In today’s FA Alpha, we will be tackling one of the most important yet overlooked pieces of analysis in the world of investing–understanding both equity and credit, through the lens of Steven Tananbaum, one of the most successful people to do it. By using Uniform Accounting, we will be evaluating how his portfolio, GoldenTree Asset Management, has been performing and what key learnings we can take away from it.

FA Alpha Daily:

Friday Portfolio Analysis

Powered by Valens Research

Back in 1998, I was asked to speak at a conference for credit investors…

I was 28 at the time, and given that the conference was in Las Vegas, I quickly accepted.

The one problem was that I knew very little about credit investing. At the time, most of my knowledge was in accounting and, to a certain extent, equity investing.

I knew most of the attendees would be investing in corporate bonds, credit default swaps, and other “credit” investments, so I was thinking on my feet to figure out how to provide the most value with my areas of expertise.

I was lucky to run into Mitchell Julis while I was preparing. Mitch is a co-founder of Canyon Partners, one of the largest and most consistent hedge funds in the U.S.

Canyon invests in many different asset classes, spanning from debt to equity and everything in between. But in particular, Mitch and Canyon focus on investing in debt.

While I was planning my presentation, Mitch gave me a great piece of advice I carry with me to this day.

First, he told me that great equity investors need to be deeply knowledgeable on credit, and great credit investors need the same focus on equity.

Then, he said that my accounting knowledge is what the credit investors were interested in – if I focused on giving a full picture of understanding a company, they would figure out how it applies to credit.

Mitch made a fairly simple point. To put it differently, he was stating that successful equity and credit investors look at the company as a whole.

It’s a logical thought, but it’s one that investors often overlook…

Whether you’re buying equity or credit, you’re buying a small claim on a company. If you were buying a car or a house, you’d want to inspect the whole asset, right?

But countless equity investors fail to properly understand a company’s credit before buying its stock.

A business finances itself with a combination of debt and equity.

In the event a company liquidates, debtholders have the first claim on that company’s assets… while equity investors get whatever is left over. As a result, it’s critical for equity investors to understand a company’s credit risk before making an investment.

That is exactly what Steven Tananbaum’s GoldenTree Asset Management does. He evaluates companies as a whole and makes investment decisions accordingly.

His strategy is focused on finding companies that look distressed on the credit side with massive upside potential on the equity side, and this holistic approach to investing made him one of the most successful investors in distressed debt.

To show what we mean, we’ve done another high-level portfolio audit of GoldenTree Asset Management’s top holdings, based on their most recent 13-F. This is a very light version of the custom portfolio audit we do for our institutional clients when we analyze their portfolios for torpedoes and companies they may want to “lean in” on.

See for yourself below.

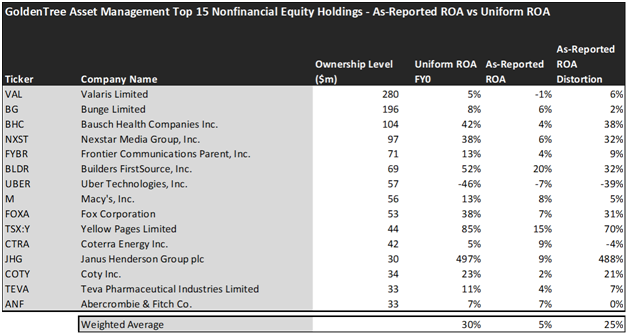

Using as-reported accounting, investors would think investing with GoldenTree Asset Management is not that profitable.

On an as-reported basis, many of these companies are poor performers in terms of profitability with an average as-reported ROA of just 5%, which is way below the corporate averages in the United States.

However, once we make Uniform Accounting (UAFRS) adjustments to accurately calculate earning power, we can see that the returns of the companies in GoldenTree Asset Management are much more robust.

The average company in the portfolio displays an average Uniform ROA of 30%, which is more than two times the average corporate returns.

Once the distortions from as-reported accounting are removed, we can realize that Nexstar Media Group (NXST) doesn’t have 6% returns, but a Uniform ROA of 38%.

Similarly, Bausch Health Companies’ (BHC) ROA is actually 42%, not 4%. Bausch Health is a Canadian multinational specialty pharmaceutical company that develops, manufactures, and markets pharmaceutical products and branded generic drugs, primarily for skin diseases, gastrointestinal disorders, eye health, and neurology.

Janus Henderson Group (JHG) is another great example of as-reported metrics misrepresenting the company’s profitability. With a Uniform ROA of 497%, an as-reported of 9% is wholly misleading and misses the story.

To find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

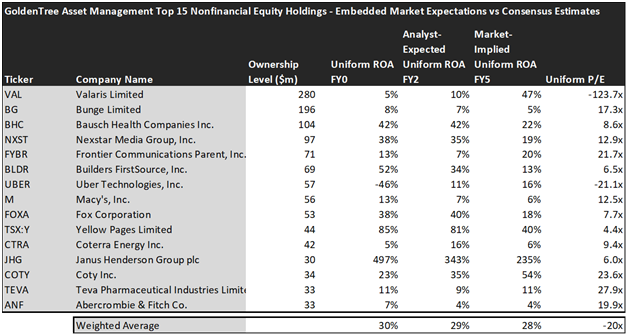

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The Uniform ROA FY0 represents the company’s current return on assets, which is a crucial benchmark for contextualizing expectations.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here is 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 24x.

Embedded Expectations Analysis of GoldenTree Asset Management paints a clear picture for investors. As the stocks it tracks are strong performers historically, analysts are pricing them to slightly increase in profitability. Meanwhile, the market is a bit more optimistic, which could cap future upside.

While analysts forecast the fund to see Uniform ROA improve to 29% over the next two years, the market is pricing the fund to see returns increase to 28%.

However, there are a few names that have a large discrepancy between analyst and market expectations, which should lead investors to be cautious.

The markets are pricing Valaris’ (VAL) Uniform ROA to rise to 47%. Meanwhile, analysts are projecting the company’s returns to increase to 10%.

Frontier Communications Parent (FYBR) may further disappoint investors as their returns are expected to increase to 20% Uniform ROA, while the analysts expect them to decline returns to 7%.

To sum up, the portfolio is composed of strong performers and high-growth names that can deliver impressive returns, but investors should carefully analyze the current investment environment and valuations before making a strategic decision.

This just goes to show the importance of valuation in the investing process. Finding a company with strong growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which have not been fully priced into their current prices.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of the fund’s largest holdings.

SUMMARY and Valaris Limited Tearsheet

As GoldenTree Asset Management’s largest individual stock holding, we’re highlighting Valaris Limited (VAL:USA) tearsheet today.

As the Uniform Accounting tearsheet for Valaris Limited highlights, its Uniform P/E trades at -123.7x, which is below the global corporate average and its historical average of -54.5x.

Negative P/Es only require low EPS growth to sustain them. In the case of Valaris Limited, the company has recently shown -7% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Valaris Limited’s Wall Street analyst-driven forecast is for EPS to deeply shrink by 444% and 290% in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Valaris Limited’s $58 stock price. These are often referred to as market-embedded expectations.

The company is currently being valued as if Uniform earnings were to decline by 7% annually over the next three years. What Wall Street analysts expect for Valaris Limited’s earnings growth is below what the current stock market valuation requires through 2023.

Meanwhile, the company’s earning power is neutral in the long-run corporate averages. Also, cash flows and cash on hand consistently exceed the total obligations—including debt maturities and capex maintenance. However, intrinsic credit risk is 170bps. All in all, these signal moderate credit risk.

Lastly, Valaris Limited’s Uniform earnings growth is below peer averages, and is trading below its average peer valuations.

Best regards,

Joel Litman

Chief Investment Strategist at Valens Research

This portfolio analysis highlights the same insights we share with our FA Alpha Members. To find out more, visit our website.