Although this company may thrive exiting the pandemic, investors may need to stay away anyway

This company has been able to survive the pandemic despite operating in a competitive industry with many macroeconomic tailwinds. But can it now thrive in a post-pandemic world?

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Now that 2020 is behind us, it’s clear the recovery from the pandemic has been uneven. While many industries such as travel and leisure have struggled over the past year throughout the pandemic, many other areas of the economy have flourished.

Surprisingly for some, one industry that has been left behind are the hospitals. Voluntary procedures such as hip replacements or complex surgeries are the money makers for hospitals. However, these activities had to be put on hold to make way for pandemic treatments.

At first glance, it appears one of the biggest public hospitals is positioned well for a “survive and thrive” story. By surviving through these tough times with smaller hospitals going bankrupt, this large company can consolidate the market and succeed with the pandemic abating.

This company is Community Health Systems (CYH).

However, despite these potential tailwinds and opportunities to thrive post-pandemic, Community Health Systems’ stock price is still roughly 75% lower than its all-time highs from 2015.

As a result, investors may think this is the time to buy before the small 2021 surge continues.

Let’s take a closer look below.

To understand what valuations are telling us about Community Health, we can use our Embedded Expectations Framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model, which takes assumptions about the future and produces the “intrinsic value” of the stock.

However, here at Valens we know models with garbage-in assumptions only come out as garbage. Therefore, we’ve turned the DCF model on its head with our Embedded Expectations Framework. Here, we use the current stock price to determine what returns the market expects.

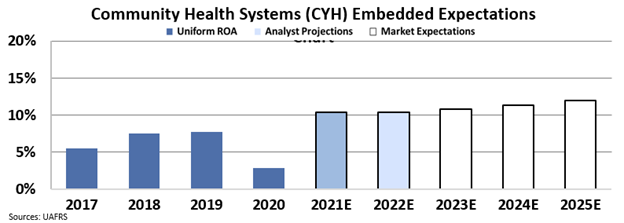

In the chart below, the dark blue bars represent Community Health Systems’ historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how the company’s ROA will shift in the next five years.

Wall Street analysts are expecting the company’s Uniform ROA to leap to 10% levels in 2021 and 2022. These would be the highest levels the company has seen in the past 15 years.

The market has even more bullish views, pricing in Uniform ROA to expand to 12% levels by 2025, accompanied by 8% Uniform asset shrinkage going forward.

While Community Health Systems is poised to see a performance increase, investors may already be pricing in the best possible scenario with limited upside.

A great company doesn’t always make a great stock. Looking at the above may further prove this point. As a result, investors may want to avoid the stock even if the company thrives after surviving the pandemic.

SUMMARY and Community Health Systems Tearsheet

As the Uniform Accounting tearsheet for Community Health Systems (CYH:USA) highlights, the Uniform P/E trades at 15.1x, which is below the global corporate average of 23.7x and its own historical average of 26.3x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Community Health, the company has recently shown a 242% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Community Health’s Wall Street analyst-driven forecast is a 101% EPS decline in 2021 and 880% EPS growth in 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Community Health’s $14 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 21% annually over the next three years. What Wall Street analysts expect for Community Health’s earnings growth is below what the current stock market valuation requires in 2021 and above this requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Also, intrinsic credit risk is 840bps above the risk-free rate and cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high credit risk.

To conclude, Community Health’s Uniform earnings growth is below its peer averages and the company is also trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research