It’s easy for investors to assume pharmaceutical companies are money-making machines but lack an easy way to measure this outperformance. Using Uniform Accounting, we can easily see exactly how much.

While the corporate average Uniform return on assets (“ROA”) sits at about 10%, the average Uniform ROA for the top 50 pharma companies is on average 22%, more than twice as large.

Many people believe this is the case because we are willing to pay anything to keep people healthy. But when you look at pets and livestock, you see that the same high profitability extends into that portion of the industry as well.

As just one example, the “Cavapoo” dog breed is known to have heart problems. This means there are multiple Cavapoo cardiologists operating in the northeast U.S. alone.

Zoetis (ZTS), the world’s largest producer of medicine for pets, is proof of that.

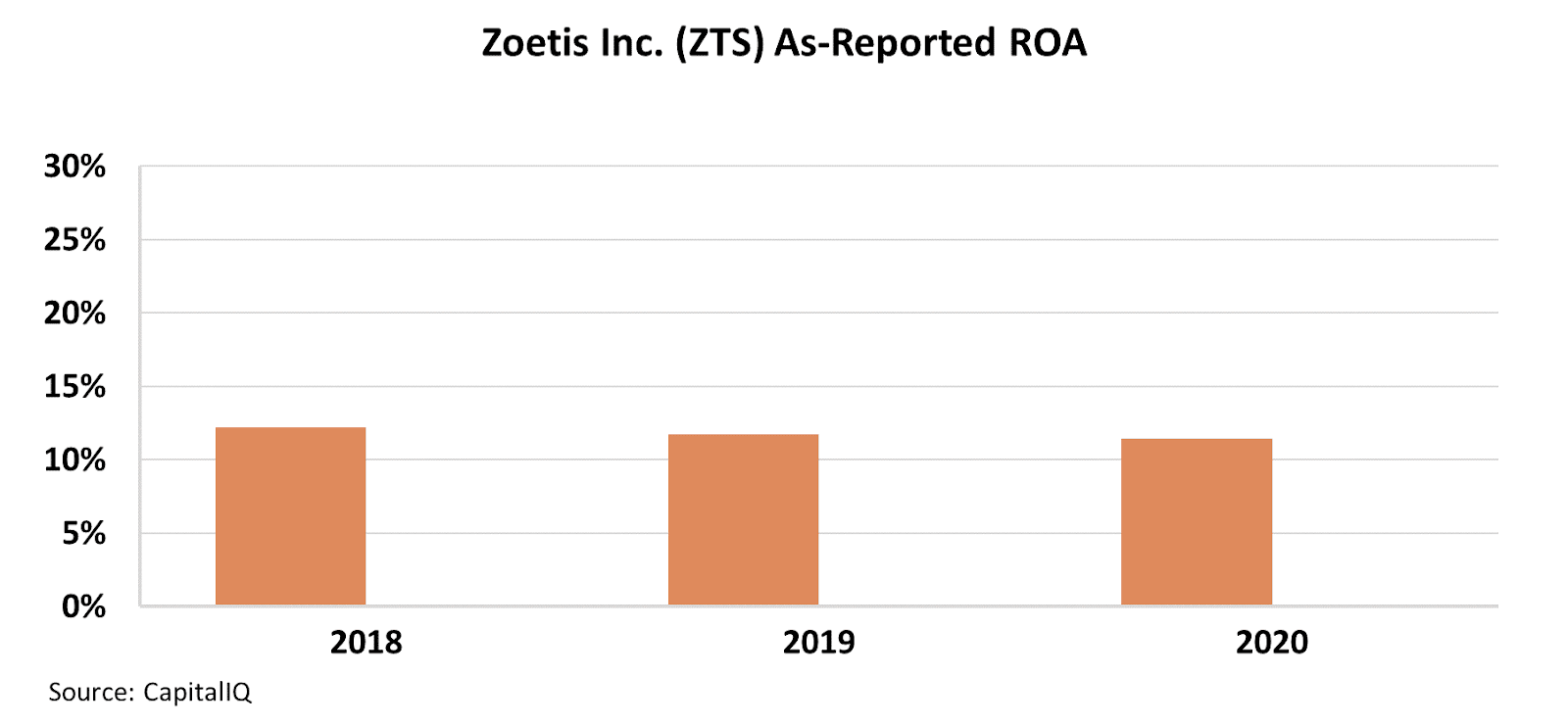

Looking at as-reported metrics, though, it looks like the company barely has a double-digit ROA. For the past three years, Zoetis’ ROA seems to have sat at 11%-12% levels. That’s not terrible, but it’s also not anything extraordinary. Zoetis seems to just be another average company.

With performance like this, it appears that we don’t value the health of our animals nearly as much as the health of people.

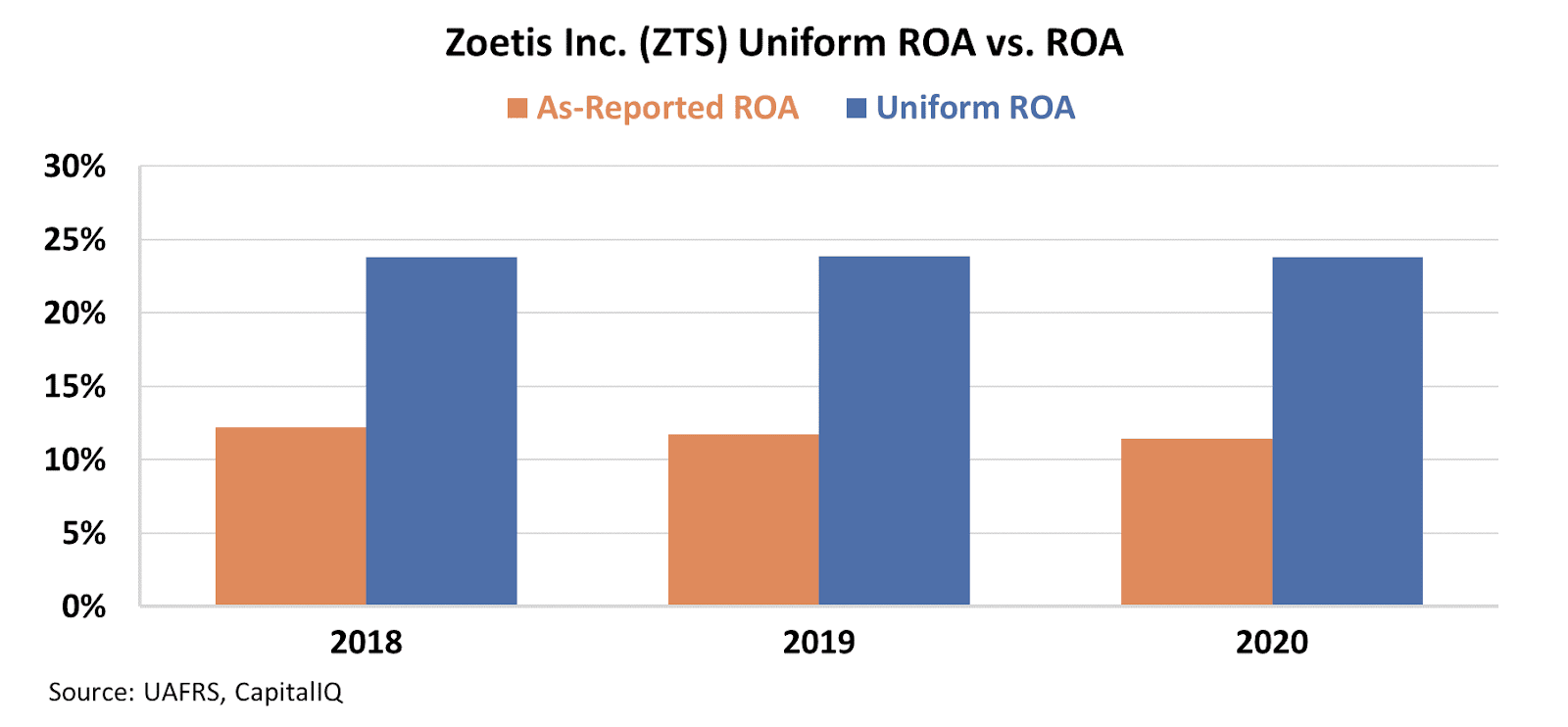

However, Uniform Accounting tells a bit of a different story. We can see that the saying that our pets are “a man’s best friend” maybe stands to be true after all.

With a closer look, Uniform metrics show that Zoetis’ ROA has been rising and even reached 24% last year, surpassing the already high pharmaceuticals average.

With Americans spending more than $100 billion on their pets in 2020, this comes as no surprise.

Pets are treated as part of the family, and when it comes to their health, their owners are willing to spend the big bucks.

This allows companies like Zoetis to flourish. And considering the pandemic caused a spike in pet adoptions as more people sat at home, it doesn’t seem the demand for pet healthcare will be going away any time soon.

So as the pharma industry continues to rise above, Zoetis will be right up there alongside the industry, if not ahead of some of the best companies out there.

It points to just how valuable being in the pharma space is, including if it’s pharma for animals and not people.

SUMMARY and Zoetis Inc. Tearsheet

As the Uniform Accounting tearsheet for Zoetis Inc. (ZTS:USA) highlights, the Uniform P/E trades at 36.7x, which is above the global corporate average of 24.0x and its own historical P/E of 31.6x.

High P/Es require high EPS growth to sustain them. In the case of Zoetis, the company has recently shown a 6% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Zoetis’ Wall Street analyst-driven forecast is a 20% and 12% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Zoetis’ $188 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 17% annually over the next three years. What Wall Street analysts expect for Zoetis’ earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are almost 3x its total obligations, signaling low credit and dividend risk.

Lastly, Zoetis’ Uniform earnings growth is above its peer averages and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

The Uniform Accounting insights in today’s issue are the same ones that power some of our best stock picks and macro research, which can be found in our FA Alpha Daily newsletters.