If there is a silver lining of the pandemic, it’s the renewed sense of cleanliness instilled in the world.

People had to actively think about being sanitary, many for the first time since learning to wash their hands as kids.

Certain trends like sanitizing every inch of clothing, groceries, and mail with disinfectant and leaving outdoor clothing in a “quarantine zone” were short lived fads.

But many businesses implemented better cleaning procedures to make their customers feel safe at their stores and restaurants. These trends appear they may be here to stay a little longer and could even help prevent the spread of the common cold or flu for years.

Businesses with direct public exposure like airlines and office buildings invested in better ventilation and public places like hospitals and doctors’ offices adopted stricter gear protocols.

Clean uniforms and gear were critical to have on hand at all times, not only for healthcare workers, but also anyone in the building, such as custodians.

It was undoubtedly a great time to be in the uniform and cleaning business, which is why companies like Cintas Corporation (CTAS) were still in high demand during the pandemic.

Cintas is an outsourced uniform provider that can deliver all the products a business needs to keep clean, including fresh uniforms and sanitizing and disinfecting products.

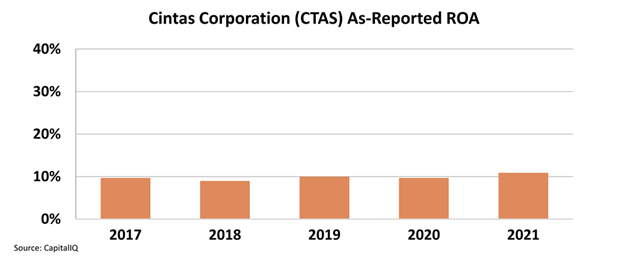

However, when we look at the as-reported return on assets (“ROA”), it shows us that the demand boom during the pandemic did nothing to help the business.

As-reported metrics make it appear Cintas’ ROA has been just about flat since 2017, sitting around 10% levels for the past five years.

As-reported metrics make Cintas look like a pretty disappointing company, as even when it was seeing a surge in demand, its ROA didn’t do anything different.

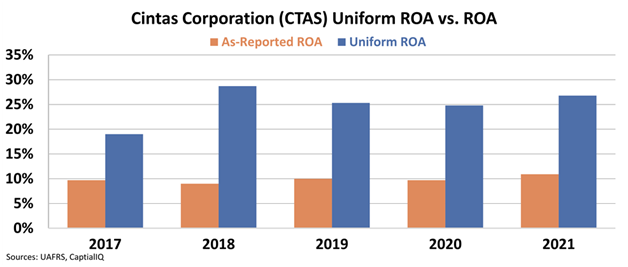

However, Uniform ROA shows us a different picture.

We can see that in reality, Cintas was significantly more profitable in this time frame, with ROA levels at or above 25% in each year since 2018.

Uniform Accounting allows us to see that COVID-19 and the general push to outsource non-core parts of your operation, including cleaning and uniforms, has been a major source of profitability for this company.

Even as the worst of the pandemic winds down, there’s still more attention paid to keeping public spaces cleaner and more sanitized, which is good news for a company like Cintas.

Without Uniform Accounting, investors would never realize Cintas’ strong and consistent profitability.

SUMMARY and Cintas Corporation Tearsheet

As the Uniform Accounting tearsheet for Cintas Corporation (CTAS:USA) highlights, the Uniform P/E trades at 32.5x, which is above the global corporate average of 24.0x and its own historical P/E of 27.1x.

High P/Es require high EPS growth to sustain them. In the case of Cintas, the company has recently shown a 21% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cintas’ Wall Street analyst-driven forecast is a 9% and 5% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cintas’ $424 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 12% annually over the next three years. What Wall Street analysts expect for Cintas’ earnings growth is below what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2021 is 4x the long-run corporate average. However, cash flows and cash on hand are below its total obligations in 2022, and intrinsic credit risk is 80bps above risk-free rate, signaling high credit and dividend risk.

Lastly, Cintas’ Uniform earnings growth is above its peer averages, and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research