Rating agencies are making a losing bet going against this casino operator

Las Vegas is known as the gambling capital of the world. It has the highest concentration of casinos and the oldest location for legal gambling in the U.S. However, casinos exist in other parts of the country as well. Currently, 18 states have casinos located within their borders.

Today’s company is a regional casino operator with locations outside of Las Vegas. Credit markets are spooked by the firm’s cyclical nature.

Below, we show how Uniform Accounting clarifies the financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The casino industry has been one of the hardest hit during the pandemic. Casinos were not deemed “essential businesses”, forcing many to close during the shutdowns starting in March and April.

With activities opening back up during the fall and winter, casinos saw a huge surge in demand. They have a very loyal customer base who were clamoring to get back inside. Anyone who saw images from Las Vegas could tell how fast demand returned to these businesses.

Similar to the national players in Las Vegas, regional casinos saw a huge bounceback in demand. One company in particular benefiting from this rebound is Boyd Gaming Corporation (BYD).

Boyd has 29 casinos across the country with over 800,000 square feet of casino space. The firm has three casinos located in downtown Las Vegas, with the rest spread out across the country.

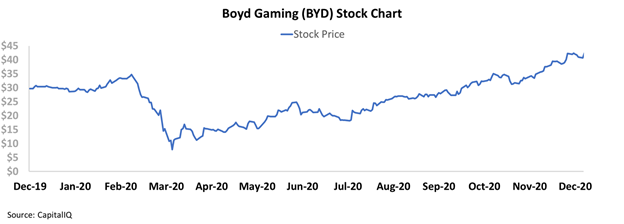

The stock has risen from a low of $7 in March to its peak of $43 in December.

Despite the strength of the stock, rating agencies are not buying into the success of the business. Casinos are generally cyclical businesses with higher demand coming in times of prosperity. Additionally, they are capital intensive with large capex investments required to build and maintain properties.

Moody’s thus rates the firm as a high-yield B2 credit rating. This indicates the firm has a near 25% chance of defaulting on its debt within the next five years.

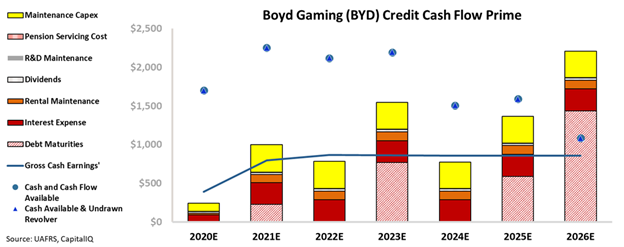

However, the firm’s Credit Cash Flow Prime (CCFP) tells a different story. The firm is a much stronger credit than rating agencies give it credit for.

Specifically, Boyd’s cash on hand should be able to cover the expected shortfall in cash flows, exceeding obligations in every year until 2026. This gives Boyd a six year runway to improve operations or refinance the debt.

While Boyd does have a long debt runway, the firm has cyclical cash flows and a low Uniform ROA.

Thus, Valens rates the firm as a much safer crossover XO rating. The firm is not quite at an investment grade due to its cash flows, but is much safer than rating agencies imply.

This rating indicates only around a 2% chance of default over the next five years, far lower than the 25% risk implied by rating agencies.

Ultimately, even with a low ROA and cyclical cash flows, the firm’s strong balance sheet and expected cash build should mitigate credit risk. However, it is only when looking at Boyd under the Uniform Accounting framework can we see the true risk of this casino operator.

SUMMARY and Boyd Gaming Corporation Tearsheet

As the Uniform Accounting tearsheet for Boyd Gaming Corporation (BYD:USA) highlights, the company trades at a 36.2x Uniform P/E, which is above global corporate average valuation levels, but below its own historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Boyd Gaming, the company has recently shown a 266% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Boyd Gaming’s Wall Street analyst-driven forecast projects a 158% and 203% EPS shrinkage in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Boyd Gaming’s $41.03 stock price. These are often referred to as market embedded expectations.

The company needs to grow its Uniform earnings by 7% each year over the next three years to justify current prices. What Wall Street analysts expect for Boyd Gaming’s earnings growth is far below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is above the corporate average, and cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate credit risk.

To conclude, Boyd Gaming’s Uniform earnings growth is below its peer averages, but the company is trading near average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research