As-reported financials give this educational institution a passing grade, Uniform Accounting shows it’s actually failing badly

Higher education is a highly competitive industry, with over 4,000 institutions competing in the US. However, the reward for the college that can innovate is sizable.

As-reported metrics make it look like this company is starting to succeed in its innovation efforts to differentiate itself in the higher education market.

However, UAFRS shows how successful this strategy really is after adjusting for ROA distortions.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

As some of our regular readers may know, we often teach classes at the Hult University in Boston. Through our experience in teaching, we have firsthand knowledge of how higher education has been innovating over the past twenty years. One example of this innovation comes from the story of the Hult Business School itself.

Back in 2001, the prestigious consulting firm AD Little was in dire straits. While it was the oldest consulting firm in the US, AD Little had taken on too much debt.

AD Little management had breached their debt covenants with Cerberus Capital Management, a private equity firm specializing in distressed debt.

Due to the restrictive clauses within the debt agreement, Cerberus was able to take control of the firm and break up its constituent parts, making a nice return on the value of the debt it had owned for AD Little. This process is reminiscent of what Edward, the main character of the film Pretty Woman, did for a living, or something seen in the movie Wall Street.

This is how the Arthur D. Little School of Management was spun off from AD Little. Sold to Swedish businessman Bertil Hult, he soon transformed the school into a full MBA program.

By leveraging the international presence of the former Arthur D. Little network, Hult created a global MBA program where students can travel around the world while completing their degree.

Hult is just one example of a school looking to innovate. There are over four thousand institutions of higher learning in the United States, and they are all competing with one another to draw student funds.

Higher education can be rewarding for the institutions that can pull ahead of the pack and attract top dollar. In a market that has seen little change, investors are looking for the next institution to break out of the pack.

Laureate Education (LAUR) is just one example of a firm looking to further innovate in the higher education space. Laureate operates as a network of undergraduate and graduate institutions.

Similar to Hult, Laureate is looking to benefit from the rising trend of globalization, through opening colleges under the Laureate umbrella around the world. Laurate operates more than 150 campuses in 10 countries, with a strategy to reduce their administrative costs through scale.

Through their web-based learning model, all Laureate affiliates are able to effectively share classroom resources and administrative tools. This network also allows Laureate to match students with internship opportunities around the world.

This leveraging of cost reduction and AI tools to improve learning has drawn significant investor interest over the past few years.

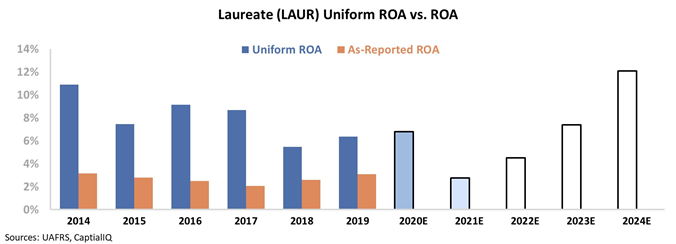

By looking at the as-reported ROA, it would appear that Laureate has begun to execute on this strategy of business development. Over the past 3 years, Laureate has consistently improved their ROA by 50%.

However, in reality, Laureate has not been successfully executing on their strategy of innovation. Rather than see profitability improve, Uniform ROA profitability has in fact contracted over the past three years, from 9% to 6% through 2019.

This company isn’t benefiting from its scale and seeing returns decline, it is seeing declining profitability as it struggles to improve execution.

Even with the company’s declining real returns, it appears that the market still has sizable expectations for Laureate. Thinking Laureate is seeing returns improve, the market is pricing the company for ROA to reach new highs by 2024, rising to over 12%.

With market valuations forecasting such aggressive ROA growth, Laureate would need to radically turn their business around to meet current market expectations.

Meanwhile, for higher education in 2020, even continuing current performance will be a challenge. Almost 40% of colleges have announced they will be pursuing an online plan for the fall semester, putting pressures on the typical business model of colleges.

With such sizable headwinds, Laureate looks set up to disappoint market expectations going forward.

Laureate Education, Inc. Embedded Expectations Analysis – Market expectations are for Uniform ROA to expand, but management may have concerns about capital allocation, Chile, and momentum

LAUR currently trades above corporate averages relative to Uniform earnings, with a 27.5x Uniform P/E (Fwd V/E′).

At these levels, the market is pricing in expectations for Uniform ROA to expand from 6% in 2019 to 11% in 2024, accompanied by 6% Uniform asset shrinkage going forward.

However, analysts have more bearish expectations, projecting Uniform ROA to fall to 3% levels through 2021, accompanied by 10% Uniform asset shrinkage.

As a provider of higher education mostly in Latin America, a highly competitive market in general, LAUR has historically seen somewhat muted profitability.

Prior to its IPO in 2017, Uniform ROA ranged from 7%-11% levels in 2013-2016. However, since then, Uniform ROA has faded to 6% lows in 2018-2019.

Meanwhile, Uniform asset growth has been mostly negative, positive in only one of the past six years, while ranging from -12% to 5%, as the firm continues to downsize its portfolio in efforts to deliver.

Performance Drivers – Sales, Margins, and Turns

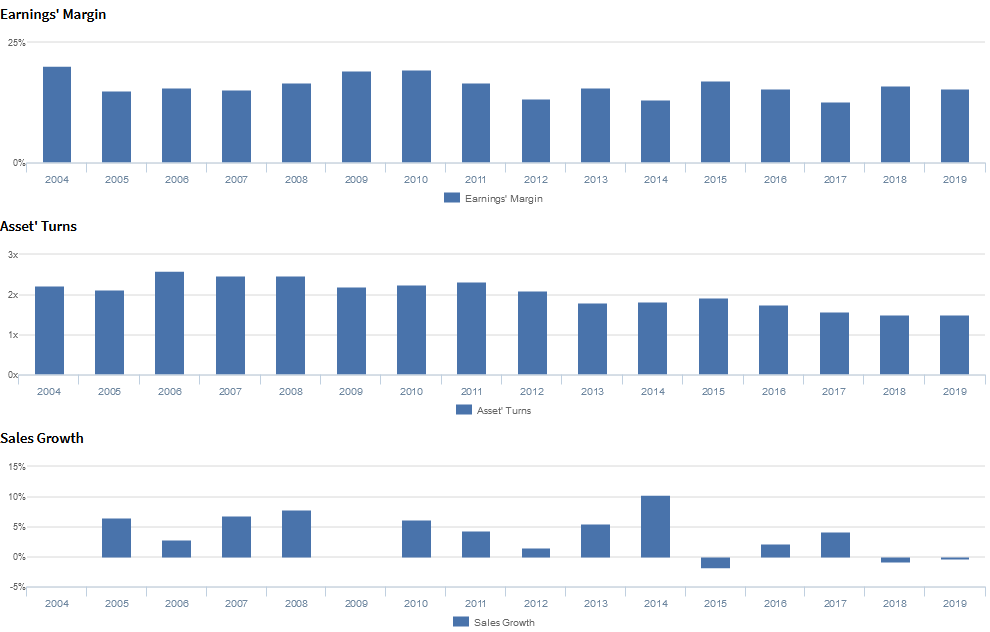

Trends in Uniform ROA have largely been driven by trends in Uniform earnings margins, slightly offset by trends in Uniform asset turns.

After improving from 8% in 2013 to 10% in 2014, Uniform earnings margins fell to 7% in 2015.

Thereafter, Uniform earnings margins recovered to a peak of 11% in 2017 before fading to 6% levels in 2018-2019.

Meanwhile, Uniform asset turns rose from 0.9x in 2013 to 1.2x in 2015 before compressing to 0.8x in 2017. Since then, Uniform asset turns have rebounded to 1.0x in 2019.

At current valuations, markets are pricing in expectations for an expansion in Uniform earnings margins and for a continuation of recent improvements in Uniform asset turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2019 earnings call highlights that management generated an excitement marker when saying that they saw improvements in student retention.

However, they may have concerns about their capital allocation strategy and the impact of disruptions in Chile, and they may lack confidence in their ability to sustain their domestic business momentum.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for LAUR than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly overstate LAUR’s margins, one of the primary drivers of profitability. For example, as-reported EBITDA margin for LAUR was 16% in 2019, materially higher than Uniform earnings margins of 6% in the same year, making LAUR appear to be a stronger business than real economic metrics highlight.

Moreover, as-reported margins have improved from 13% in 2017 to 16% in 2019, while Uniform earnings margins have faded from 11% to 6% in the same timeframe, directionally distorting the market’s perception of the firm’s recent performance.

SUMMARY and Laureate Education, Inc. Tearsheet

As the Uniform Accounting tearsheet for Laureate Education (LAUR) highlights, the Uniform P/E trades at 27.5x, which is above corporate average valuation levels but below its own recent historical P/Es.

High P/Es require high EPS growth to sustain them. In the case of Laureate Education, the company has recently shown a 213% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Laureate Education’s Wall Street analyst-driven forecast is a 1% growth in 2020, followed by a 354% shrinkage in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Laureate Education’s $10 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 1% each year over the next three years to justify current prices. What Wall Street analysts expect for Laureate Education’s earnings growth is in line with what the current stock market valuation requires in 2020 but far below that requirement in 2021.

Furthermore, the company’s earning power is 1x the corporate average. Also, the company’s intrinsic credit risk is 410bps above the risk-free rate and cash flows will fall short of debt headwalls after three years. Together, these signal moderate credit and dividend risk.

To conclude, Laureate Education’s Uniform earnings growth is above peer averages, but the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research