Investors are forgetting the building blocks of the upcoming automation transformation

In today’s world, automation is progressing at an all-time high. As the world continues to change, one sure bet is the company supplying this automation wave.

Currently, the ratings agencies are showing a lack of understanding for this company’s credit risk, rating it at almost a high yield name without looking at its fundamentals.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Since the dawn of civilization, people have been scared of the consequences of automation. In the 19th century, a secret society of oath swearing members destroyed machinery to protest automation.

Known as “Luddites,” these textile workers have given us a handy byword for those opposing progress. However, human nature hasn’t changed in the past centuries.

Workers today are concerned the next wave of automation will make their own jobs obsolete. Truck drivers everywhere are fearing the adoption of self-driving trucks. Factory work will continue to be given to dedicated robots.

It’s not just blue collar jobs under threat, but white collar ones as well.

Developments in artificial intelligence and deep learning promise breakthroughs in data analytics. Technology like 5G enables better integration with the Internet of Things (IoT). Finally, the floodgates are opening for cloud computing, changing the way the software is developed.

Any one of these trends would have luddites quaking in their boots. Together, these technological advancements promise to continue disrupting the world we live in.

This is why a firm like Cadence Design Systems (CDNS), who supplies these technologies, is set to win.

Cadence Design Systems creates the software needed to design integrated circuits and full circuit boards. Without Cadence’s software, engineers would be unable to further improve computing.

However, the ratings agencies are missing the impressive competitive moat Cadence has created. The company is rated as a Baa2 by Moody’s, on the fringe of investment grade. This implies a default rate at around 10%.

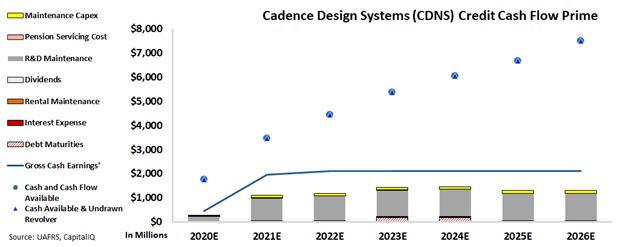

Moody’s wildly low rating is totally detached from reality. To understand the real credit risk, we can turn to our Credit Cash Flow Prime (CCFP) analysis.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As you can see below, Cadence Design Systems has plenty of liquidity, and therefore should have no issues handling its obligation going forward.

On top of this, even if the firm did not have access to this capital, cash flows alone exceed all obligations with a wide margin. With miniscule debt to speak of in the next six years, Cadence Design Systems should have no problem whatsoever paying back its creditors.

Rather than a name in distress, Cadence Design Systems is actually a cash flow machine. Furthermore, this is only likely to continue improving as automation trends continue to accelerate.

Using the CCFP analysis, Valens rates Cadence Design Systems as an investment grade IG3+ safe credit rating, equivalent to an A1 rating from Moody’s.

This rating corresponds to a default rate below 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Cadence’s credit risk profile is much safer than what rating agencies believe. Without any sizable obstacles in the firm’s path, ratings agencies are failing to take stock of this name.

By using Uniform Accounting, investors are able to quickly understand how a firm’s obligations stack up to its performance. When Moody’s or S&P overlook a quality name, investors can see the truth from themselves.

SUMMARY and Cadence Design Systems, Inc. Tearsheet

As the Uniform Accounting tearsheet for Cadence Design Systems, Inc. (CDNS:USA) highlights, the Uniform P/E trades at 46.8x, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. That said, in the case of Cadence Design, the company has recently shown a 20% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cadence Design’s Wall Street analyst-driven forecast is a 15% and 1% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cadence Design’s $145.68 stock price. These are often referred to as market embedded expectations.

To justify current valuation the company needs to grow its Uniform earnings by 21% per year over the next three years. What Wall Street analysts expect for Cadence Design’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 4x the long-run corporate averages. Also, cash flows and cash on hand are 3x of its total obligations—including debt maturities and capex maintenance. Together, this signals low credit risk.

To conclude, CDNS’s Uniform earnings growth is in line with its peer averages and the company is trading in line with average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research