Why Peter Drucker’s recommendation to “outsource the rest” has led this company to a massive payday

As human resource roles are not as easy as most people think, many companies have entered the space to consult companies with their HR department.

With these services difficult to master, today’s company’s as-reported metrics highlight a firm struggling to meet the challenge.

However, when looking at the Uniform Accounting metrics, the company’s financials are painting a different picture.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Peter Drucker, an Austrian management consultant and author, is often known as the founder of modern management consulting. His writings on business and core competencies are still read today, with many of his quotes standing the test of time.

One quote management still leans on today is, “Focus on what you do best, and outsource the rest.” In other words, companies should only spend time and money on what they are good at to create wealth for their business and shareholders.

Anything that isn’t directly a part of this goal, or not essential to the success of the business should be outsourced to other companies or services.

One of the first places many boards or management teams focus on getting outside help from is human resources, as the skills required are so different from the rest of the corporate world.

With a high bar of legal knowledge and expertise in managing talent required, running an HR department is a practical maze to navigate for those inexperienced.

This is why there are numerous companies out there that specifically focus on helping companies large and small with these services.

A few examples of these companies would be Automatic Data Processing (ADP), Paychex (PAYX), and Paycom (PAYC).

Paycom does everything from helping companies onboard and pay employees, to tracking employee work hours and benefits.

In other words, Paycom helps conduct the tasks essential to running any business.

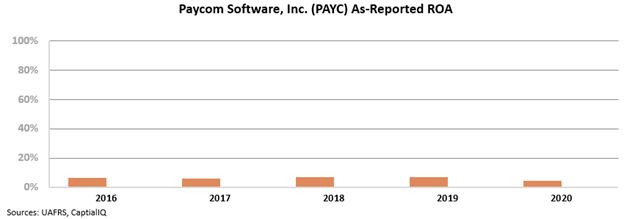

This area of a business is such a hassle to manage, many investors may wonder if there is any profit to be made solving these problems. These perceived challenges line up with the company’s as-reported financial metrics.

Looking just at the as-reported numbers, investors would assume Paycom is only offering a commodity offering in a highly competitive market.

The company’s as-reported return on asset (ROA) figure is currently at a weak 5% levels. For context, the U.S. corporate average is currently at 12%.

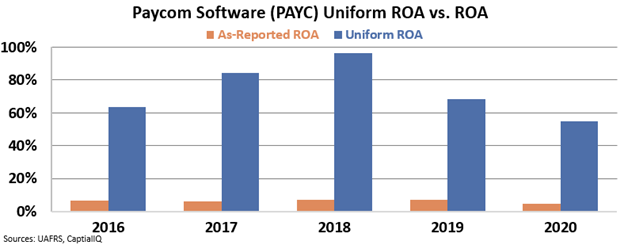

However, this is not an accurate picture of Paycom’s profitability levels.

In reality Paycom has posted robust profitability levels over the past five years.

When looking through a Uniform Accounting lens, it becomes clear the company’s HR services are highly valued by its customers.

Specifically, the company’s ROA metric has consistently exceeded 55% level over the past five years. ROA even peaked at 96% in 2018.

The distortions between the as-reported and Uniform Accounting metrics for Paycom are significant, and they are telling the wrong story for investors.

Running a smooth HR system within a business is crucial, and is a service many customers are willing to pay top dollar for. This is why Paycom has been able to earn such a strong return over the past five years.

SUMMARY and Paycom Software, Inc. Tearsheet

As the Uniform Accounting tearsheet for Paycom Software, Inc. (PAYC:USA) highlights, the Uniform P/E trades at 63.6x, which is above the global corporate average of 25.2x and its own historical average of 54.0x.

High P/Es require high EPS growth to sustain them. That said, in the case of Paycom Software, the company has recently shown a 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Paycom Software’s Wall Street analyst-driven forecast is an 8% and 22% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Paycom Software’s $398 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 29% annually over the next three years. What Wall Street analysts expect for Paycom Software’s earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 9x the long-run corporate average. Also, intrinsic credit risk is 40bps above the risk-free rate and cash flows and cash on hand are 5x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend and credit risk.

To conclude, Paycom Software’s Uniform earnings growth is above its peer averages, and is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research