Forging strong relationships is the foundation of all good businesses.

That’s why all stakeholders in a business are putting a greater and greater emphasis on sourcing quality customer data, and making relationships that help them obtain this data.

For businesses to get the right kind of data about their customers, they need to be actively involved in conversations with them, instead of just having a transactional relationship.

This kind of conversation is moving from a good-to-have to a necessity in the business world, as companies in all industries are getting smarter at leveraging their advertising spend. It is for this reason that tools like SurveyMonkey have become so powerful and popular.

These kinds of tools fuel corporate engagement and communications, and Momentive Global (MTNV) tools like SurveyMonkey and GetFeedback solutions have seen significant growth.

In an age where the world is increasingly pivoting to a relationship-based economy, demand for Momentive Global’s services will only continue to grow.

And yet, the credit agencies seem to have an issue with their data because they continue to underestimate Momentive Global.

They are failing to recognize these tailwinds, and instead rate it like it’s got a 25% chance of going bankrupt by assigning it a B credit risk.

However, when we look at their credit picture without any bias, a different picture emerges. Momentive’s Credit Cash Flow Prime (CCFP) is way healthier than credit ratings agencies imply.

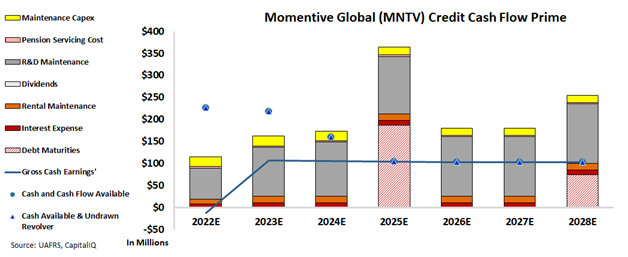

We can figure out if there is a real risk for this high-potential company by leveraging the CCFP to understand the company’s obligations matched against its cash and cash flows.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Its B rating suggests a high risk of default, but the CCFP shows that Momentive doesn’t have an issue covering its debt until 2025, when it has time to refinance its obligations over multiple years. Additionally, the company can cut back on flexible operating costs such as its high R&D spend to unlock additional capital.

That’s why the Valens Credit Rating is a much stronger XO or crossover rating.

Rating agencies seem to be missing the potential success of companies once again, by giving Momentive a credit rating that implies it is riskier than the company actually is.

On the contrary, Valens Credit Rating represents the full story of the company. Momentive has a lot less risk attached to it than what the rating agencies suggest.

It is our goal to bring forward the real creditworthiness of companies, built on the back of better Uniform Accounting.

To see Credit Cash Flow Prime ratings for thousands of companies, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Momentive Global Inc. Tearsheet

As the Uniform Accounting tearsheet for Momentive Global Inc. (MNTV:USA) highlights, the Uniform P/E trades at -35.7x, which is below the global corporate average of 20.6x, but above its historical P/E of -48.3x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Momentive, the company has recently shown 7% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Momentive’s Wall Street analyst-driven forecast is for an immaterial EPS growth and 45% EPS shrinkage in 2022 and 2023, respectively.

Furthermore, the company’s earning power in 2021 is below the long-run corporate average. Moreover, cash flows and cash on hand are also below its total obligations—including debt maturities and capex maintenance, with a 150bps intrinsic credit risk. All in all, this signals a moderate credit and dividend risk.

Lastly, Momentive’s Uniform earnings growth is below its peer averages, but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

This analysis of Momentive Global Inc. (MTNV) credit outlook is the same type of analysis that powers our macro research detailed in the FA Alpha Pulse.