Although consumer staples companies are expected to stay strong, not all will prevail

With people spending more time and money at home, consumer staples companies have seen sustained demand, and they are projected to continue on this trend.

As such, major ratings seem anything but worried when rating today’s company’s debt. However, it might not be taking specific company risk into account.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Most investors, across equity and credit, are specialized. Some investors are particularly comfortable investing in internet startups, while others, including Warren Buffett, won’t touch that type of business model.

Peter Lynch had a famous investment philosophy. Similar to Buffett, he would only buy a stock if he understood the business model.

Lynch took it a step further when teaching retail investors – he recommends “buying what you know.” If you walk through a mall, find the businesses you know and like and invest in them.

By building up an expertise or comfort within a handful of industries and business models, investors can make better fundamental decisions.

Consumer staples companies are viewed as one of the more sleepy, but secure sectors of the entire economy, and they tend to be a great starting place for equity investors.

In the less risky, but no less interesting credit market, this perception of consumer staples is only amplified.

Over the past year, people have grown accustomed to spending more time and money in their home, creating steady demand for these consumer goods.

Products like Smuckers jelly or Folgers coffee are expected to see steady demand into the future.

In addition, companies that sell products related to pet care, such as pet food, will continue to see high demand. As many people have decided to adopt pets over the pandemic, pet food like Meow-Mix and Milk-Bone will see continued demand.

The J.M. Smucker Company (SJM) owns a diverse portfolio of consumer staple products, with just a few being all of the above mentioned brands.

Major rating agencies are bullish on the name, pricing in its secular tailwinds and opportunity to capitalize on significant market trends.

Specifically, S&P gives the J.M. Smucker Company an investment grade BBB rating, with the implied assumption of a sub 2%+ risk of default over the next five years.

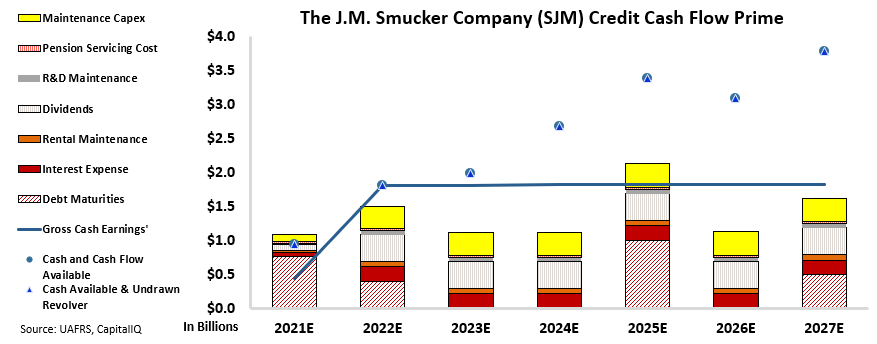

To see the real credit risk, our Credit Cash Flow Prime (CCFP) analysis shows the real picture. As you can see below, investors should be careful about painting with too broad of a brush stroke when investing in these companies that seem to have favorable tailwinds behind them.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, The J.M. Smucker Company doesn’t have the cash flows or cash on hand to cover its debt in 2021, giving it little room to refinance.

Additionally, the firm has massive debt headwalls in 2022, 2025, and 2027. Although the firm should have cash flows and available cash to cover these obligations before the 2021 refinancing, it may put pressure on the company’s cash flows through what is supposed to be a successful few years.

Rather than an investment grade name, The J.M Smucker Company is actually much riskier than it appears at first. This is why S&P’s investment grade rating, with a sub 2%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates the company as a high yield HY2- rating. This rating corresponds with a default rate around 25% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

Ultimately, Uniform Accounting and the Credit Cash Flow Prime analysis highlights how the company’s credit risk profile is much riskier than what rating agencies believe.

SUMMARY and The J. M. Smucker Company Tearsheet

As the Uniform Accounting tearsheet for The J. M. Smucker Company (SJM:USA) highlights, the Uniform P/E trades at 16.7x, which is below the 23.7x global corporate average valuation levels, but around its historical average valuations of 16.8x.

Low P/Es require low EPS growth to sustain them. That said, in the case of The J. M. Smucker Company, the company has recently shown a 16% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, The J. M. Smucker Company’s Wall Street analyst-driven forecast is a 6% and 4% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify The J. M. Smucker Company’s $135 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 2% annually over the next three years. What Wall Street analysts expect for The J. M. Smucker Company’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 5x the corporate average. However, cash flows and cash on hand are below total obligations. All in all, this signals a high credit and dividend risk.

To conclude, The J. M. Smucker Company’s Uniform earnings growth is above with peer averages. However, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research