s strong cash flows easily cover all their obligations including debt maturities. Moreover, their sizable cash build should allow them to service all obligations including debt maturities if their cash flows ever fall short. We therefore rate TWTR six notches higher at an IG3- credit rating, or an A- equivalent using S&P’s ratings scale.

Moreover, convertible bond markets are materially overstating TWTR’s credit risk, with a convertible bond YTW of 4.290% relative to an Intrinsic YTW of 2.130%.

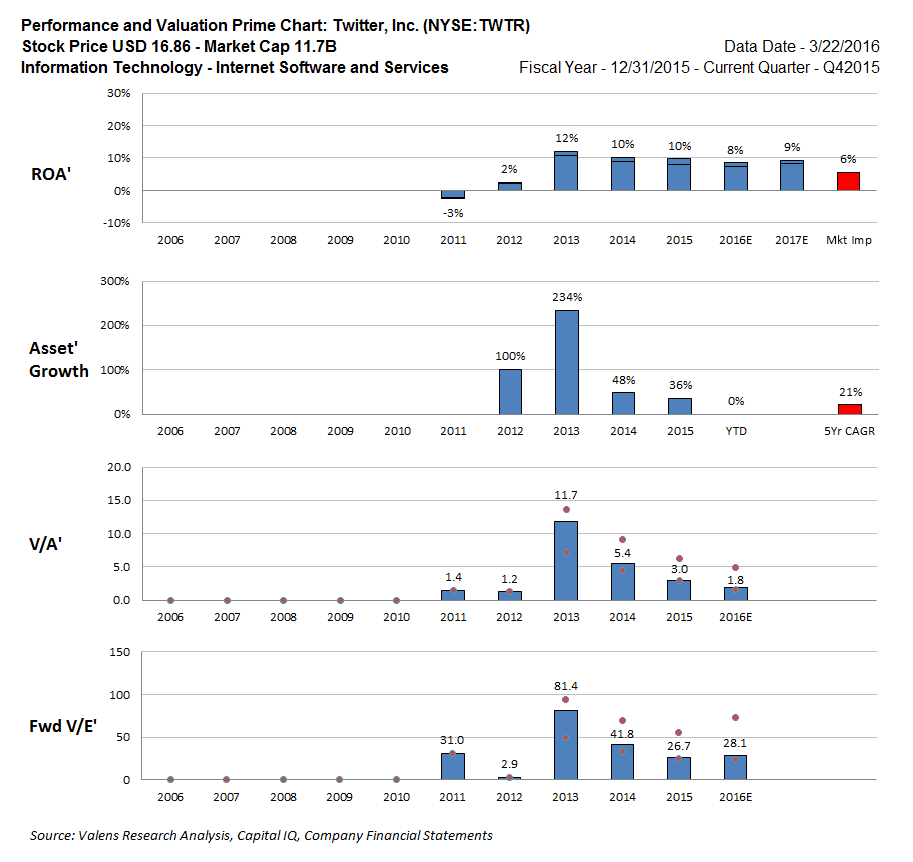

TWTR is trading at a 1.8x V/A’ and a 28.1x V/E’. The market is expecting ROA’ to decrease to 6% levels, with 21% Asset’ growth going forward. Consensus estimates are more bullish and forecast ROA’ to remain around current 1.5x cost-of-capital levels. Moreover, expectations for Asset’ growth of 21% appear to be a bit pessimistic, as they are expecting TWTR’s growth to halve from current levels. The company has also been improving fundamentals, and management’s confidence has been growing. With current market expectations, these tailwinds imply that equity upside may be warranted. On the other hand, TWTR’s convertible bonds for 2019 and 2021 both have a $77.64 strike price for conversion, well above current $16.86 levels.

Click here to read the article in its entirety at Seeking Alpha.