Uniform Accounting shows how this resort business has unlocked the power of season tickets for strong profitability

This ski resort company has embraced the season ticket model fad to boost profitability.

As-reported metrics would have you believe this company’s strategy has left it with no growth in recent years, but true UAFRS (Uniform) based analysis shows the firm’s real profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The software as a service (SaaS) model has become extremely popular in recent years. Adobe (ADBE) popularized the model in the early 2010s and it has spread to other firms like Slack (WORK), Salesforce (CRM), Autodesk (ADSK), and even Microsoft (MSFT).

The genius of the model is that it turns one-time customers into recurring customers. It does this by requiring regular payments to use a product. This makes the product much stickier and profitable in the long-run.

While it gets lots of press, the SaaS model is not the only pricing strategy that has gotten highly popular in the last few years. In the past decade, many businesses have looked at how to generate recurring revenue from customers or “expand wallet share” in ways that make customers feel like they’re getting a deal.

The season ticket model is another model that has become more widespread in this vein.

Although offered well before this decade by experience-based businesses, a few businesses helped re-popularize the model recently. Six Flags (SIX) and other theme parks have become the standard bearers of the model in recent years. They have done this through aggressively promoting season ticketing.

The idea behind season tickets is to price them extremely low. This way, someone who is only at the park once may wonder if it is worth buying. Oftentimes, the price is so low the customer will only have to return to the park one or two more times to make the purchase economically smart.

“If there’s any chance I might come back, I guess I should just buy it,” the logic goes.

Depending on the type of season pass a customer buys, if a customer does buy a season pass, they gain access to many locations around the country. Some users will still only go to the park once, and the firm makes much more money from said customer. However, those who embrace the season ticket model and come back will still benefit the business because they spend so much more on ancillary products with every trip.

Another business to aggressively embrace the model is ski resorts, Vail Resorts (MTN) in particular. This ski resort business has rolled up many different ski mountains in recent years and now owns resorts from its home base in Colorado to California, New Hampshire, and Australia.

With so many ski resorts in Vail’s portfolio, it now offers its own season ticket, the Epic pass. In order to get people to embrace the model, Vail offers unrestricted access to nearly 20 mountains and additional access to 46 other resorts.

Most subscribers will never visit most of the mountains, since they are located all over the world. However, the opportunity to use all the mountains is enough to get customers to jump for the Epic pass.

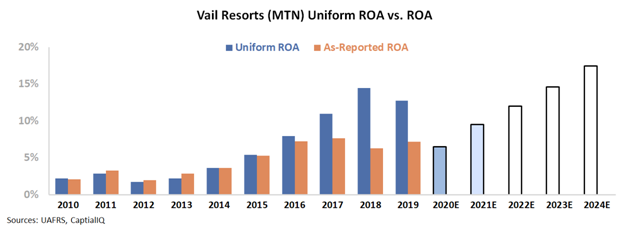

The Epic pass began earlier this decade and as-reported return on assets (ROA) shows it worked initially. ROA grew from 2% in 2012 to 7% in 2016. However, profitability metrics have not improved since, leaving investors to wonder if the strategy’s positive effects have already played out.

However, this picture of Vail’s performance is inaccurate, pulled down by distortions in as-reported accounting. Due to GAAP’s treatment of interest expense and goodwill & intangibles, among other distortions, the market has missed the mark on the success of this firm.

The Uniform ROA for Vail has in reality continued to improve in recent years. Uniform ROA was 2% in 2012 and reached 15% in 2018, before falling slightly to 13% last year.

With the help of Uniform Accounting, it is clear Vail has been able to use the season ticket strategy to turn a high fixed cost and asset intensive business into a much more profitable company.

However, in order to fully understand the stock, we must look at valuations to understand expectations for future performance. We can use the Embedded Expectations Analysis to see specifically what the market expects of Vail.

The chart below explains the company’s historical corporate performance levels, in terms of Uniform ROA (dark blue bars) versus what Wall Street sell-side analysts think the company is going to do in the next two years (light blue bars) and what the market is pricing in at current valuations (white bars).

The chart shows sell-side analysts are expecting a material drop this year in profitability in the wake of the coronavirus pandemic. Many ski resorts were forced to close down in March and cut the season short. However, analysts are also expecting Uniform ROA to rebound to 9% next year, only slightly below 2019 profitability levels.

In the future, the market is pricing in consistent Uniform ROA improvement, expecting the firm to reach an ROA of 17% in 2024. This is fairly significant growth, over two times higher than expected 2020 ROA. However, it is only 2% higher than the 2018 level. If Vail is able to continue growing its Epic pass once the pandemic is behind us, the firm may be able to meet expectations.

Vail has fully embraced the season ticket model and Uniform Accounting is able to show that the firm has correctly executed the strategy. The coronavirus pandemic has caused headwinds and the company will need to continue to grow in order to justify its valuation, yet if Vail is able to continue growing, it may live up to the market’s lofty expectations.

Vail Resorts, Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to reach new peaks, but management may have concerns about macro headwinds, season passes, and costs

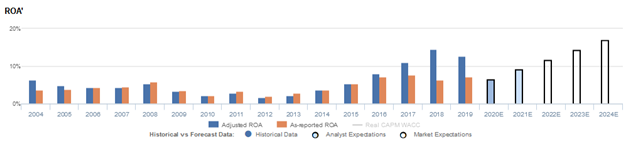

MTN currently trades above corporate averages relative to Uniform earnings, with a 43.1x Uniform P/E (Fwd V/E’). At these levels, the market is pricing in expectations for Uniform ROA to improve from 13% in 2019 to 17% in 2024, accompanied by 3% Uniform asset growth going forward.

Meanwhile, analysts have bearish expectations, projecting Uniform ROA to contract to 9% by 2021, accompanied by 4% Uniform asset shrinkage.

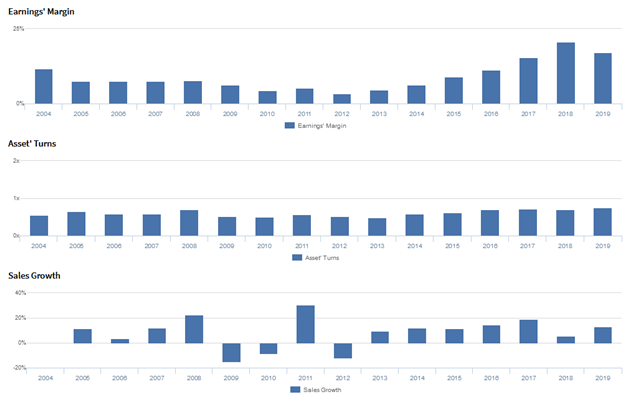

Historically, MTN had seen near cost-of-capital returns, before experiencing a significant spike in profitability recently.

After falling from 6% in 2004 to 4%-5% levels in 2005-2008, Uniform ROA compressed to 2%-3% lows in 2009-2013 before steadily rebounding to a peak of 15% in 2018, as the firm was able to raise its prices and accelerate its season pass program following the acquisitions of Canyons Resort, Park City Mountain Resort, and other notable ski destinations, starting in 2013. Since then, Uniform ROA has faded to 13% in 2019.

Meanwhile, Uniform asset growth has been historically volatile, positive in eleven of the past sixteen years, while ranging from -8% to 14%.

Performance Drivers – Sales, Margins, and Turns

Trends in Uniform ROA have been driven primarily by trends in Uniform earnings margins, coupled with stable Uniform asset turns.

After gradually declining from 12% in 2004 to a low of 3% in 2012, Uniform margins recovered to 21% in 2018 before compressing to 17% in 2019.

Meanwhile, since 2004, Uniform turns have remained at 0.5x-0.7x levels through 2019.

At current valuations, markets are pricing in expectations for Uniform margins to climb to new peaks, accompanied by improvements in Uniform turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q2 2020 earnings call highlights that management is confident they will continue to provide a full comprehensive experience in all of their resorts, that the Northeast Value Pass is delivering more value to their guests, and that their Park City resort’s strong performance somewhat offset weaker post-holiday performance across Colorado resorts.

However, they may have concerns about sluggish growth in their Vail and Breckenridge resorts, coronavirus-related macroeconomic headwinds, and the potential of the Whistler Blackcomb Day Pass.

In addition, they may be exaggerating the strength of their season pass program, their ability to offer value across-the-board, and the speed at which demand recovers when skiing conditions improve.

Moreover, they may lack confidence in their ability to sustain Resort EBITDA improvements and convert lift ticket purchasers and new prospective guests to their advanced products.

Furthermore, they may be downplaying concerns about their inability to reduce fixed costs in their Mountain segment, and they may be overstating the progress of their automated digital market platform implementation.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for MTN than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate MTN’s profitability. For example, as-reported ROA for MTN was 7% in 2019, substantially lower than Uniform ROA of 13%, making MTN appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2016, as-reported ROA has remained at 6%-8% levels through 2019, while Uniform ROA has expanded from 8% to 13% over the same timeframe, directionally distorting the market’s perception of the firm’s recent profitability trends.

SUMMARY and Vail Resorts Tearsheet

As the Uniform Accounting tearsheet for Vail Resorts, Inc. (MTN:USA) highlights, the Uniform P/E trades at 43.1x, which is above the global corporate average valuation levels but around its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Vail Resorts, the company has recently shown a 13% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Vail Resorts’ Wall Street analyst-driven forecast is a 66% EPS shrinkage in 2020, followed by a 81% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Vail Resorts’ $212 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 8% per year over the next three years. What Wall Street analysts expect for Vail Resorts’ earnings growth is below what the current stock market valuation requires in 2020, but above what the market requires in 2021.

Furthermore, the company’s earning power is 2x corporate average. However, cash flows are below their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals an average credit and dividend risk.

To conclude, Vail Resorts’ Uniform earnings growth is in line with its peer averages. Also, the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research