5 years ago, we showed Moody’s was getting this company wrong. TRUE uniform cash flows show that even after the stock’s run, there’s still opportunity

This company’s stock and bonds have both performed extremely well thanks to an improved credit position and the boom in AI. However, Moody’s is STILL incorrectly misrating the name.

TRUE uniform UAFRS-based cash flow analysis shows what Moody’s totally missed 5 years ago, and is still missing now.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting- based Performance and Valuation analysis of the company…

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

In 2015 Robin Blumenthal at Barron’s produced a piece on AMD (AMD), the semiconductor firm. She had a positive call on the stock.

A major reason was the transformation that the company was going through under the new CEO Lisa Su. She was cutting costs and moving into new businesses generating significant revenue and importantly for AMD, she was focused on improving their credit position.

Because of the credit tilt of the article, Blumenthal had come to Valens to understand if AMD really was an interesting idea or if the credit would serve to sink the stock further. (Valens Research is unique in the investment research space because we analyze equities and corporate credit together, among other reasons).

At the time, as-reported cash flow from operations had been negative for each of the last 3 years for AMD, so creditors were spooked. Moody’s was rating the name as a B2 credit, deep in high yield also know as deep junk debt – meaning imminent bankruptcy.

Credit default swaps (CDS), which are an insurance contract for creditors to hedge the risk of a bankruptcy, were trading at above 600bps. That was a highly elevated level, signalling real risk of distress for the credit. The 2019 bonds were trading at a yield of 8.3%.

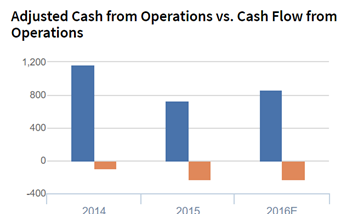

At the time of the article, one could only see the 2014 numbers in the chart above. That was more than enough.

Uniform Accounting analysis provided Blumenthal an explanation for the market’s and Moody’s credit concerns – the orange bar.

It also provided the insight for the opportunity and that the market had overreacted – the blue bar.

Those overblown credit concerns were part of the reason why AMD was such a compelling equity idea, and they made it an interesting credit idea also.

The problem with GAAP and IFRS accounting is that they completely misrepresent a company’s real performance in earnings and in cash flows.

Among many reasons, AMD’s non-cash stock option expense, and their significant R&D investment, flowed through as-reported operating cash flows, making that number look negative.

In reality, in 2014 AMD didn’t have negative cash flow from operations. Uniform-based cash flow from operations was almost $1.2 billion. The company’s commitment to investing in the growth engines that Su had identified was being miscategorized as an operating expense under GAAP, among other issues.

Once we made that adjustment, and several more, we could see AMD would have no issues paying their debts in the future. With the bonds trading at an 8% yield, and the equity priced for bankruptcy, that made the stock and the bonds an incredible opportunity.

Since then, AMD’s CDS has dropped to 60bps, meaning buying insurance on AMD’s bonds costs only 0.6% a year. AMD is priced like an investment grade credit.

And yet, Moody’s still rates AMD as a Ba2 credit, still in high yield, junk debt land. Moody’s has been significantly on the wrong side of this for five years.

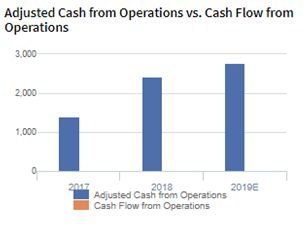

How does the chart look today, showing Moody’s has still not figured it out?

GAAP operating cash flows still misrepresent how profitable AMD really is. The orange bars don’t even show on this chart because the as-reported GAAP cash flow from operations is very, very close to zero.

In reality, AMD generated over $2 billion in operating cash flows last year. That’s what Uniform Accounting tells us.

Using as-reported metrics, one would think the company was still in trouble. It isn’t.

The stock has risen from $2.50 when we originally talked to Barron’s in early 2015 to $48 today. This stems from both reduced credit risk and the AI boom.

Meanwhile, Moody’s continues to focus on bad data, the as-reported GAAP data, misrating the bonds.

That misrating may have created an opportunity. The 2024 bonds are trading with a yield-to-worst interest rate at 5%. In a market where investment-grade debt yields a far lower level, Moody’s may have convinced enough people to price this debt too cheaply.

The fact is, a large market of potential credit holders are simply mandated to not buy whatever bonds that Moody’s deems as junk. This is regardless of the quality – or lack thereof – of Moody’s analysis.

That makes for a compelling idea for credit holders.

This looks especially compelling because the company has such robust cash flows, and management is excited about their outlook for their business going forward.

Healthy liquidity, a robust recovery rate, and R&D flexibility indicate cash bond markets and ratings agencies are overstating credit risk

Credit markets are accurately stating CDS risk with a CDS of 57bps relative to an Intrinsic CDS of 47bps, while cash bond markets are grossly overstating credit risk with a YTW of 5.136%, relative to an Intrinsic YTW of 2.076%. Furthermore, Moody’s is materially overstating the firm’s fundamental credit risk, with their Ba2 credit rating seven notches lower than Valens IG3+ (A1) credit rating.

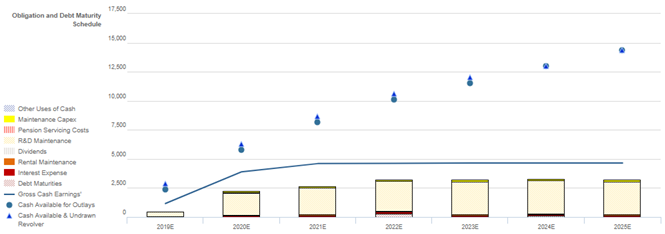

Fundamental analysis highlights that AMD’s cash flows should exceed all obligations including debt maturities in each year going forward. Furthermore, with a healthy liquidity profile and R&D spending flexibility, the firm should have no issues servicing all obligations including debt maturities through 2025 even if cash flows weaken. Additionally, with a robust 300% recovery rate on unsecured debt and a large market capitalization, AMD should have no issues accessing credit markets to refinance if needed.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for credit holders. AMD’s compensation metrics should drive management to focus on improving all three value drivers: top-line growth, margins, and asset utilization, which would lead to Uniform ROA expansion and increased cash flows available to servicing debt obligations. Furthermore, most members of management hold material AMD equity relative to their annual compensation, aligning them with shareholders for long-term value creation. That said, apart from CEO Su, management is well compensated in a change-in-control scenario, indicating they may be incentivized to pursue a sale or accept a takeover, elevating event risk for credit holders, though she may influence them to do otherwise.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (10/29) highlights that management generated excitement markers when discussing further product announcements in Q4 and the strong positioning of their product portfolio. That said, they may be concerned about the sustainability of recent 7-nanometer revenue growth, and they may lack confidence in their ability to drive a richer product sales mix.

Healthy liquidity, a robust recovery rate, and R&D flexibility indicate cash bond markets and ratings agencies are overstating credit risk. As a result, a tightening of bond spreads and a ratings improvement are likely going forward.

AMD Tearsheet

As our Uniform Accounting tearsheet for AMD highlights, AMD trades well above market average valuations. The company has recently had over 400% Uniform EPS growth. EPS is forecast to actually fall, -17%, in 2019, but will return to strongly positive 82% levels in 2020. Lumpy earnings is a natural phenomenon in this space.

At current valuations, the market is pricing the company to see earnings grow by 15% a year going forward.

The company’s earnings growth is forecast to be around peer averages in 2019, but the company is trading well above peer average valuations. The company has strong returns, and no cash flow risk going forward.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research