There’s been a great deal of discussion about how Ryan Cohen can transform GameStop (GME) as chairman, and now Bed Bath & Beyond (BBBY) with his new 10% stake.

Before people start to build models or predict the future of these businesses, it is worth a look at how he did with the company that made him a name in retail, Chewy (CHWY).

Ryan Cohen got his start by founding Chewy, an ecommerce pet store company that sells practically everything pet owners could need, from food to toys and even medication.

Chewy, which rivaled the largest pet stores when it was still public, was bought out by PetSmart in 2017 for more than $3 billion, which was the largest ecommerce acquisition at the time.

Cohen then moved on to GameStop, and it was his appointment to the chairman position that acted as a final catalyst for the short squeeze.

People look to Cohen to help companies like GameStop turn around, but he doesn’t necessarily have a history of making that happen.

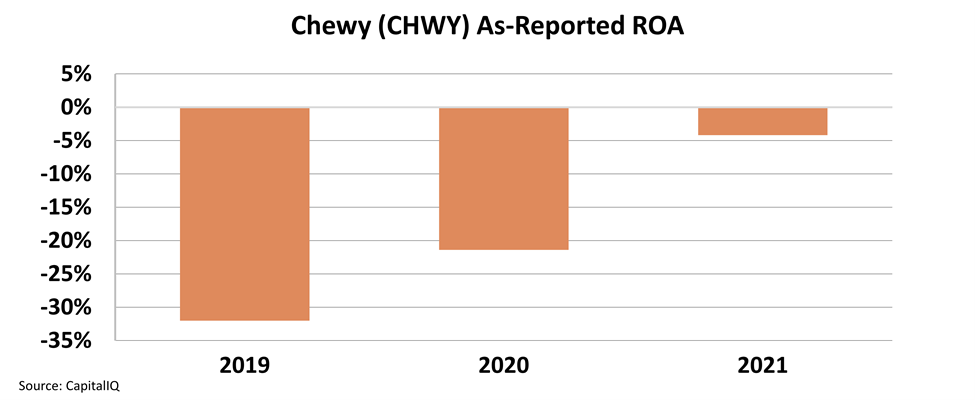

Looking at as-reported accounting metrics, it looks like Chewy struggled to make money with Cohen’s strategy. For the past three years, it appears return on assets (“ROA”) was in the negative levels, rising from -32% in 2019 to -4% in 2021.

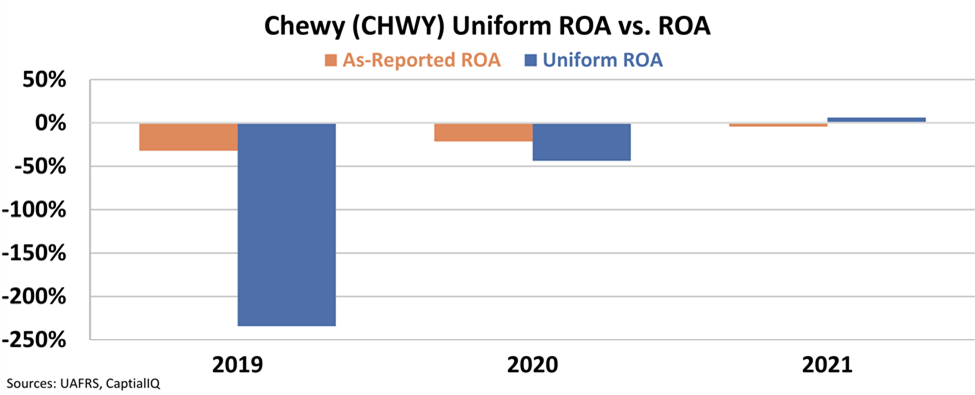

While as-reported metrics clearly make it seem Chewy wasn’t doing too well, it actually underestimates how much the company was losing each year from Cohen’s legacy.

Uniform metrics show us Chewy was doing significantly worse than as-reported accounting made it appear.

In 2019, it had a -234% ROA. While Chewy’s returns improved to -44% in 2020 and 6% in 2021, it was only because of record pandemic demand, well after Cohen left the business.

Not only did people buy more pets and increase the demand for pet supplies during the pandemic, but there were also more people looking to have their pet food delivered directly to their houses.

It seems Cohen didn’t do much for the performance of his own company—perhaps expecting him to be able to turn around other struggling companies is a longer shot than most want to admit.

If GameStop and Bed Bath & Beyond follow in the footsteps of Chewy under Ryan Cohen’s tutelage, they will have a harder time than people expect to return to the limelight.

SUMMARY and Chewy, Inc. Tearsheet

As the Uniform Accounting tearsheet for Chewy, Inc. (CHWY:USA) highlights, the Uniform P/E trades at 250.8x, which is above the global corporate average of 24.0x, and its own historical P/E of 241.0x.

High P/Es require high EPS growth to sustain them. In the case of Chewy, the company has recently shown a 118% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Chewy’s Wall Street analyst-driven forecast is a 183% and 20% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Chewy’s $35 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 108% annually over the next three years. What Wall Street analysts expect for Chewy’s earnings growth is above what the current stock market valuation requires in 2022 but below that requirement in 2023.

Furthermore, the company’s earning power in 2021 is in line with the long-run corporate average. However, cash flows and cash on hand are 5x its total obligations—including debt maturities and capex maintenance. All in all, this signals low credit risk.

Lastly, Chewy’s Uniform earnings growth is above its peer averages, and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.