Uniform Accounting helps show how this retailer is using the lessons learned by overcoming the “retail apocalypse” to navigate the pandemic

As Amazon threatened the retail world, this firm was able to pivot its strategies to avoid bankruptcy and the “retail apocalypse” by managing its credit risk.

Today, as COVID-19 and potentially long-lasting store shutdowns threaten retailers once again, sending credit investors into a panic, this firm’s prudent capital management still convinces credit markets that it ought to be viewed as low risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile to confirm this counterintuitive view.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Throughout the 2000s, electronics retailer Best Buy (BBY) was able to amass a large retail footprint. For years, the firm used its substantial size and economies of scale to deliver the best price possible to consumers.

However, in the early 2010s, the firm faced a growing and eventually seemingly insurmountable threat. Online retailers, namely Amazon (AMZN), were able to leverage an even larger supply chain network to provide cheaper prices than Best Buy. They could even ship products directly to a customer’s front door.

This led to a phenomenon known as “showrooming.” Consumers would go into Best Buy’s physical stores to test out expensive products and return home to actually buy them on Amazon. As showrooming grew in popularity, investors grew increasingly panicked.

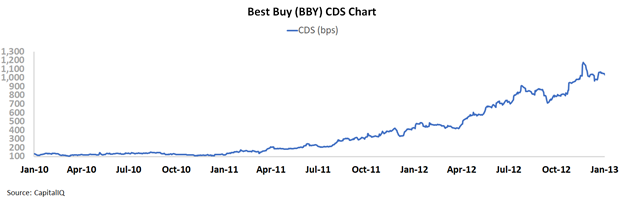

The following chart, detailing Best Buy’s credit default swap (CDS) prices, a value often referred to as a proxy for credit risk, showcases just how concerned investors, namely credit investors, were becoming during that time period.

Best Buy’s CDS widened from near 100bps levels seen throughout 2010—levels that would suggest the firm was an investment-grade name—to over 1,000bps in less than two years. That means the company’s bonds were yielding in excess of 10%, incredibly high levels.

At these spreads, the firm was being priced for bankruptcy, and if it did not adapt quickly, it would follow in the footsteps of Circuit City and countless other peers that could not survive the “retail apocalypse.”

To combat this fate, CEO Hubert Joy launched the “Renew Blue” initiative. The firm knew it could never compete directly with Amazon on prices, so it had to find new ways to stay relevant.

First, the firm offered price matching. When customers came to the stores to test out products, they would be incentivized to purchase in-store and get the product immediately instead of having to go home and wait days for the package to be delivered.

This selective pricing strategy allowed Best Buy to cushion its margins, as it didn’t have to slash pricing on all of its products. Just the ones that savvy customers wanted the best price for.

In addition, the firm decided to lean in on its “showroom” experience, as it already was a draw for customers. Through initiatives such as Magnolia, Best Buy created expansive set ups that allow customers to demo home-theater or surround-sound setups.

Best Buy also partnered with Microsoft and Samsung to create smartphone showrooms. The phone manufacturers paid for the space, which reduced Best Buy’s costs and boosted revenues.

Moreover, Best Buy focused on cutting administrative costs and doubled down on sustainable strengths, such as its in-home consultation and helpdesk service, Geek Squad, to improve its customer loyalty.

However, most importantly for creditors, these initiatives, as well as other aspects of “Renew Blue,” helped the firm manage its capital structure.

While other retailers often flirt with higher credit risk and credit problems by building massive debt headwalls, Best Buy has been prudent about managing its credit, spreading out and limiting its debt obligations, and making sure it maintains cash reserves.

For instance, as the COVID-19 pandemic threatens the firm with potentially long-lasting store closures, Best Buy was able to draw down its $1.25 billion revolving credit facility to comfortably cover its obligations until social distancing measures are finally reversed.

Furthermore, as the revolvers do not expire for another three years, the firm has ample time to generate enough cash flow to pay down this obligation, even if the impact of the pandemic lasts longer than anticipated.

That is part of the reason why, today, as investors are once again panicked about credit risk for retailers, including some of Best Buy’s largest peers, the firm remains a safe credit. Even as almost the entire economy is shut down, Best Buy only has a CDS of 68bps, well below the levels seen before Amazon materially threatened the traditional retail world.

Tightening of Bond Spreads Likely Given BBY’s Substantial Liquidity

Cash bond markets are grossly overstating credit risk with a cash bond YTW of 3.643% relative to an Intrinsic YTW of 0.923%, while CDS markets are accurately stating risk with a CDS of 68bps relative to an Intrinsic CDS of 31bps.

In addition, Moody’s is also accurately BBY’s credit risk, with its low-end investment grade Baa1 rating in line with Valens’ IG4+ (Baa1) rating.

Fundamental analysis highlights that BBY’s cash flows should comfortably exceed operating obligations in each year going forward.

In addition, the combination of the firm’s cash flows and cash on hand should be sufficient to cover all obligations including debt maturities through 2027.

Moreover, BBY’s robust 172% recovery rate and sizable market capitalization should allow the firm to access credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for credit holders. BBY’s management compensation framework should drive them to focus on top-line growth and margins, which should lead to Uniform ROA expansion.

In addition, management members have low change-in-control compensation, indicating they are not likely to accept a buyout or sale of the firm, reducing event risk for creditors.

Furthermore, most management members hold material amounts of BBY equity relative to their average annual compensation, indicating they are well aligned with shareholders for long-term value creation. However, the lack of debt control metrics means that management could overleverage the balance sheet to finance growth.

Earnings Call Forensics™ of the firm’s Q4 2020 earnings call (2/27) highlights that management is confident they will continue to bring their deep customer engagement expertise to commercialize new technology and that computer gaming has been a successful portion of their Toys category.

In addition, they are confident about the progress of their Teen Tech Centers initiative and that they invested in a new surrogacy assistance benefit for employees. However, management may be exaggerating their ability to address online and in-store customer needs through digital technologies and improve the pick-up in-store customer experience.

Furthermore, they may be exaggerating the progress of their “Building the New Blue” strategy, their technology innovation opportunities, and the sustainability of a favorable consumer environment.

Moreover, management may lack confidence in their ability to continue to reduce SG&A expense, sustain operating income margins, and generate cost savings from efficiency investments.

Additionally, they may have concerns about the impact of COVID-19 on H1 2020 results and their ability to coordinate with partners, and they may be downplaying concerns about changes to the global consumer electronics market once the pandemic ends.

Finally, management may lack confidence in their ability to drive new Total Tech Support memberships and predict changing consumer trends.

SUMMARY and Best Buy Co., Inc. Tearsheet

As the Uniform Accounting tearsheet for Best Buy Co., Inc. (BBY:USA) highlights, the company trades at a 17.2x Uniform P/E, which is below global corporate average valuation levels, but around its historical average valuations.

Moderate P/E’s only require moderate EPS growth to sustain them. That said, in the case of Best Buy, the company has recently shown a 16% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Best Buy’s Wall Street analyst-driven forecast projects a 19% shrinkage in earnings in 2021 followed by 19% growth in 2022.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $72 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for Best Buy, the company would have to have Uniform earnings shrink by 8% or less each year over the next three years.

Wall Street analysts’ expectations for Best Buy’s earnings growth are above what the current stock market valuation requires.

Meanwhile, Best Buy’s Uniform earnings growth is below peer average levels, and the company is also trading below peer valuations.

In addition, the company’s earnings power is 2x corporate averages. As a result, total obligations, including debt maturities, maintenance capex, and dividends, are above total cash flows, signaling a low risk to its dividend or operations.

To summarize, Best Buy is expected to see below average Uniform earnings growth in 2021, which is expected to inflect positively in 2021. Furthermore, the company is trading below peer valuations, in line with having earnings growth that is below peer averages.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research