Investors May be Too Excited About E-Commerce’s Impact on This Business

The rise of e-commerce has doomed many great brands of the past 100 years. Sears and Kmart, Barney’s New York, Payless Shoes, Circuit City, Radio Shack, and Borders are just a few of the biggest names that have gone under.

As those retailers have gone away, other retail jobs have not appeared to replace them. It is the reason why malls have had to shift from store-based anchors to experiences, like restaurants, cinemas, even axe-throwing venues to keep themselves full.

Those jobs have vanished, but another industry has risen to take some of those jobs. From January 2017 through mid-2019, retail lost over 140,000 jobs, but the warehouse and transportation industry added over 430,000 jobs over the same period. Many of them specifically in warehouses powering e-commerce giants like Amazon.

Most people think of companies like Amazon (AMZN) when they think of those warehouses, but in reality most warehouses are not owned by the retailers themselves. They’re owned by Real Estate Investment Trusts (REITs) and other owners.

Companies like Prologis (PLD), a REIT focused specifically on logistics real estate.

Because of excitement about Prologis’ positioning as a leader in the logistics space as the e-commerce business booms, Prologis stock is up 70% since early 2017. The market is pricing Prologis to make mint from the e-commerce revolution.

But after this run, market expectations for Prologis have gotten excessively high. While Prologis is in an exciting market, REITs rarely earn a return significantly above 5% levels, the long-run corporate average. The real estate market is just too efficiently priced to find wildly mispriced assets. The market right now is pricing Prologis to see returns basically double to historic peaks, and double that 5% level.

But Prologis management is growing more concerned about their outlook for the company, in particular about warehouse demand, weather, and the cost of their coastal development initiatives. High expectations and growing management pessimism may put pressure on the stock.

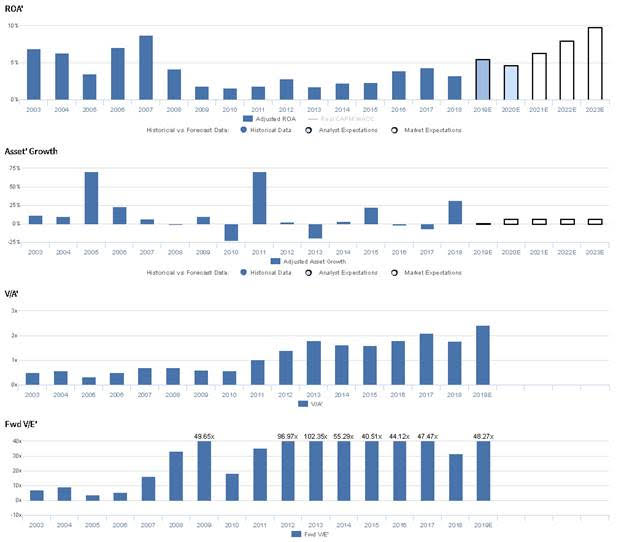

Market expectations are for Uniform ROA to reach all time highs, but management may be concerned about warehouse demand, weather, and coastal development

PLD currently trades at historical highs relative to UAFRS-based (Uniform) Assets, with a 2.4x Uniform P/B. At these levels, the market is pricing in expectations for Uniform ROA to expand from 3% in 2018 to 10% by 2023, accompanied by 6% Uniform Asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to only improve to 5% levels through 2020, accompanied by 1% Uniform Asset growth.

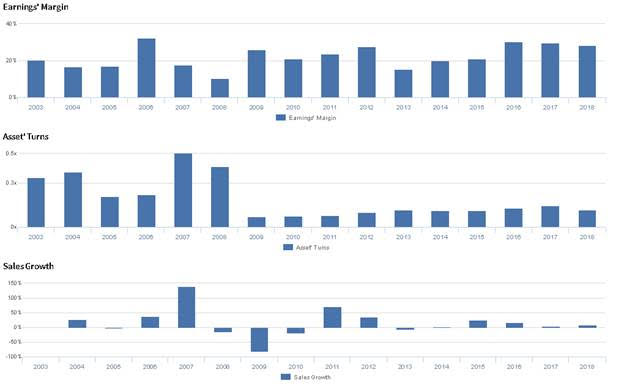

Historically, PLD has seen somewhat cyclical but overall fading profitability. After falling from 7% in 2003 to 4% in 2005, Uniform ROA improved to 9% in 2007, and slid to 2%-3% levels from 2009 to 2015. Then, Uniform ROA improved to 4% in 2017, before falling to 3% in 2018. Meanwhile, Uniform Asset growth has been volatile, positive in 11 of the past 16 years, ranging from -22% to 71%.

Performance Drivers – Sales, Margins, and Turns

Trends in Uniform ROA have been driven mainly by trends in Uniform Earnings Margin and, to a lesser extent, Uniform Asset Turns. After falling from 20% in 2003 to 17% levels in 2004-2005, Uniform Margins improved to 32% in 2006, slid to 10% in 2008, and sustained 21%-28% levels from 2009 to 2012. Then, Uniform Margins fell to 15% in 2013 before improving to 28%-30% levels from 2016-2018. Meanwhile, after fading from 0.3x-0.4x levels in 2003-2004 to 0.2x levels in 2005-2006, Uniform Turns improved to 0.5x in 2007. However, Uniform Turns then fell to 0.1x levels from 2009 to 2018. At current valuations, markets are pricing in expectations for significant expansion in both Uniform Earnings Margins and Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident their big data initiatives will drive incremental earnings. However, they are also confident e-commerce growth will reduce demand for their warehouses, and they may lack confidence in their ability to provide space where customers desire. Furthermore, they may be exaggerating the rigor of their WACC requirements, and they may be concerned about the impact of weather on their construction schedule. Finally, they may be concerned about U.S. market fundamentals and about the cost of replacing land in their coastal developments.

UAFRS VS As-Reported

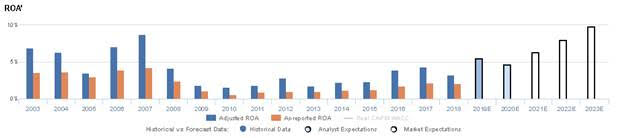

Uniform Accounting metrics also highlight a significantly different fundamental picture for PLD than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate PLD’s profitability. For example, as-reported ROA for PLD was near 2% levels in 2018, materially lower than Uniform ROA of 3%, making PLD appear to be a much weaker business than real economic metrics highlight. Moreover, from 2013-2017, as-reported ROA has been nearly half of Uniform ROA, distorting the market’s perception of the firm’s historical profitability trends.

Today’s Tearsheet

Today’s tearsheet is for Total S.A.. Total trades in line with market average valuations. The company has recently had Uniform EPS growth around 15%. EPS growth is forecast to moderate, dipping in 2019 before recovering strong in 2020. At current valuations, the market is similarly pricing in the company having neutral earnings growth going forward, below forecasts, if the company sees a recovery in 2020.

The company’s earnings growth for 2019 is at the high end of peer average levels, but the company is trading at peer average valuations. The company has weak returns, but no risks to their dividend.

Regards,

Joel Litman

Chief Investment Strategist