The demand for this firm’s services are as certain as death and taxes

Despite yielding returns near the corporate average, investors are willing to pay a premium for today’s firm due to its secure cash flows.

Today, this means the firm is sizably overvalued, as it’s unlikely to see cash flows improve in such a steady business.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Although the markets, and life, can be full of chaos, there are a few certainties. Ben Franklin referenced two while writing Jean-Baptiste Le Roy in 1789. He quoted both Daniel Defoe’s The Political History of the Devil and Christopher Bullock’s The Cobbler of Preston with “nothing can be said to be certain, except for death and taxes.”

Sadly, there is something else we can undoubtedly add to death and taxes as a certainty in life. This is the fact that our species will continue creating garbage.

This may seem negative, but enterprising minds can see the positive. Some companies thrive on garbage.

Companies in the waste business have been great investments for the past twenty years or so. One man’s trash is another firm’s treasure.

Waste Management (WM) engages in the provision of waste management environmental services. This business reliably grows as our population and consumption expand, meaning its cash flows have reliably grown for the last several decades.

As Uniform Accounting shows, Waste Management has seen fairly stable Uniform ROA expansion over the last 15 years. Its Uniform ROA has expanded from roughly 5% in 2005 to 7% in 2019.

While not robust, these returns are stable and predictable.

Waste Management’s steady growth in demand and lack of uncertainties guarantee a steady cash stream. This consistent performance is worth a premium for many risk-averse investors.

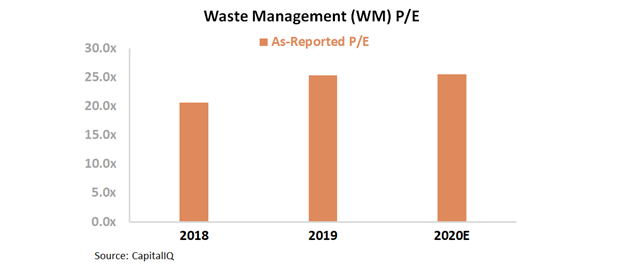

With this information, it would make sense the P/E ratio of the firm is around 26x. Even though the company generates returns near the corporate average, investors are willing to pay a little above corporate averages for the security of cash flows and secular growth.

However, the firm is not actually at this “reasonable” premium value. The market P/E is distorted due to bad accounting practices.

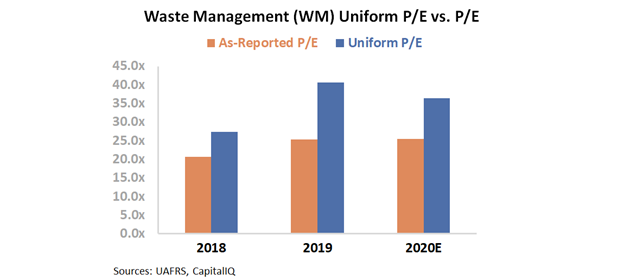

In reality, Waste Management trades at a 36x Uniform P/E. At these valuations, the firm is trading more like a high-growth technology firm. These valuations are well above what a waste management company earning cost-of-capital returns should see.

Investors only looking at the as-reported market P/E may believe Waste Management is at a reasonable premium despite lower ROAs. By cleaning up the bad accounting, investors can see that valuations are not as reasonable as they initially look.

Waste Managment’s services are as eternal as death and taxes for the modern world. Despite this, investors should always make sure they are paying the right price for consistency. Just because Waste Management is a solid company, it is not necessarily a good stock to own.

SUMMARY and Waste Management, Inc. Tearsheet

As the Uniform Accounting tearsheet for Waste Management, Inc. (WM:USA) highlights, the Uniform P/E trades at 36.4x, which is above the global corporate average valuation levels and its historical average valuations of 33.1x.

High P/Es require high EPS growth to sustain them. In the case of Waste Management, the company has recently shown a 1% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Waste Management’s Wall Street analyst-driven forecast is a 23% EPS shrinkage in 2020, followed by a 24% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Waste Management’s $115 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 11% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Waste Management’s earnings growth is below what the current stock market valuation requires in 2020, but above that requirement in 2021.

Furthermore, the company’s earning power is around the corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a moderate credit and dividend risk.

To conclude, Waste Management’s Uniform earnings growth is around peer averages, and the company is also trading in line with its peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research