This key credit metric is not rising the way it normally does in a recession, and that’s important for equity investors

Towards the end of Q1 2020, C&I loan charge-offs started rising across the U.S. That’s to be expected during the pandemic, and it’s likely not the end of the story.

In the coming months, charge-offs are likely to keep rising as they have in each of the last three recessions. That doesn’t mean it’s time for banks or investors to panic.

Today, we’ll dive into what makes this recession unique and why charge-offs and lending may recover faster than in most recessions.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Banks, at their core, act like any other business.

Their goal is to ethically maximize returns, as highlighted as the first tenet of the Return Driven Strategy framework.

In the course of operating a bank, executives and business managers are constantly calculating the risk-reward payoff of new products.

The only difference between banks and other businesses is that the product banks are “selling” is generally debt.

Debt and loans present a unique moral hazard for banks—more loans and bigger loans mean a larger potential payout. They also come at the expense of higher risk and issues.

As a result, banks tend to be inherently more risk aware than most other businesses.

Part of calculating how much debt a bank can issue is to calculate their expected charge-off rates and loan reserves.

These numbers fluctuate constantly, and banks have to be sensitive to these changes. When customers, including consumers and businesses, start defaulting on their loan payments, banks have to react quickly to preserve their capital.

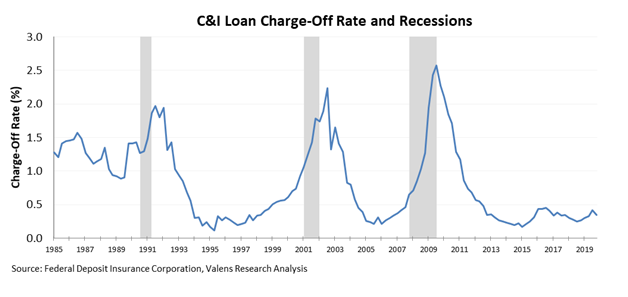

Unsurprisingly, leading up to and during financial recessions, charge-off rates rise quickly. For each of the last three recessions dating back to 1985, we’ve seen a spike in Commercial and Industrial (“C&I”) loan charge-off rates.

Since the Great Recession, banks have done a good job limiting their charge-offs. Charge-off rates have remained below 0.5% consistently since 2012. Thanks to positive economic growth, low interest rates that allow refinancing, and solid underwriting, banks haven’t had lending quality issues.

That said, despite anybody’s best efforts or forecasts, nobody could have predicted the impact of coronavirus in advance.

Many businesses that would be considered safe under any normal circumstance have suddenly lost all their cash flows, and some can’t afford to pay their loans.

Through Q1, we’ve started seeing an uptick in C&I charge-off rates. For the first time since 2012, the charge-off rate has risen above 0.5%. Don’t worry though…it’s only reached 0.6%.

While these levels are nearly at eight-year highs, they are not catastrophic.

As we’ve discussed in prior Investor Essentials Daily issues, the impact of government shutdowns was longer-term in Q2 compared to Q1, so we expect figures like charge-offs to continue rising.

That said, it’s not time to panic.

It’s likely to continue rising even into Q3, but doesn’t appear to be trending towards the levels normally seen heading in to and in the midst of recessions.

And that’s because, as we highlighted on June 8th, we’re unlikely to face a liquidity crisis in the coming months.

Not only has the government implemented several loan and stimulus programs to help bridge the gap until businesses are able to come back online.

Additionally, as we highlighted on May 11th, corporations have stronger balance sheets and longer debt runways than in any other recent recession.

All things considered, our economy is in a good spot to recover quickly so long as the economy begins opening up in the near-term.

Rising C&I charge offs over the next two quarters are unlikely to sustain much longer than that, or spike to normal recessionary peaks, which means banks shouldn’t need to get even more restrictive on their lending. And that means lending will stay open, priming the economy to grow once things reopen.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research