This macro hedge fund thrives during times of crisis, our Market Phase Cycle is telling us now might not be the time to bet on them

Macro hedge funds seek to take advantage of broad political or economic trends. They make bets based on the outcomes of events such as potential rate cuts, other central bank actions, and elections.

Today’s fund is one of the most famous macro funds in history, with a founder that has the ear of the Federal Reserve. While the fund has struggled in a more low volatile environment, it has shown signs of life during the pandemic and recession.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

There are few investors who can say they have the attention of the Federal Reserve. Alan Howard, co-founder of hedge fund Brevan Howard, is able to make this exact claim. Howard was previously on the Investor Advisory Committee on Financial Markets, along with famed macro investors David Tepper, Ray Dalio, and Paul Tudor Jones, among others. Members of the committee speak directly to Fed presidents and hold large amounts of influence.

Historically, Brevan Howard has been one of the largest and most successful macro hedge funds on Wall Street. It has garnered a reputation as one of the smartest of macro investing shops.

Brevan Howard rarely invests in equities, instead opting for interest rate swaps, currencies, commodities, and other assets. It focuses on taking advantage of broad macro trends, rather than individual mispricings.

The fund is well respected for its impressive risk controls. Senior leaders were known to push traders to hedge or trim positions seen as too risky. Thus, it is no surprise that former Chief Risk Officer Aron Landy was promoted to CEO in 2019.

This focus on risk management came into play during the early stages of the Great Recession. In 2007, Howard suspected mortgage problems would continue to grow, decreasing banks willingness to finance leverage at hedge funds.

The firm cut its bond portfolio to $10 billion from $50 billion and sharply decreased its credit default swaps. The moves paid off as Brevan’s Master Fund ended 2008 up 20%, compared to a -19% return for the average hedge fund.

Brevan Howard has multiple funds, often run by individual PMs and traders. Fund managers monitor macro trends to identify short-term (often 1-6 month) trades to profit from. Investments are often based on yield curves, spreads, and other temporary mispricings. Longer-term trades make option-style bets that benefit when a predicted action occurs such as a rate cut.

In recent years, the fund has lacked sufficient volatility to base trades on. Brevan Howard thrives off of big swings in the market, such as the financial crash in 2008. The fund improved 17% during the coronavirus induced market turmoil of March, contrary to most funds.

One has to wonder if Brevan Howard has a systematic process to identify its signals that are repeatable. What we have found at Valens is to have replicable insights from a macro perspective, there needs to be a consistent process like our Market Phase Cycle™

While it isn’t clear of the inner workings of Brevan Howard’s processes, it is telling that its funds spend so much time focusing on the credit markets. Credit market cycles are what drive the economy as a whole, one of the core drivers of the Market Phase Cycle™.

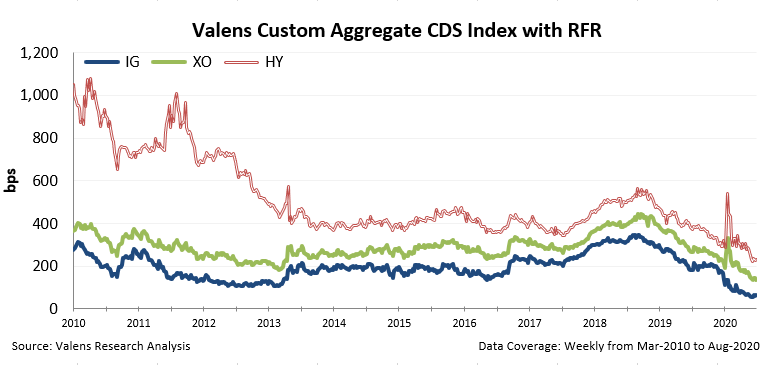

Credit markets power everything from economic growth to other markets such as currencies and equities. It is no wonder that many macro investors spend the most time looking at credit health.

Right now, as can be seen in the CDS Index chart, credit markets have seen significantly reduced spreads since April. The gap between high yield investment grade spreads continues to shrink, as the market is awash with liquidity.

Investors have to wonder if the time of the macro investor betting on volatility has dissipated as quickly as it began in March. Brevan Howard typically uses less liquid financial instruments such as derivatives to make trades. However, central banks have been flooding the markets with liquidity and suppressing volatility, limiting the ability to profit from these strategies.

Brevan Howard has reduced its assets under management and sits below $10 billion, allowing it to pursue smaller investments than during its $40 billion dollar hayday. It remains to be seen whether Brevan can recapture some of the magic it had during more volatile periods like 2008 or early 2020.

We’ll be watching our Market Phase Cycle™ to see if things start to signal that is changing.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research