Today’s steel manufacturer is an industry outlier, and that may be good coming out of a recession

Though it is typically unorthodox to think of steel manufacturing companies as safe during a recession, this company may serve as an exception.

While it’s usually true the steel industry is not a monolith, there are exceptions to every rule.

It’s important to keep in mind how different customer bases impact risk and to understand a company’s real credit picture.

Also below, we highlight today’s company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

More often than not, the middle of a recession is not the time to get bullish on steel manufacturers.

In many ways, the steel industry is representative of the broader manufacturing space, which takes time recovering after a recession like the one brought on by the pandemic.

Even with ongoing infrastructure talks, steel companies don’t have much to look forward to. Most of the investments in these proposals revolve around projects like green energy infrastructure and broadband technology.

Steel manufacturers rely on more traditional infrastructure plans, investments like roads, rails, and bridges, for business stimulus.

That’s not always the case, though. The steel industry serves a number of end markets, including some niche markets that don’t line up as neatly with the rest of the economy.

For instance, Allegheny Technologies (ATI) focuses on specialized alloys generally used in areas like Aerospace and Defense.

As opposed to broad-based infrastructure projects, the Aerospace and Defense industry is less correlated with overall economic activity.

This end market accounts for roughly 45% of Allegheny’s revenue mix. The company also focuses on other specialized niches like medical and energy.

Consequently, the company’s demand cycle and pricing power are quite different from other traditional steel companies.

Allegheny Technologies is viewed as a much more value-add type of business by consumers.

As the aerospace industry begins to recover from the obstacles it faced in 2020 due to the pandemic, Allegheny Technologies is primed to perform better.

That said, rating agencies still appear bearish when rating this company’s overall credit profile.

S&P gives the company a highly speculative B rating, with the implied assumption of a 25%+ risk of default over the next five years.

Moody’s rates the company’s debt as a highly speculative B1 rating, also with the implied assumption of a 25%+ risk of default over the next five years.

As highlighted above, Allegheny is not being treated like a core supplier to the Aerospace and Defense industry… It’s being viewed like it is any other commodity steel maker.

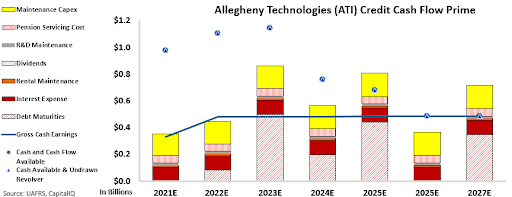

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Allegheny cash flows can sustain almost all operating obligations each year through 2027. Additionally, since the firm generates stronger cash flows than most low return steelmaker businesses, Allegheny Technologies finds itself in better credit health even when cash flows do not meet all debt obligations.

The company’s strong cash buffer means it should have relatively low risk in handling obligations.

Rather than a name in distress, Allegheny Technologies is actually in stable credit health. This is why S&P’s B and Moody’s B1 highly speculative ratings, with a 25%+ risk of default expectation do not make sense.

Using the CCFP analysis, Valens rates Allegheny Technologies as an XO rating. This rating is equivalent to a BBB- S&P rating and Baa3 Moody’s rating.

Additionally, this rating corresponds with a default rate under 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Uniform Accounting and the Credit Cash Flow Prime analysis highlights the true credit picture for Allegheny Technologies.

SUMMARY and Allegheny Technologies Incorporated Tearsheet

As the Uniform Accounting tearsheet for Allegheny Technologies Incorporated (ATI:USA) highlights, the Uniform P/E trades at 53.1x, which is above global corporate average valuation levels of 25.2x and its historical average valuations of 41.2x.

High P/Es require high EPS growth to sustain them. In the case of Allegheny, the company has recently shown a 93% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Allegheny’s Wall Street analyst-driven forecast is a 131% and EPS decline in 2021 before a robust 4,313% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Allegheny’s $22 stock price. These are often referred to as market embedded expectations.

Allegheny is being valued as if Uniform earnings will be growing 12% annually over the next three years. What Wall Street analysts expect for Allegheny’s earnings growth is below what the current stock market valuation requires in 2021 and above in 2022.

Furthermore, the company’s earning power is below the corporate average and cash flows and cash on hand are above its total obligations—including debt maturities and capex maintenance. Together, this signals a moderate credit risk.

To conclude, Allegheny’s Uniform earnings growth is below peer averages, and is trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research