Cable TV is dead, but this broadcaster has one last trick up its sleeve

While no two investors have the same opinions on investing philosophies or themes, one common belief is that the TV broadcasting business is a dying industry.

New technologies and platforms continue to disrupt the market, painting a picture of eventual irrelevancy similar to the radio or other traditional media platforms. However, this firm may be different than its peers.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Investors often disagree on the particulars of investing themes or market trends. In fact, while many investors do have similar strategies or techniques, many investors differ in the way they invest, whether it is rooted in investment philosophy or capital allocation strategies.

For example, not all investors believe the emergence of electric vehicles will change automotive profitability or how artificial intelligence (AI) can disrupt the market through replacing jobs.

Despite this, one investment theme almost universally accepted by investors is the downfall of TV broadcasting companies. Most investors agree TV broadcasting is a dying business.

Specifically, the emergence of streaming platforms such as YouTube TV or Disney+ that enable individuals to watch TV, cable news, or sporting events have significantly disrupted this space.

These factors, along with widespread internet access to quickly consume news, have pushed traditional broadcasting stations into a secular decline.

Additionally, as these broadcasting stations’ targeted demographic and majority user base continues to age, their businesses will continue to be pressured into a further secular decline.

Thanks to these major headwinds, it should come as no surprise that as-reported metrics for many TV broadcasting firms have been well below average.

One example of a company appearing to struggle in this space is Sinclair Broadcast Group (SBGI). The company operates as a media firm engaging in local news and sports broadcasting.

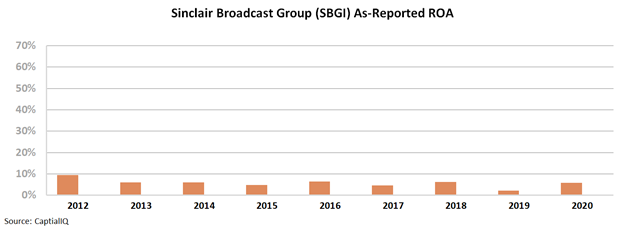

The company’s as-reported return on asset (ROA) levels showed below cost-of-capital levels of 2% in 2019. Since 2012, as-reported ROA has faded from 10% to just 6% levels by 2020.

However, the cord-cutting thesis is so widely believed, it may serve as an opportunity for investors if they focus on the few names set up to adapt.

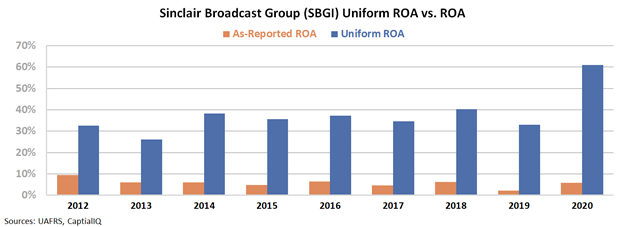

In reality, by looking at the Uniform Accounting metrics for Sinclair Broadcast Group, investors are able to see a different story in ROA levels.

For example, Uniform ROA was not 6% in 2020, it was actually at a robust 61% level.

Rather than a steady decrease, Uniform Metrics tell the story of a firm with steadily improving returns over the past nine years.

These strong ROA levels can be attributed to the company’s strategy in controlling costs and maximizing ad revenues, along with other avenues in its fight against the pressures in its space.

To gain a greater understanding about whether the market has priced in this above average performance, we can use our Embedded Expectations framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model, which takes assumptions about the future and produces the “intrinsic value” of the stock.

Here at Valens we know models with garbage-in assumptions only come out as garbage. Therefore, we’ve turned the DCF model on its head with our Embedded Expectations Framework. Here, we use the current stock price to determine what returns the market expects.

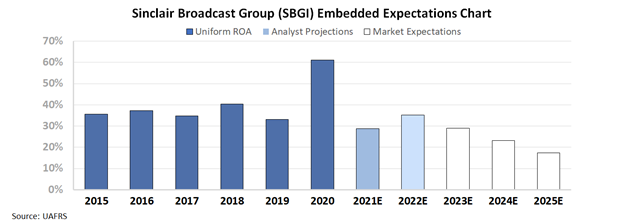

In the chart below, the dark blue bars represent Sinclair Broadcast Group’s historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how the company’s ROA will shift in the next five years.

Wall Street analysts are expecting Sinclair Broadcast Group’s Uniform ROA to return to 35% levels by 2022. They understand the firm’s resiliency through pressures in the broadcasting industry.

The market is pricing in Uniform ROA to do worse at 17% by 2025.

The market believes the company’s ROA is weak and expects it to keep falling from those weak levels. These expectations may be too pessimistic given the company’s continued resiliency in the face of weakening market trends.

Uniform Accounting demonstrates how successful Sinclair Broadcast Group has been in recent years battling secular headwinds.

More importantly, it highlights how dramatically wrong investor expectations are for the company, clouded by as-reported metrics.

While the TV broadcasting sector may be in decline, Sinclair Broadcast Group has stood out compared to the rest of the industry. If the company simply sustains current profitability levels, investors might want to keep its stock on their radar.

SUMMARY and Sinclair Broadcast Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Sinclair Broadcast Group, Inc. (SBGI:USA) highlights, the Uniform P/E trades at 15.3x, which is below the global corporate average of 25.2x, but above its own historical average of 11.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Sinclair Broadcast Group, the company has recently shown a 427% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Sinclair Broadcast Group’s Wall Street analyst-driven forecast is a 75% EPS decline in 2021, followed by a 100% EPS growth in 2022.he economy is growing strongly and picking up steam. They are raising rates to help moderate economic activity.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Sinclair Broadcast Group’s $30 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 15% annually over the next three years. What Wall Street analysts expect for Sinclair Broadcast Group’s earnings growth is below what the current stock market valuation requires in 2021, but way above that requirement in 2022.

Furthermore, the company’s earning power is 10x the long-run corporate average. Also, intrinsic credit risk is 440bps above the risk-free rate and cash flows and cash on hand are slightly above its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend and credit risk.

To conclude, Sinclair Broadcast Group’s Uniform earnings growth is below its peer averages, but the company is in line with average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research