Rating agencies are calling for a 50% risk of default for this microcap wheelmaker, which appears too overblown

Some industries have thrived during the pandemic. One of these has been the consumer goods sector, as people have been unable to spend their discretionary income on experiences like travel.

Today’s company sells wheels and tires that help power a surging segment of the consumer goods industry. Despite this, rating agencies have viewed the company as a high credit risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One thing which has kept the global economy moving the past three quarters has been the surging demand for physical goods. As people are unable to spend on travel, spending on consumer goods has increased.

This has led to elevated demand for adult consumer goods such as ATVs, snowmobiles, and electric vehicles. Companies like Polaris (PII) have thrived due to the uptick in demand.

Meanwhile, infrastructure spending has been used by the government to create jobs during periods of high unemployment.

There are not many companies that stand to benefit from both of these surges, but Titan International, Inc. (TWI) is bucking that trend.

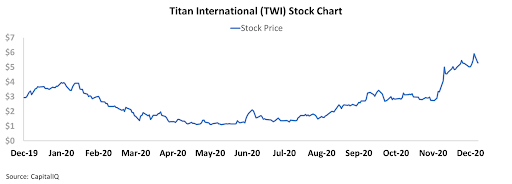

Titan makes wheels, tires, and other products that help supply both of these markets, as well as the agricultural industry. Equity investors have recognized how surging demand will boost this firm’s performance. The stock price has rallied from around $1 in May, up to $5.50 now.

However, creditors appear to have missed the message, as the company’s credit has been rated as a CCC+ by S&P and Caa3 by Moody’s. These ratings imply a risk of default close to 50% within the next five years.

Now don’t get us wrong, Titan is not a riskless company. It has a market cap of just $360 million and a muted Uniform ROA the last few years.

However, looking at the firm’s Credit Cash Flow Prime (CCFP) can give us a sense of how risky Titan’s credit really is.

Titan’s cash flows and cash on hand should exceed all outstanding obligations until 2023, when it sees a material debt headwall. If the company sees a demand surge from the mentioned potential growth avenues, there may be even more upside for the firm’s cash flows.

Titan does not need to make any tough decisions about its credit until 2023 at the earliest, which is still three years from now. The imminent credit default from both Moody’s and S&P is off base for the firm.

This is why we rate Titan as an HY1 (Ba2) credit. While still high-yield, the rating only implies a default risk closer to 10% for the firm.

Titan has a long runway to refinance its debt headwalls and to improve operations.

Investors looking at just the rating agencies’ ratings for Titan would assume the firm to be at an immediate risk of bankruptcy. However, by using Uniform Accounting and looking at the firm’s CCFP, we can see the greater safety in Titan’s credit.

SUMMARY and Titan International, Inc. Tearsheet

As the Uniform Accounting tearsheet for Titan International, Inc. (TWI:USA) highlights, the company trades at a 179.5x Uniform P/E, which is well above global corporate average valuation levels and its own historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Titan, the company has recently shown a 349% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Titan’s Wall Street analyst-driven forecast projects a 3% and 79% Uniform EPS decline in 2020 and 2021, respectively.

Furthermore, the company’s earning power is below the long-run corporate average. Also, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividend. Together, this signals high credit and dividend risk.

To conclude, Titan’s Uniform earnings growth is in line with peer averages, but the company is trading well above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research