Uniform Accounting Highlights PSMT’s Adjusted EPS will be weaker than as-reported EPS, with slower growth, contrary to current valuations pricing the firm for perfection

- PSMT’s traditional EPS is materially distorted by operating leases, the age of their assets, and the resultant depreciation charges

- After making the appropriate UAFRS adjustments, EPS’ is expected to be significantly lower than as-reported EPS next year, as true profitability rebounds more slowly than as-reported EPS

- Materially weaker EPS’ at muted growth rates indicates the firm is significantly overvalued, with a PEG ratio in excess of 6x, and valuations at premiums to peers with greater expected growth

PriceSmart (PSMT) is expected to release Q2 2017 earnings of $0.90 per share on 4/6, representing a 4% growth rate over the same period last year, a continuation of improvements on a year over year basis last quarter, and a continued reversal of declines seen in EPS in the second half of fiscal 2016. This quarterly growth is expected to continue going forward, with expectations for NTM EPS of $3.22, a 7% growth rate over EPS of $3.00 on an LTM basis.

However, after making appropriate adjustments under Uniform Accounting Financial Reporting Standards (UAFRS), it is apparent that the only reason for the growth in the next four quarters is they are rebounding from a weak LTM, and EPS’ will also be weaker than as-reported metrics suggest.

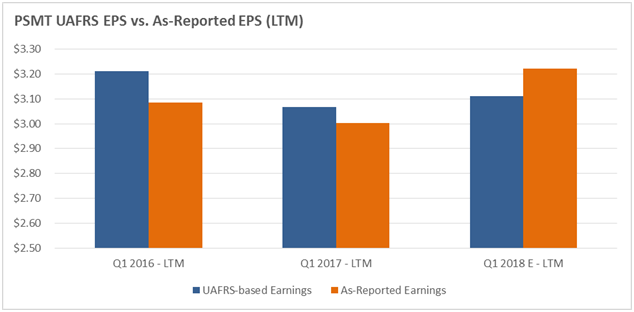

Specifically, under UAFRS, Adjusted EPS (EPS’) fell 5% over the past four quarters, double the 2.5% declines in as-reported earnings, and is only expected to rebound 1.5% over the next four quarters. As the charts below highlight, this is significant, as EPS’ will likely now fall below traditional EPS, indicating investors may not realize the significance of weakness in current profitability at PSMT. The firm’s EPS’ is expected to only reach $3.11 next year, up from $3.07 for the four quarters ended Q1 2017, but still down from $3.21 in the four quarters ended Q1 2016. Given the firm’s aggressive valuations relative to earnings, it is likely that the market is failing to recognize the firm’s faltering profitability.

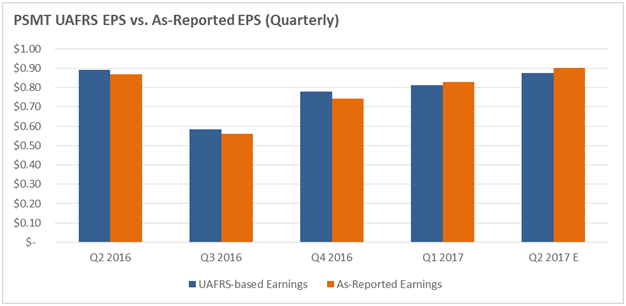

The quarterly results show a similar trend, with EPS’ lower than as-reported EPS in the last quarter, with expectations for further weakness. Given that these trends are likely to continue into the foreseeable future, valuations may be too strong at current levels.

UAFRS, Uniform Adjusted Financial Reporting Standards, call for removal of distortions from issues like the treatment of excessively aged, or relatively long-lived assets, as well as the treatment of operating leases. Once removed, it is apparent that EPS’ declines have been greater than as-reported metrics suggest, and will likely continue to be weaker than traditional EPS suggests, supporting potential downside at currently aggressive valuations.

UAFRS vs. As-Reported EPS

Investors make major decisions about which companies to own based on quarterly company earnings, the most common metric mentioned in traditional corporate investment analysis.

However, more often than not, the earnings that companies report in any given quarter can swing wildly and lead investors to completely wrong conclusions, because GAAP and IFRS rules force management to report results in ways that are not representative of the real operating performance of the business.

While there is a case to be made that some management teams can use “creative accounting” to adjust numbers, the research would show that more often than not, the real problem is with the accounting rules themselves, not management’s use of them.

Impact of Adjustments from GAAP to UAFRS

There are several adjustments required to make earnings representative of a firm’s true cash flows. For PSMT, the most material is related to adjusting for true depreciation of the firm’s assets, as well as operating leases.

PSMT has fairly long-lived assets on its books, with lives of 13-14 years. Given the long-lived nature of these assets, the true maintenance capex costs related to their assets is much higher than as-reported depreciation, which is reflective of the cost of those assets when the company bought them, which happened over five years ago for many of PSMT’s assets and beyond 10 years for some. As such, nominal asset values should be restated into constant-currency values to improve the reliability of business performance metrics, and the related depreciation (maintenance capex) expense should then be calculated off of the value of the Adjusted Asset base.

Additionally, PSMT’s operating lease expense is material. The decision management makes between investing in capex and investing in a lease is not a decision between an expense and an investment, but rather a decision in how management wants to finance their investments. If they would rather spend cash up front for the asset, they will spend capex. However, if they want to spread the cost of the asset over several years, they will instead choose to lease the asset. That said, as-reported accounting statements treat one as an investment, and the other as an expense that does not impact the balance sheet. Because PSMT materially spends on operating leases, as-reported metrics like EPS can materially understate the firm’s earnings power.

Weak earnings and limited growth spell downside at aggressive valuations

PSMT is currently trading at a 28.1x UAFRS-based P/E (Fwd V/E’), which is near historical highs. Considering recent declines in EPS’, and only modest expectations for a rebound, longer-term EPS’ growth expectations of 3%-5% imply a PEG ratio around 6x-9x, indicating the firm is significantly overvalued.

Moreover, even assuming a slight premium for “safe” consumer staples companies, PSMT looks overvalued. Compared to the ten other companies in our database in the Hypermarkets and Super Centers sub-industry, PSMT is trading at a premium valuation to eight, including Wal-Mart and Costco, who although are more mature companies, have greater expectations for earnings growth. With expectations so high, and weak expected performance, PSMT is poised to disappoint even if as-reported earnings are in line.

By using Uniform Adjusted Financial Reporting Standards (UAFRS), investors see a cleaner picture that distorted GAAP and IFRS metrics cannot show. By standardizing financial reporting consistently across time and across companies, corporate performance and valuation metrics improve dramatically. Comparability of a company’s earnings over time, trends in corporate profitability and comparability in earnings power and earnings growth across close competitors and different sectors becomes far more relevant and reliable.

To find out more about PriceSmart, Inc. and how their performance and market expectations compare to peers, click here to access the open beta of the Valens Research database.

Our Chief Investment Strategist, Joel Litman, chairs the Valens Equities and Credit Research Committees, which are responsible for this article. Professor Litman is a recognized global expert in advanced financial statement analysis, corporate performance, and valuation.