Last year’s run on animal shelters will leave lasting tailwinds for today’s company, but Moody’s remains skeptical

Products like pet supplies and gardening have thrived during the pandemic. With more free time than ever, people are looking for both companionship and extra hobbies.

Today’s company is involved in both of these product lines. Despite the surge in demand, rating agencies continue to view the firm as a high credit risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

A surprising trend resulting from the pandemic has been an increase in the sale of pets. As people were trapped at home for long periods, many realized they might as well have a furry friend with them.

You might remember the news early last year that shelters around the country were practically empty thanks to skyrocketing adoption and fostering rates.

With the work-from-home environment, there has never been a better time to train dogs. Even those with busy schedules have found some extra time while working from home.

The At-Home Revolution has birthed many spending trends. Consumers are making unique decisions not possible in normal years.

For those not in the market for a pet, gardening has become another appealing pastime. With people stuck at home, making their yards look presentable has taken on a more central role.

One company sits right in the middle of both the rising gardening and pet trends. Central Garden & Pet Company (CENT) sells both gardening and pet supply products.

The company’s many brands include Adams Flea & Tick Control, Diacon IGR, Perm-X, Nylabone, and Earth’s Finest Cat Litter. The firm sells through retail chains, grocery stores, mass merchants, and through e-commerce solutions.

Central Garden & Pet has seen surging demand throughout the pandemic.

Better yet, this demand is likely to stick around for years to come. New pets create sticky demand – multiple years’ worth of demand for food, toys, and other related products.

However, rating agencies still view Central Garden & Pet as a high credit risk. Moody’s gives the firm a high-yield Ba3 credit rating, indicating a chance of default greater than 10%.

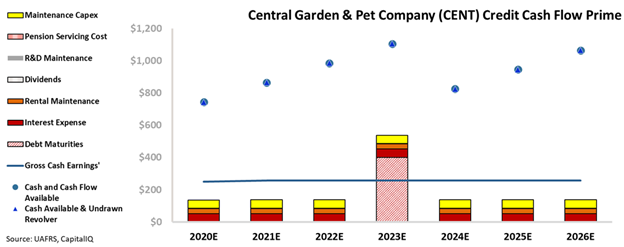

Looking at the firm’s Credit Cash Flow Prime (CCFP) can give us a sense of how risky the firm’s credit really is.

Central Garden & Pet’s cash flows should exceed all operating obligations going forward. Additionally, the firm has enough cash on hand to exceed all outstanding obligations, including a $400 million debt headwall in 2023.

If the company sees another demand surge for pet supplies or gardens due to the At-Home Revolution, there may be even more upside for the firm’s cash flows.

That said, Central Garden & Pet currently has enough liquidity for the next 7+ years. The sizable default risk indicated by Moody’s is therefore too pessimistic.

This is why we rate Central Garden & Pet as a much safer IG4+ (Baa1) credit. This investment grade rating only implies a less than 2% risk of default over the next five years.

Once again, rating agencies are slow to recognize fundamental shifts in different industries. Central Garden & Pet Company is seeing a sustainable increase in demand, which will likely improve cash flows and liquidity.

However, it is only when using Uniform Accounting and looking at the firm’s CCFP can we see the true safety of Central Garden & Pet’s credit.

SUMMARY and Central Garden & Pet Company Tearsheet

As the Uniform Accounting tearsheet for Central Garden & Pet Company (CENT:USA) highlights, the company trades at a 17.0x Uniform P/E, which is below global corporate average valuation levels but around its own historical average valuations.

Low P/Es require Low EPS growth to sustain them. That said, in the case of Central Garden & Pet, the company has recently shown a 57% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Central Garden & Pet’s Wall Street analyst-driven forecast projects a 19% Uniform EPS shrinkage in 2021 and 8% Uniform EPS growth in 2022.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Central Garden & Pet’s $41.15 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 7% each year over the next three years and still justify current prices. What Wall Street analysts expect for Central Garden & Pet’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is 2x the long-run corporate average. That said, intrinsic credit risk is 290bps above the risk-free rate. Together, this signals moderate credit risk.

To conclude, Central Garden & Pet’s Uniform earnings growth is well below its peer averages and the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research