Investors are concerned about a tax plan come November, here is what it would do to a portfolio if it comes

Last week, we discussed the possibility of inflation impacting stock market valuations.

Now, it is important to address the other major factor that drives market valuations, the tax rate. Some investors fear that a Biden victory could be catastrophic to the stock market because of taxes.

When gauging how likely a Biden administration would significantly raise taxes, it is also important to measure how a high tax rate is a headwind for valuations.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Last week, we discussed the possibility of a high inflation event and how it would impact the shape of the recovery. The other macroeconomic factor that drives valuations is the tax rate. With the growing probability of a Biden victory this November, discussion around the tax rate has once again entered the discussion for investors.

First, it is important to understand if Biden wins, it does not necessarily mean taxes will skyrocket.

A Biden victory does not spell doom for the market. A key question to understand its implication is to what extreme the Democrats win the election if they do. The President doesn’t govern on his own–to pass laws he or she also needs to work with the Senate and House of Representatives.

If the Senate does not win a filibuster-proof majority, which is currently not a certainty, or the Democrats miss the mark in the House, which admittedly is more of a long shot, the government will be split.

Historically, if government control is split, that means gridlock in Washington. Gridlock is good for the markets because it means things don’t change, which reduces uncertainty for the market. In this case, it mostly reduces negative potential outcomes related to taxes.

Even if Biden does get the Senate and the House on his side, some of those new Senators will be coming from regions where they will need to walk a moderate political line. For example, recall how Joe Manchin of West Virginia has voted since he got elected in a very “purple” West Virginia, meaning while it votes democratically, it is more conservative.

This is why the idea of wholesale changes to the tax code undoing 40 years of lowering taxes is unlikely, even if there could be some cosmetic changes. Investors shouldn’t panic about the outcome even if, as the polls show, it’s likely to be a very positive electoral cycle for the Democratic party.

That being said, it is critical to understand the pressures to stock market valuations from high taxes in case there is a “blue sweep” in November. There are three reasons why higher taxes will negatively impact the market.

The first reason is the most obvious one. As corporate tax rates rise, the earnings a company makes in relation to their revenue will fall. Assuming factors like inflation stay the same, as more of a firm’s pretax profit is paid to the government, stock prices fall, assuming P/Es stay the same.

And yet, the real pressure to stock prices come because P/E doesn’t stay the same if tax rates change, the warranted P/E changes too.

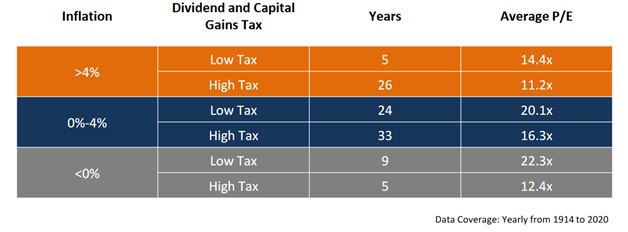

The second reason market valuations would fall is due to how taxes on dividends and capital gains impact P/E. As investors pay a greater percentage of their capital gains and dividends in taxes, they need a higher pretax return to make the same amount of money.

If an investor’s goal is to make a 10% gain in the market, in a market with a 0% capital gains tax rate, investors just need the market to rise 10%. However, if there is a 20% capital gains tax, to reach that same 10% return, the pretax capital gains has to be 12.5%, since 20% of that gain (2.5%) will go to the government.

The pretax returns needed for investors to make their previous return will continue to rise as taxes climb. This means investors will pay a lower P/E ratio for any company they buy, driving down market valuations. Because you need to start with a lower P/E to justify higher stock appreciation, all else being equal.

The third reason is the impact of taxes on nominal gains, meaning gains not adjusted for inflation. This is why taxes and inflation together are key drivers of stock market valuations.

If an investor has a 10% pretax gain, but inflation is 10%…they didn’t actually make any money. If they now have to pay a 20% capital gains tax, the nominal (not inflation adjusted) after-tax gain is 8%. Adjusted for the 10% inflation rate this investor lost around 2% on a real basis.

This is why understanding taxes and inflation is so important to understanding market valuations. In total, these three interacting impacts of taxation directly affect P/E ratios of the stock market, all other factors being equal.

As you can see below, if inflation remained constant between 0% and 4%, the U.S. moving from a low tax environment to a high tax environment would lower average P/E ratios from 20.1x to 16.3x. That could mean a 20% drop or more in the market!

However, even if Biden wins as part of a blue sweep and tax increases are coming, more important for investors, it does not mean the market will immediately plummet.

The market won’t plummet immediately after a theoretical Biden win partly due to how wealth advisors think about changing an investor’s entire portfolio strategy on the potential for a future tax hike.

If a wealth manager sold an entire portfolio’s worth of capital gains at the rumor of higher taxes, and the bill never comes to fruition, clients will be unhappy they paid so much capital gains tax for nothing.

This means fund managers, advisors, and traders will wait until after a law is passed and they are able to read the fine print of the tax change before making any conclusions on changing their strategy. Even if it is clear taxes are rising, the “how” is important before the markets react.

So while many might cry out in terror about the election in November, smarter investors will be patient and wait for the data, as the market as a whole will.

After all, we wouldn’t be the first to point out that the stock market has often done very well in Democractic administrations as well as Republican ones. If there’s a gridlocked DC, that’s generally great for the stock market, no matter who is living in 1600 Pennsylvania Ave.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research