Advanced Micro Devices’ R&D Flexibility And Robust Recovery Rate Merit Better Credit Ratings, While Equity Markets Expect Imminent Upside

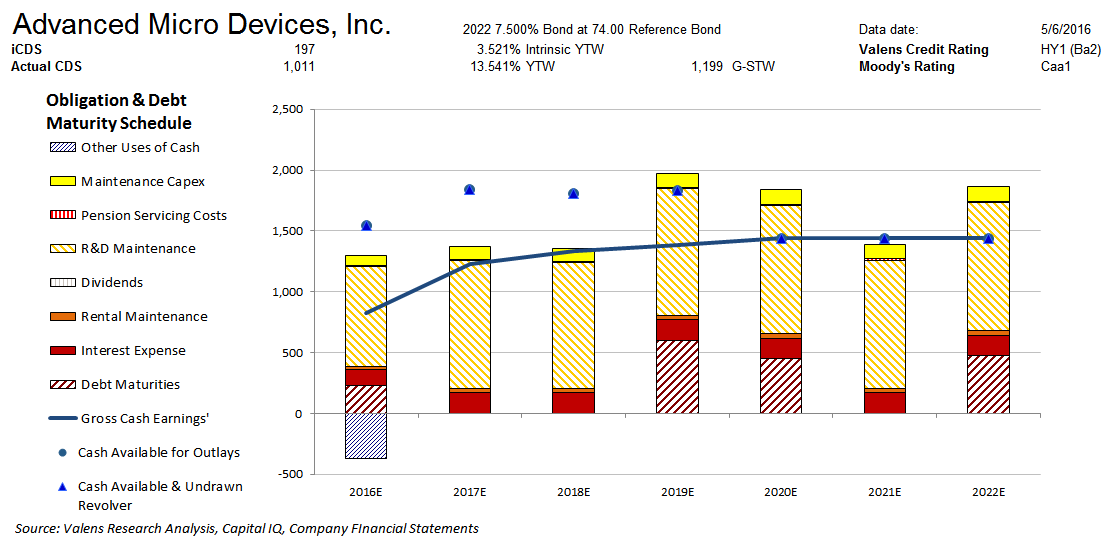

Moody’s is materially overstating the credit risk of Advanced Micro Devices, Inc. (NASDAQ:AMD) with its Caa1 rating. Our fundamental analysis highlights that AMD has cash flows that would exceed operating obligations each year except for 2017-2018. Furthermore, AMD’s healthy liquidity profile and flexibility around R&D spending would allow them to service all obligations including debt maturities beginning in 2019.

Moreover, credit markets are grossly overstating fundamental credit risk with a CDS of 1,011bps relative to an Intrinsic CDS of 197bps, and a cash bond YTW of 13.541% relative to an Intrinsic YTW of 3.521%.

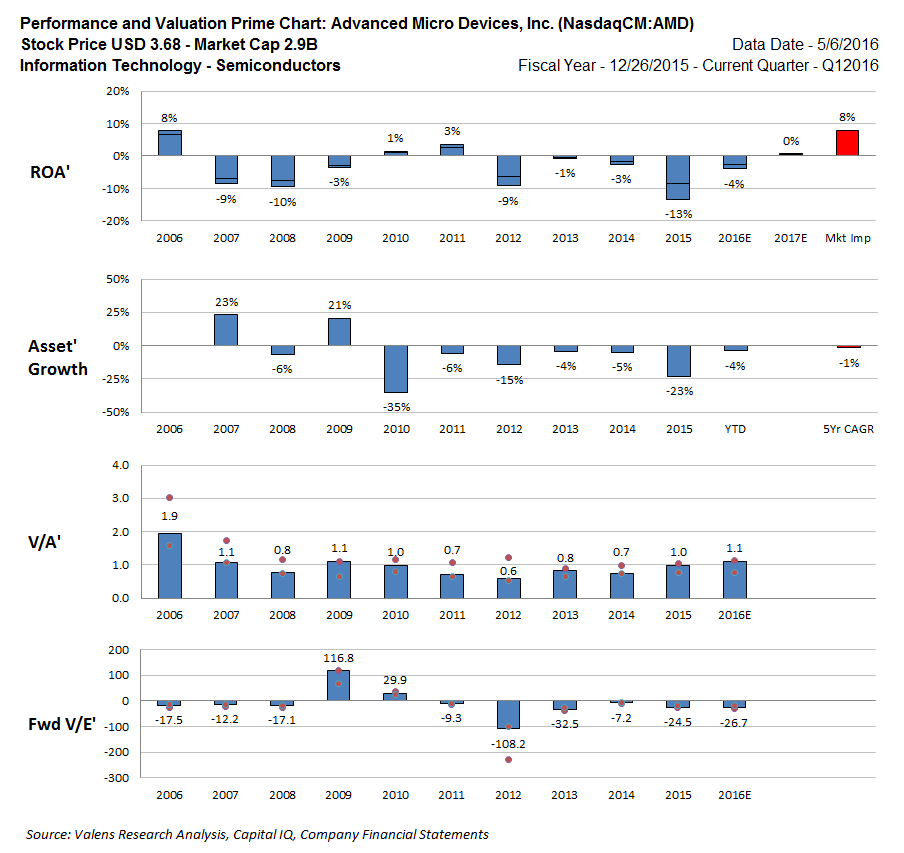

On the contrary, equity markets have a better outlook for AMD, trading at a V/A’ of 1.1x, which is high relative to historical averages. The market is expecting ROA’ to materially expand to 8%, with Asset’ shrinkage of 1% going forward. This appears too bullish given current fundamental headwinds and AMD’s historical performance, and may limit fundamental-driven upside. However, given current market expectations in the debt markets, there could be room for credit-driven equity upside if spreads were to tighten.

Click here to read the article in its entirety at Seeking Alpha.