Commoditized businesses fail major strategy tenets, but UAFRS highlights that alone doesn’t make this one a bad credit investment

Commoditized businesses often get a bad reputation, and rightfully so. These companies have limited power over suppliers and offer nothing to customers that a competitor couldn’t also offer.

That said, a bad equity investment doesn’t always make for a bad credit investment, and bond investors are spooked about bad returns for this company without understanding its real credit risk levels. Once things return to normal for this firm, its likely those spooked investors will recognize their error, and bond prices will recover.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Michael Porter is famous for his “Five Forces” and how those should affect corporate strategy. These are often pictured similarly to the below:

Competitive Advantage: Creating and Sustaining Superior Performance (New York: Free Press, 1985), page 5.

The relative importance of each force has been argued by various authors since Porter’s work was published, but the consensus is if firms can master the above, they can have significant success.

In the book Driven, we discussed a framework that draws from similar concepts, suggesting that there are ten tenets that firms should focus on in order to create shareholder wealth. The second tenet, “fulfill otherwise unmet needs” effectively covers four of the five above forces, save for the bargaining power of suppliers. The remaining nine tenets expand upon how to command an industry and create value.

As a result, while a firm likely cannot be successful by only fulfilling unmet needs and mitigating the bargaining power of suppliers, if a firm doesn’t at least do those two things, it will be difficult for it to create value for shareholders.

Commodity businesses fail to do either.

These businesses have limited control over input costs, and given the commoditized nature of their business, they cannot differentiate themselves enough to command premium prices. They fail to meet unmet needs, since there are plenty of other competitors ready to do the exact same thing.

These companies are therefore at the whim of suppliers and customers. If either causes a headwind, it can be painful for these firms and their shareholders.

A great case study in commoditized businesses is the tire market. Absent a select few drivers, most don’t care about brand, as long as quality meets a certain minimum threshold. Therefore, customers are buying based on price.

Meanwhile, one of the biggest input costs for (synthetic) tire producers is oil prices. Natural rubber is largely immune from this cost, but 70% of tires are made of synthetic rubber, so it stands that this cost affects most of the industry.

When oil prices fell off massively earlier in the year, in another market, this would be great for tire producers like Goodyear Tire (GT). Unfortunately, this was a result of economic growth and travel coming to a dead stop. Although the supply side got better, the demand side got much, much worse.

As a result, Goodyear, and all of its competitors, have had to compete on price to keep share, and have failed to sustain profitability in this market, even as costs have come down. In fact, Goodyear is forecast to see massive earnings declines in 2020, and this has resulted in the credit markets getting much more bearish on the name.

Investors are incredibly worried that earnings are poor, and will remain poor, as the firm struggles to compete due to the commoditized nature of its business.

However, earnings alone don’t tell the story for Goodyear. To understand the real risk of the firm, investors need to look at why earnings are negative and what obligations could create liquidity risk.

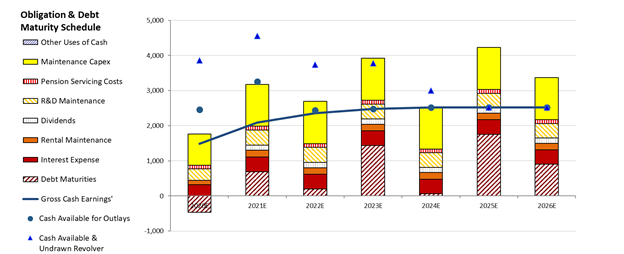

For Goodyear, a majority of costs are around depreciation and R&D, two investments that the firm can defer as necessary. What’s more, the chart below highlights how even if earnings are slow to rebound, the firm should be able to pay “non-flexible” obligations with no problem:

Cash flows will comfortably exceed obligations like debt headwalls, interest expenses, dividends, or rent over the next several years. After the firm’s recent debt issuance, it should even be able to service R&D and CapEx obligations through 2021 as well, though they will likely defer that spend.

It is a fact that things are not good for Goodyear. However, things might not be as bad as they seem. If the company is able to defer spend and get back to normal profitability levels, it would be able to sustain incredibly stable returns historically. This stability would likely give investors resumed confidence in the business, and credit spreads would return to safer, tighter levels.

Equity investors can worry about whether Goodyear can master Porter’s Five Forces, credit investors just need to worry about whether Goodyear can continue to master “paying up on time.”

Credit Markets are too Negative on GT, Disregarding its Capex and R&D Flexibility

Credit markets are grossly overstating credit risk with a cash bond YTW of 7.797% and a CDS of 611bps relative to an Intrinsic YTW of 2.927% and an Intrinsic CDS of 266bps. Meanwhile, Moody’s is accurately stating GT’s fundamental credit risk, with its B1 credit rating one notch higher than Valens’ HY2 (B2) rating.

Fundamental analysis highlights that GT’s cash flows would fall short of servicing operating obligations in 2020 and 2021 due to coronavirus headwinds, before roughly matching operating obligations going forward.

That said, following its recent debt issuance, the firm’s cash flows and cash on hand would be sufficient to cover all obligations including debt maturities until 2022. Additionally, GT has ample capex and R&D flexibility to free up liquidity to help service these obligations in the near-term. Furthermore, the firm’s robust 175% recovery rate indicates it should have access to credit markets to refinance when necessary.

Incentives Dictate Behavior™ analysis also highlights mostly positive signals for credit holders. GT’s management compensation metrics should align them to focus on all three value drivers: asset utilization, margin expansion, and revenue growth, which should lead to Uniform ROA expansion and higher cash flows available for servicing obligations.

Additionally, management is less likely to overleverage the balance sheet, as elevated interest expense could decrease their total compensation. Also, management members are not well-compensated in a change-in-control scenario, indicating that they are unlikely to pursue a sale or accept a buyout of the firm, limiting event risk for creditors.

That said, management members do not hold material amounts of GT equity relative to their average annual compensation, indicating they may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ analysis of the firm’s Q1 2020 earnings call (4/30) highlights that management may be exaggerating the strength of their liquidity, the quality of their relationship with lenders, and their ability to further draw down credit facilities and refinance. Moreover, they may be concerned about declines in US and Canadian sales volumes, industrial shipments, and overhead absorption.

Furthermore, they may lack confidence in their ability to reduce costs and preserve cash, meet capex guidance, and manage their working capital. Management may also be downplaying concerns about the progress of their phased production restart, year-over-year earnings declines, and declines in their accounts receivable and inventory balances.

In addition, they may be exaggerating the potential of their e-commerce investments, the progress of their replacement business restructuring initiatives. Finally, they may be concerned about the sustainability of improving replacement channel fundamentals, their supplier payment terms, and commodity market prices.

GT’s capex and R&D flexibility and a robust recovery rate indicate credit markets are overstating credit risk. As such, a tightening of credit spreads is likely going forward.

SUMMARY and The Goodyear Tire & Rubber Company Tearsheet

As the Uniform Accounting tearsheet for The Goodyear Tire & Rubber Company (GT:USA) highlights, the company trades at a -33.8x Uniform P/E, which is way below global corporate average valuation levels and its historical average valuations.

Negative P/Es only require low EPS growth to sustain them. That said, in the case of Goodyear, the company has recently shown a 6% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Goodyear’s Wall Street analyst-driven forecast projects a 332% shrinkage in earnings in 2020, followed by a slight improvement to 114% shrinkage in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $9 per share. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 8% each year over the next three years and still justify current prices. Wall Street analyst expectations for Goodyear’s earnings growth are below what the current stock market valuation requires in 2020 and 2021.

Meanwhile, the company’s earnings power is below corporate averages. Furthermore, total obligations—including debt maturities, maintenance capex, and dividends—are below total cash flows, and intrinsic credit risk is 266bps above the risk-free rate, signaling moderate risk to its dividend and operations.

To summarize, Goodyear is currently seeing below average Uniform earnings growth, and this performance is expected to continue going forward. Therefore, as is warranted, the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research