The entertainment industry isn’t doomed, but the rating agencies might make you think it is

Many of the “experience” related industries have been slammed throughout the pandemic due to low levels of demand and unfavorable market conditions.

Live entertainment, including concerts, has been on its own shutdown for nearly a year now. The rating agencies, unsurprisingly, are spooked, but the industry as a whole may be poised for an eventual comeback.

Today’s company in particular had a tough 2020, but its credit profile is far stronger than the rating agencies assume.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Many industries have suffered greatly throughout the pandemic. Anything that involves a live “experience,” things like concerts, travel, and movies, has been on hiatus for nearly a year.

Unfortunately, experience products can’t just sit in a warehouse for a year. The past year of concerts and movies are gone for good, and there’s been almost no way to make money in the meantime.

For example, airline companies and hotels cannot store the empty seats or rooms they are not able to sell to save for future demand. Similarly, the movie theater industry can’t start selling last July’s movie tickets.

Finally, bands and artists cannot recover the lost opportunity and revenue the suspension of concerts throughout the pandemic. While many artists and channels have been adapting to the current environment, virtual concerts don’t provide the same experience or economics.

With all of these challenges in these respective industries, it might not come as a surprise rating agencies are pessimistic regarding firms that operate in the area.

For example, Moody’s rates Live Nation Entertainment (LYV), one of the largest businesses revolving around concert venues, as a B2 high yield credit.

While it makes sense logically, it highlights the fact that Moody’s is only looking at lagging historical data and missing the rest of the picture.

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk and it shows a few key factors regarding the firm.

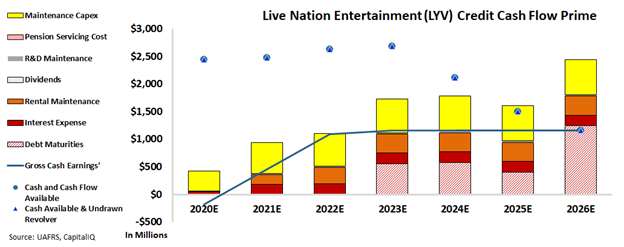

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Live Nation faced serious coronavirus headwinds in 2020, generating negative cash flows. This is before looking at the firm’s obligations. 2021 will similarly be a challenging year. Despite these shorter-term obstacles, Live Nation’s massive cash on hand levels, coupled with the likelihood of a recovery in the industry by 2022, highlights that the company has a much stronger credit profile than Moody’s may think.

Additionally, the potential for a surge in demand back to previous pandemic levels might contribute to the fact that Live Nation really has limited risk of default over the next few years.

This is why Moody’s B2 high yield rating, with a 25%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates Live Nation as a lower medium grade XO rating (equivalent to a Baa3). This rating corresponds with a default rate below 2% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how Live Nation’s credit risk profile is much safer than what rating agencies believe.

By using Uniform Accounting, investors have a better understanding of whether market yields for bonds really make sense, or provide opportunities for investment.

SUMMARY and Live Nation Entertainment, Inc. Tearsheet

As the Uniform Accounting tearsheet for Live Nation Entertainment, Inc. (LYV:USA) highlights, the Uniform P/E trades at -67.3x, which is below the global corporate average valuation levels and its historical average valuations.

Low P/Es require Low EPS growth to sustain them. That said, in the case of Live Nation, the company has recently shown a 3% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Live Nation’s Wall Street analyst-driven forecast is a 640% and 85% EPS decline in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Live Nation’s $88.09 stock price. These are often referred to as market embedded expectations.

To justify current stock prices the company needs its Uniform earnings grow by 36% per year over the next three years. What Wall Street analysts expect for Live Nation’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 2x the corporate average. Also, cash flows and cash on hand are 2x its total obligations within the next five years—including debt maturities and maintenance capex. In addition, intrinsic credit risk is 160bps above the risk-free rate. Together, this signals a low dividend risk and moderate credit risk.

To conclude, Live Nation’s Uniform earnings growth is trading below its peer averages, and trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research