Even though Sonos (SONO) is one of the world’s leading sound experience brands, investors could have easily been burned by its round trip. Today’s FA Alpha Daily will examine how the disruptions of as-reported metrics led investors to misinterpret Sonos’ profitability.

FA Alpha Daily:

Thursday Uniform accounting analysis

Powered by Valens Research

Throughout the pandemic, the world moved away from big cities, started working from home, invested at home, and communicated with each other via online tools available.

Most of these changes can be explained by the At-Home Revolution, which also changed the way businesses work dramatically.

They closed offices, adapted online systems, and gave their employees more flexibility in terms of working hours and place.

We saw which way the wind was blowing and looked for names that may benefit from it. One of our best ideas was Sonos (SONO), one of the world’s leading sound experience brands.

The company invented the multi-room wireless sound system in 2005 and has been leading the space since. Currently, it has a portfolio of home theater speakers, components, and accessories.

It has devoted lots of its resources to innovating new products, mostly focusing on wireless speakers. We saw how this industry had the opportunity to grow with the At-Home Revolution.

The stock was up 186% in less than a year from when we recommended it in June 2020 and took it off the list in March 2021.

We recognized the huge At-Home Revolution benefits the company was going to ride, which would lead to more spending on its equipment.

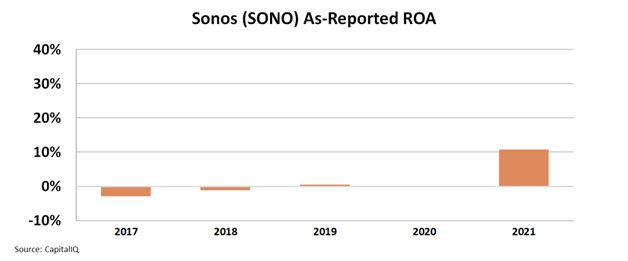

At the time, many investors looking at Sonos’ profitability were worried that the company did not make any money. This was understandable because investors were looking at the as-reported metrics.

The as-reported return on assets (“ROA”) of the company was negative until 2019 and became 0% in 2020, when we recommended investing in the name.

A 0% ROA means that Sonos had no real earnings at all. But why would we recommend a name incapable of generating any cash?

This was because we could see through the as-reported metrics.

There are lots of distortions in as-reported accounting and they can be fixed by making the over 130 adjustments needed under Uniform Accounting standards.

These adjustments allow us to see clearly what lies ahead in front of companies and their current position in the industry.

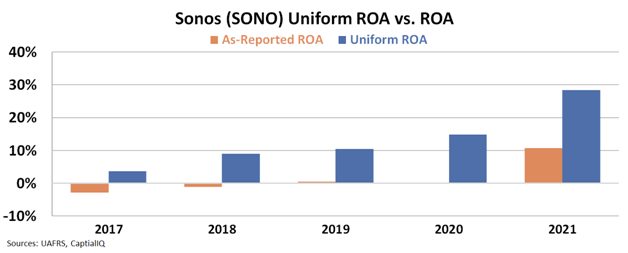

Using Uniform Accounting, it becomes clear that Sonos was already a profitable company before the At-Home Revolution. When the as-reported metrics showed negative profitability in 2018, the Uniform ROA was actually 9%.

Uniform ROA actually surged above 10% in 2019 before booming to 15% in 2020 and 29% in 2021.

As the ROA peaked, we walked away from the name. Macro signals told us a roll-over was happening as the home speaker market became saturated.

We managed to avoid the roll-over because Uniform metrics were helping us understand what was priced in and what the company’s peers could do.

We understood that the company has reached peak earnings at 20% and there was limited room for growth. The stock is down 54% since we recommended closing the position.

Investors that are not looking at the Uniform metrics not only missed the opportunity with Sonos, but also had no idea when to get out of the stock.

As-reported metrics hide the actual performance of companies, which leads to uninformed decision-making.

Uniform Accounting provides the right tools for investors to unlock the real value that the company offers. To learn more about how to gain access to the real numbers for almost 25,000 companies around the world, click here to read about our Uniform Accounting database.

SUMMARY and Sonos, Inc. Tearsheet

As the Uniform Accounting tearsheet for Sonos, Inc. (SONO:USA) highlights, the Uniform P/E trades at 11.1x, which is below the global corporate average of 20.6x, but around its own historical P/E of 11.0x.

Low P/Es require low EPS growth to sustain them. In the case of Sonos, the company has recently shown an 84% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sonos’ Wall Street analyst-driven forecast is a 3% and 21% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sonos’ $19 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% annually over the next three years. What Wall Street analysts expect for Sonos’ earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2021 is 5x the long-run corporate average. Also, cash flows and cash on hand are 5x its total obligations—including debt maturities and capex maintenance. However, the company’s intrinsic credit risk is 190bps above the risk-free rate.

All in all, this signals moderate operating and credit risk.

Lastly, Sonos’ Uniform earnings growth is below its peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.