Surging aluminum prices and strong industry tailwinds should have bolstered Century Aluminum Company’s (CENX) credit standing, yet it has been hammered with a B- rating. Today’s FA Alpha Daily will reveal the firm’s actual credit risk by leveraging the Credit Cash Flow Prime.

FA Alpha Daily:

Wednesday Credit

Powered by Valens Research

Most materials and resources have seen surging prices in recent years, ever since the start of the pandemic.

Diminished capacity due to labor constraints, combined with shipping delays, has spiked demand while reducing the available supply.

Aluminum is no different, as it has almost doubled in price from its lows at the start of the pandemic.

Both Investors and the public understand that demand is strong, and many of these increased prices are here to stay. The capex supercycle means that many of the tailwinds the industry has seen are likely to last. As the U.S. invests in historically old infrastructure, it will create a huge boom in spending that will kickstart another wave of earnings across the economy.

Century Aluminum Company (CENX), with access to many low-cost aluminum smelters in Iceland, should benefit from these increased prices and industry tailwinds. However, its credit ratings don’t illustrate that.

Rather, it is rated as a B- name, implying a 25% risk of defaulting in the next five years.

However, we can figure out if there is a real risk for this company by leveraging the Credit Cash Flow Prime (CCFP) to understand the company’s obligations matched against its cash and cash flows.

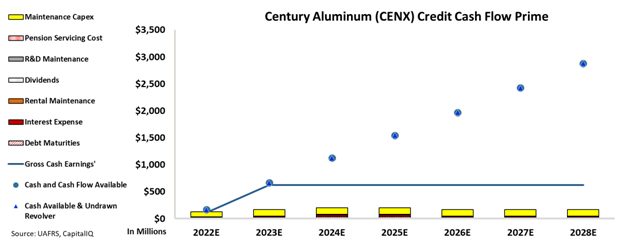

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As evidenced by the following chart, Century Aluminum has plenty of cash flow and cash on hand to cover all of its obligations going forward.

This is why we have rated the company a much safer investment-grade XO rating, due to its limited debt maturities and plentiful cash flows.

It seems the credit rating agencies have missed the tailwinds the company is experiencing and will continue to benefit from.

Rating agencies seem to be getting caught up in seeing increased prices and reduced supply as a cause of concern for future headwinds. But by thinking rationally and looking at the data to back it up, we can see that Century Aluminum will continue to be in a healthy position for years to come.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Century Aluminum Company Tearsheet

As the Uniform Accounting tearsheet for Century Aluminum Company (CENX:USA) highlights, the Uniform P/E trades at 8.5x, which is below the global corporate average of 20.6x, but above its historical P/E of -10.1x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Century Aluminum, the company has recently shown 50% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Century Aluminum’s Wall Street analyst-driven forecast is for an EPS growth of 75% in 2022 and EPS shrinkage of 258% in 2023.

Furthermore, the company’s earning power in 2020 is below the long-run corporate average. However, cash flows and cash on hand are more than 1x its total obligations—including debt maturities and capex maintenance, with a 360bps intrinsic credit risk. All in all, this signals a moderate credit and dividend risk.

Lastly, Century Aluminum’s Uniform earnings growth is well above its peer averages, and the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Century Aluminum Company (CENX) credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.