Investors overreacted to last week’s vaccine news, and this essential RV vendor took far too big a hit

During the pandemic, RVs and other vehicles sales skyrocketed, as families take control of their vacations. Today’s firm supplies the parts for these machines to keep the market running.

Last week’s vaccine news caused this company’s stock to plummet. Realistically, investors have no reason to be concerned about this company going anywhere. Furthermore, on a closer look, the firm has stronger profitability than as-reported metrics suggest.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Last week’s news of Pfizer’s (PFE) vaccine sent shockwaves through the market. When trading opened on November 11th, some companies saw their stock soar, while others felt the hurt. This recent swing was only solidified when Moderna announced the results of its own vaccine this Monday.

Thanks to the hope the pandemic is ending, some investors now think themes like “Survive and Thrive” and the “At-Home Revolution” are priced in and have run their course.

After the vaccine announcement, there was a secular rotation out of technology stocks that have overperformed this year. Companies related to leisure and travel, which have had terrible years, saw their stocks come around.

The reality is, a lot of these moves were probably too aggressive. It’s going to take significant time to return to the pre-pandemic normal, even with an effective vaccine.

Additionally, the market is overlooking how the pandemic accelerated existing trends, not simply introduced new ones. It is important to differentiate companies who will see demand sustain after the pandemic and those who will see demand return to normal.

Sectors like online education might see performance return to pre-pandemic levels as students begin flocking back to in-person institutions. Similarly, airlines should see demand return to normal once a vaccine is widely available and distributed.

However, many companies will see the changes wrought by the pandemic continue. Cruise lines have structural challenges which will impact performance even after things return to normal.

In addition, with consumer investment into the At-Home Revolution, demand for some offerings will remain long after normalcy returns. One area in particular is for items like RVs. As we mentioned earlier this month, the pandemic has caused increased demand for outdoor vehicles like boats, RVs, and ATVs.

People have made investments in the RV space and these purchases need to be maintained. It’s unlikely anybody is going to get rid of their new toy as soon as they can safely stop wearing a mask. Because of this trend, companies like LCI Industries (LCII) could benefit for years to come.

LCI Industries supplies much of the RV space with the components necessary for continued operation. If people want to continue using their RVs, LCI Industries will benefit.

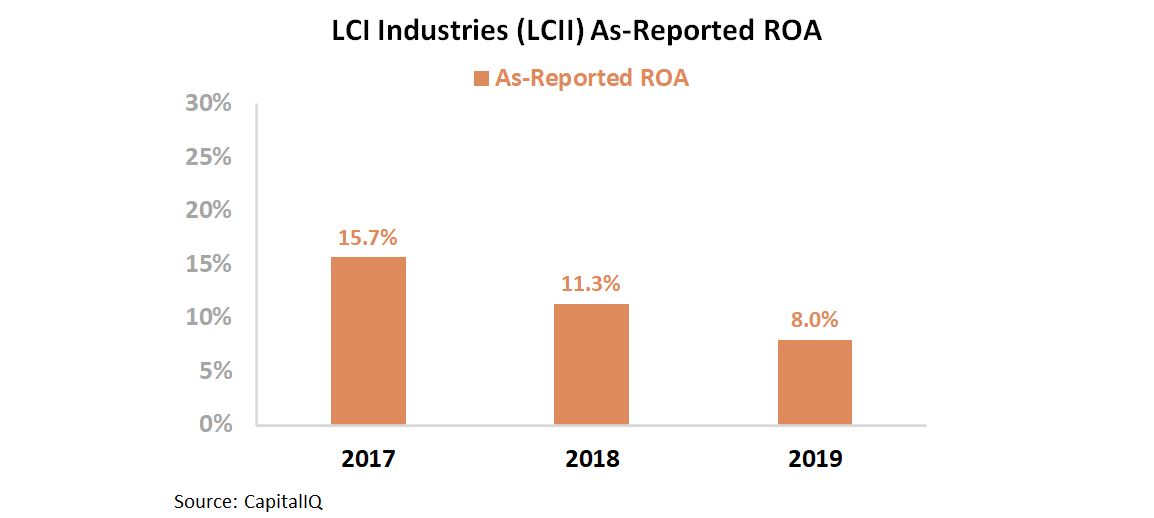

However, the stock fell over 6% last Monday when the news of the vaccine was announced. Looking at as-reported ROA, that move may make sense. As-reported ROA has appeared to trend barely above the firm’s cost of capital in recent years, with ROA reaching just 8% in 2019.

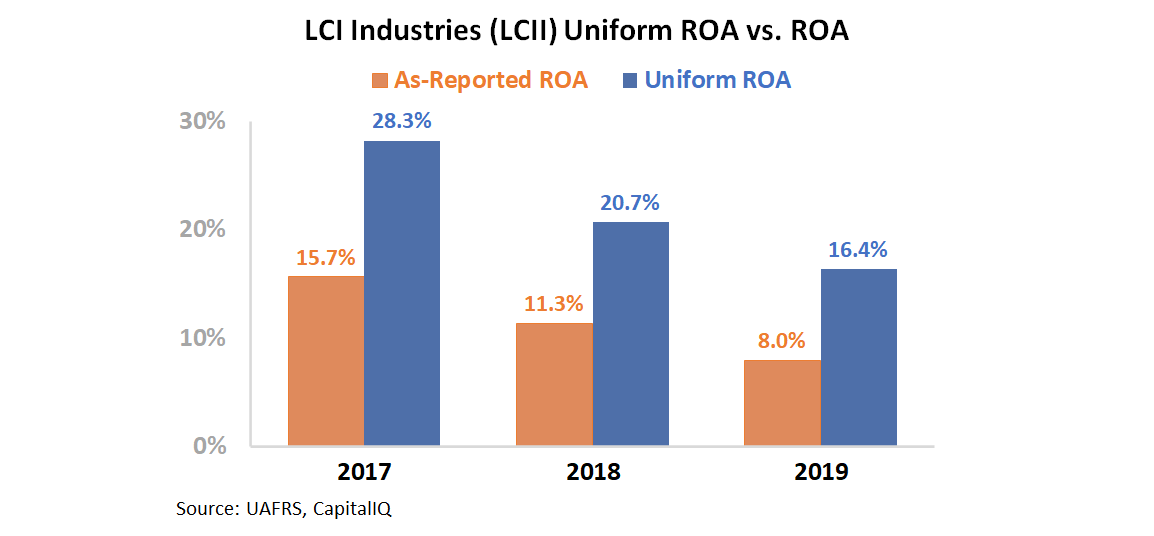

This is not an accurate depiction of the firm’s performance. GAAP’s treatment of amortization and stock option expenses, among other distortions, is suppressing the firm’s profitability.

Uniform Accounting shows LCI Industries has sustained an ROA well above its cost of capital. Over the past three years, ROA has ranged between 16% and 28%.

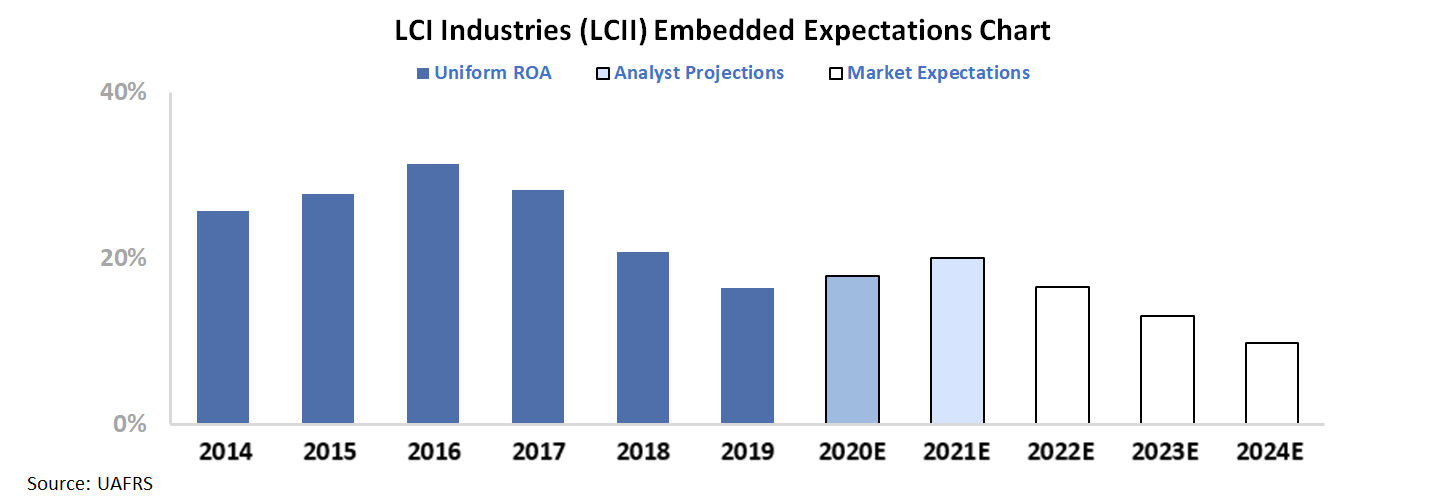

The last aspect we need to consider are the expectations for the firm. To understand what the market is expecting LCI Industries to do, we can use our Embedded Expectations Framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model. Investors build a DCF model using assumptions about the future, which then produces the “intrinsic value” of the stock.

Here at Valens, we know models with garbage-in assumptions only come out as garbage. This is why we turn the DCF model on its head in the chart below. Here, we use the current stock price to solve for what returns the market expects the firm to make.

The dark blue bars represent the historical corporate performance levels, in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how ROA will shift in the next five years.

We can see Wall Street analysts are expecting Uniform ROA to improve from current levels. They expect Uniform ROA to reach 20% in 2021. However, the market is pricing in Uniform ROA to be cut in half by 2024, languishing at 10%.

The market is failing to see how the tailwinds from the pandemic are long-term for LCI Industries. Just because the pandemic is over does not mean LCI Industries will not continue to see elevated levels of demand for years to come.

Uniform Accounting highlights how LCI Industries can benefit for years to come. Without it, investors may think it is a low return business with few prospects for growth.

Just because there is a light at the end of the tunnel, don’t assume all of this year’s trends will come to an end. While many companies will see profitability and demand return to normal once society addresses the pandemic, others will still see structural tailwinds or headwinds going forward.

Should the RV market stay on its feet, LCI Industries is positioned to benefit for years to come.

SUMMARY and LCI Industries Tearsheet

As the Uniform Accounting tearsheet for LCI Industries (LCII:USA) highlights, the Uniform P/E trades at 15.9x, which is below the global corporate average valuation levels, but around its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of LCI Industries, the company has recently shown a 4% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, LCI Industries’ Wall Street analyst-driven forecast is a 12% and 25% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify LCI Industries’ $119 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 3% per year over the next three years. What Wall Street analysts expect for LCI Industries’ earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x corporate average. Also, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, LCI Industries’ Uniform earnings growth is well above peer averages and the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research