Market valuations are pricing in a permanent slowdown in economic growth, but history says that’s unrealistic

After the recent market skid, valuations and embedded expectations have fallen to their lowest levels in years.

In fact, current market valuations are pricing in expectations for growth and returns to remain near decade lows into perpetuity.

That’s probably an overreaction, and it could be an indicator that it’s a great time to buy into the market.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

In last week’s Monday Macro Report, we highlighted that the credit market is flashing “all-clear” for a faster rebound than during most other recessions.

Banks are still lending, most American corporations aren’t in any near-term credit risk even without any cash coming in the tills, and most parts of the economy should be able to return to business as usual as soon as it’s safe to do so.

It’s all well and good to know the credit markets are healthy, but what does that have to do with the stock market?

In reality, it has everything to do with the stock market.

One of our research tenets here at Valens is “You can’t be a great equity investor without being a solid credit analyst.”

The idea was passed down to us from Mitch Julis, one of the world’s great value investors.

In a lot of ways, the credit market informs, and even drives, the equity market.

As we’ve mentioned repeatedly, just about every modern recession has been preceded by a credit crunch. Likewise, healthy credit markets are one of the top drivers of strong equity markets.

With that in mind, this week, we’re looking at equity market signals at the aggregate level.

We’re well into Q1 earnings season for most U.S. corporations, meaning we’ve finally had time to ingest and analyze most of the full-year 2019 results.

For context, 2019 has high standards to uphold. 2018 was about as strong of a year as we’ve ever seen for U.S. corporate performance.

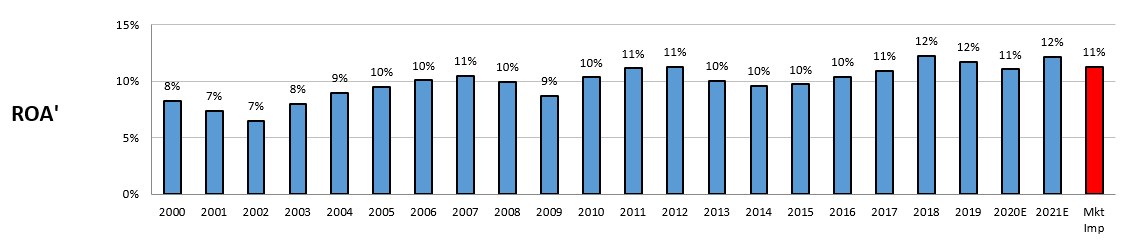

Not only did average Uniform ROA reach 12%, which represents both a 20-year high and twice the long-term corporate average, but U.S. corporations also grew by 8% in aggregate.

By any account, that’s a year for the record books and it helps explain why the markets were so strong in 2019. U.S. corporations were carrying a lot of fundamental momentum until the recent pandemic, and yet shares are still off more than 15% from pre-coronavirus highs.

While 2020 will undoubtedly end up worse than most people expected prior to the start of the year, looking at how U.S. corporations held up through 2019 may give us an idea of what to expect once widespread shutdowns subside.

Starting with aggregate Uniform ROA, it’s clear the market maintained its momentum in 2019. It was another near-record year for U.S. profitability, with the average company again returning 12% on its assets.

Even after companies have started guiding lower, profitability is only expected to drop to 11% in 2020. That said, current valuations expect profitability to remain at 11% into perpetuity. Investors are expecting the economy to fail to shake off the impact of coronavirus for years to come.

The above chart is already telling that equity markets may have overreacted, but that’s only half of the story.

When we look at average Uniform asset growth for U.S. corporations, we can see just how overly bearish current expectations are.

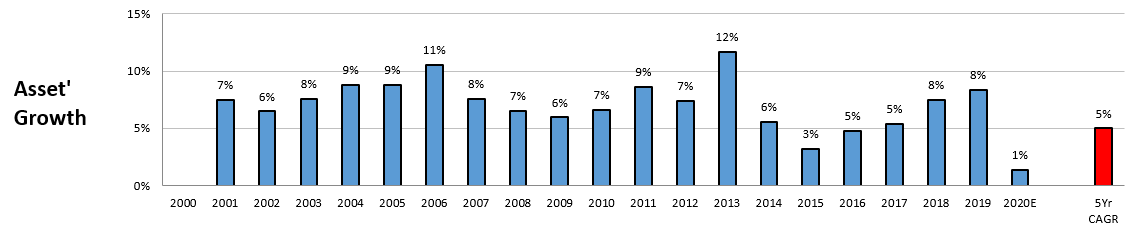

2019 was another fantastic year for corporate growth. In fact, U.S. corporations more than offset the slight skid in Uniform ROA with even stronger Uniform asset growth, again coming in around 8%.

While estimates are for growth to come to a virtual standstill in 2020, with just 1% growth, market-implied five-year growth shows how bearish current expectations are.

Currently, the market expects U.S. corporations to only manage 5% growth annually for the next five years.

For context, growth never fell as low as 5% during the Great Recession, and we’ve only had three years with 5% growth or less in the past two decades.

Even if U.S. corporations don’t grow at all this year, it feels far too bearish to expect that trend to continue, considering what strong momentum the economy had entering Q1 of this year.

Furthermore, as we discussed above, credit markets tend to inform equity markets. Considering how sound credit markets look right now, it’s unreasonable to expect corporations to put off growth indefinitely.

As investors start to realize how cheap the market is, it’s only a matter of time before valuations begin creeping back up to reasonable levels.

All the best, as always,

Joel Litman

Chief Investment Strategist

at Valens Research