Size matters for creditors, but even at below peer-average yields, the market is not understanding the favorability of this firm’s capital structure

For creditors, the size of a company matters. Larger companies have larger market caps, revenue streams and typically, asset bases. As such, larger companies tend to be safer credit investments.

Even in a struggling industry, this firm’s size has given it the opportunity to borrow at lower cost.

Additionally, following the firm’s prior debt struggles, its management team has become vigilant in managing credit risk, and has built a favorable capital structure. Therefore, even though the market may respect its size, it is still overstating its credit risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

For creditors, size matters.

Larger companies tend to have lower cost to borrow due to a number of different reasons. For instance, because they have large market capitalizations, large companies have significant shareholder wealth that they are able to tap into.

Also, they generally have sizeable revenue streams, so cost reduction initiatives and other efficiency improvements can create outsize benefits for the firm, as well as creditors. Moreover, they typically have larger asset bases, which gives creditors comfort that loans and other debt can have some asset-backing behind them.

In recent years, despite steady growth and sustained productivity, much of the mining industry has been punished by the stock market. The market seems to be concerned about shifting consumer sentiment, an increased focus on climate change and pollution, and technology adoption, weighing down market values for these firms.

That said, two metals, gold and copper, have held up fairly well against this backdrop. Specifically, within these sub industries, a premier copper miner with exposure to gold and molybdenum, Freeport-McMoRan (FCX), has been able to maintain its valuation surprisingly well.

Despite this recent stability, the company’s market capitalization is just a fraction of its historical peaks. It is valued well below its peaks following its Phelps Dodge acquisition in 2007 and well below what it was worth prior to its merger with McMoRan Exploration and acquisition of Plains Exploration & Production in 2013.

Yet, due to the company’s remaining size, with a market cap exceeding $16 billion, it has relatively low yields for the space, with YTW on its bonds generally ranging from 3%-6%. This is significantly lower than many other firms with exposure to oil and gas assets, particularly given the weakness in oil prices throughout the coronavirus pandemic.

While some firms in the field struggle with high leverage and face the threat of bankruptcy as their cash flows have leveled off, Freeport-McMoRan has actually benefited from its past issues with debt.

Following a painful period in which the market was worried about its leverage, the firm’s management learned that they need to limit credit risk in order to be recognized appropriately by investors.

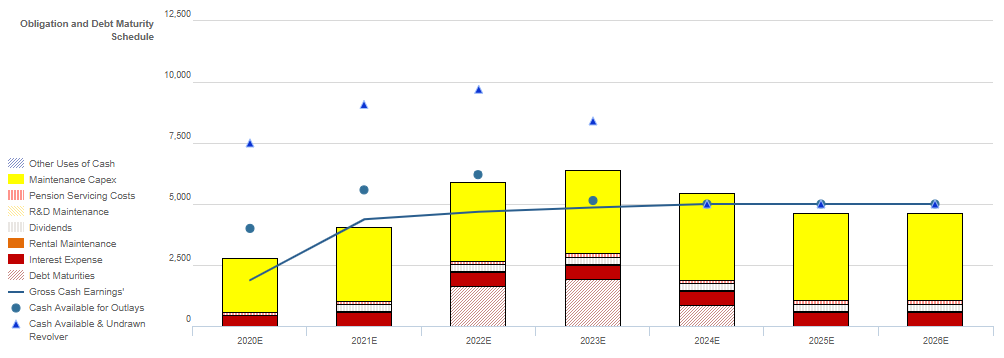

As such, the company has limited debt maturities in the next few years, as evident in the Credit Cash Flow Prime for the firm below.

This favorable capital structure, combined with Freeport McMoRan’s scale and cash flows relative to obligations suggest it shouldn’t have any issues with credit going forward. Moreover its sizable capex flexibility affords it the opportunity to cut expenses in the near-term to avoid a liquidity crunch.

This safe credit profile is highlighted in the firm’s relatively low yields. Yet, even at current levels, the yield may be overstating the company’s true fundamental credit risk, potentially still factoring in its former debt struggles.

Tighter Credit Spreads is Likely Given FCX’s Sizeable Liquidity

Cash bonds markets are grossly overstating FCX’s credit risk with a YTW of 4.486% relative to an Intrinsic YTW of 1.556%, while CDS markets are materially overstating credit risk with a CDS of 360bps relative to an iCDS of 124bps. Meanwhile, Moody’s is accurately stating the firm’s fundamental credit risk, with its high-yield Ba1 rating one notch lower than Valens’ XO (Baa3) rating.

Fundamental analysis highlights that FCX’s expected cash flows should be sufficient to cover operating obligations in each year after 2020, and even in 2020, the firm has sufficient liquidity to service shortfalls.

The combination of the firm’s cash flows and cash on hand should be sufficient to service all obligations until 2023, when the firm faces the second of three consecutive $850 million+ debt headwalls. The firm even has ample capex flexibility to free up sufficient liquidity in the near-term. Additionally, FCX’s robust 284% recovery rate on unsecured debt and sizable market capitalization should allow it to access credit markets to refinance its debt, as necessary.

Incentives Dictate Behavior™ analysis highlights positive signals for credit holders. FCX’s management compensation framework should drive management to focus on all three value drivers: asset utilization, margin expansion, and top-line growth. This leads to Uniform ROA improvement and increased cash flows available for servicing obligations.

Furthermore, management members have relatively low change-in-control compensation, indicating they are not likely to accept a takeover or pursue a buyout of the firm, limiting event risk. Finally, most management members are material owners of FCX equity relative to their annual compensation, indicating they are likely well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q1 2020 earnings call (4/24) highlights that management is confident about the progress of their strategic PT-FI initiatives, that many input costs declined, and that copper has important uses in the healthcare industry.

However, they may be concerned about their balance sheet liquidity, Cerro Verde production capacity, and lower copper prices. Moreover, they may be exaggerating the growing importance of copper as a commodity, the long-term potential of their Lone Star mine, and the quality of their government relationships.

In addition, management may be concerned about IUPK project delays, macroeconomic uncertainty, and lower milling and mining rates, particularly in the Americas. Furthermore, they may lack confidence in their ability to reduce operational costs, guarantee employee safety, and meet their capex guidance.

Finally, they may be concerned about the sustainability of high gold prices, the benefits of the combination of Grasberg and the Phelps Dodge portfolio, and their cash generation ability.

FCX’s operating sustainability, sizeable liquidity, and robust recovery rate suggest credit markets are overstating credit risk. As a result, a tightening of credit spreads is likely going forward.

SUMMARY and Freeport-McMoRan Inc. Tearsheet

As the Uniform Accounting tearsheet for Freeport-McMoRan Inc. (FCX:USA) highlights, the company trades at a -39.0x Uniform P/E, which is well below global corporate average valuation levels and its historical average valuations.

Negative P/Es only require low EPS growth to sustain them. That said, in the case of Freeport-McMoRan Inc., the company has recently shown a 170% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Freeport-McMoRan Inc.’s Wall Street analyst-driven forecast projects 23% growth in earnings in 2020, followed by a decline of 90% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $11 per share. These are often referred to as market embedded expectations.

Meanwhile, the company’s earnings power is below corporate averages. Furthermore, total obligations—including debt maturities, maintenance capex, and dividends—are slightly above total cash flows, and intrinsic credit risk is 110bps above the risk-free rate, signaling moderate risk to its dividend and operations.

To summarize, Freeport-McMoRan Inc. has seen below average Uniform earnings growth, and this performance is expected to continue going forward. Therefore, as is warranted, the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research