Big Pharma is often spoken about with fear and mistrust.

The complicated legal battles and extensive regulatory battles have led to an unsteady relationship between people and companies at times.

From an investor’s point of view however, the fear and concern arise from a very different topic.

In particular, we are talking about pharmaceutical investment analysis and the difficulty in valuing them.

The two most terrifying words in a pharmaceutical analyst’s world are “patent cliff.” The cliff means the firm needs to think about when their blockbuster drug will no longer be a cash cow.

When a drug hits its “patent cliff,” the drug’s copyright has expired and the creator no longer has the protection from someone coming in and making a generic version.

A generic drug provides a very similar alternative at a dramatically reduced price. This in turn reduces the pricing power, profitability, and market share of the original drug.

The constant chance of innovation and the money that large pharmaceutical firms pour into R&D is because of this perpetual patent cliff risk.

Patent cliffs have taken down many great large-cap pharma companies throughout the years.

But there’s a related type of company for whom that language is less terrifying—biotech.

Pharmaceutical companies typically have portfolios made up of chemicals combined together in a specific recipe. When everyone knows the recipe they are generally easy to replicate. However, biotech companies have treatments that are much more complicated.

Biotech companies grow their complex biologic treatments, generally made up of complex proteins that fold in specific ways based on the cells they’re grown in. This means drugs can be challenging to replicate, even once off their patent.

With this increased complexity, patent cliffs are less scary, and even if someone comes out with the biologic equivalent to a generic drug, a biosimilar, they can’t just produce something with the same chemical markings and market it off the research the original maker did.

In other words, the barrier to entry is raised, as they must prove through clinical trials that it has the same activity. To prove this efficacy, they have to go through costly FDA trials.

For the original biotech, there is rarely a massive drop in price for its flagship drugs as the new entrant needs to recoup a high entry cost as well.

A great example of this is the biotech firm Amgen (AMGN) in the mid-2010s.

Amgen’s Neupogen and Epogen were market leaders for two decades before biosimilars of each came in the mid-2010s.

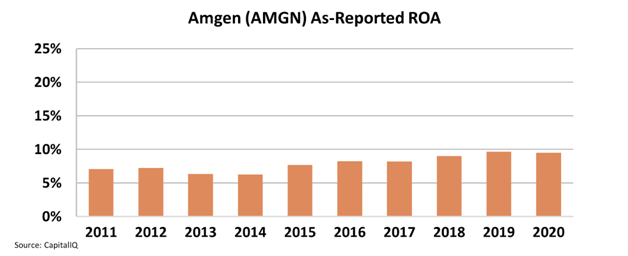

Looking at as-reported metrics make it look like the post-patent cliff AMGN was a 5%-10% ROA firm, with weak returns for a biotech with real products.

However, a closer look at the business’s real performance tells a much different story. Using Uniform Accounting adjusts for distortions such as goodwill and excess cash which are artificially inflating the assets on the balance sheet.

After resolving these discrepancies, we can see that returns have a very different reality.

Uniform metrics show ROA actually rose from 2011 until 2020 and was significantly stronger, showing how biotech companies can survive the patent cliff.

As long as complexities remain in the process, high barriers to entry and therefore high intellectual property protection will remain. Names like Amgen are poised to continue to retain their profitability even as they reach the patent cliff.

In our Conviction Long List, we highlight a plethora of names that have stronger earnings than reported that the wider investment community hasn’t yet caught onto. If you are interested in reading more, you can click here to subscribe.

SUMMARY and Amgen, Inc. Tearsheet

As the Uniform Accounting tearsheet for Amgen, Inc. (AMGN:USA) highlights, the Uniform P/E trades at 15.4x, which is below the global corporate average of 24.0x but around its own historical P/E of 16.3x.

Low P/Es require low EPS growth to sustain them. In the case of Amgen, the company has recently shown a 19% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Amgen’s Wall Street analyst-driven forecast is a 10% EPS decline in 2021 and a 23% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Amgen’s $228 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 5% annually over the next three years. What Wall Street analysts expect for Amgen’s earnings growth is below what the current stock market valuation requires in 2021 but above this requirement in 2022.

Furthermore, the company’s earning power in 2020 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations, and intrinsic credit risk is 50bps above the risk-free rate, signaling low credit and dividend risk.

Lastly, Amgen’s Uniform earnings growth is in line with its peer averages. However, the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.