The reversal of globalization is going to hurt many companies’ profitability, UAFRS shows this company as a big winner

Today’s company is a software-as-a-service firm poised to benefit from disruptions in globalization. However, looking at as-reported numbers, it appears the firm has negative returns.

UAFRS (Uniform) based analysis, on the other hand, shows the firm’s real performance, with the market and as-reported metrics missing the profitability of the firm.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We first heard about Alibaba (BABA) from a colleague of ours who previously worked in the consumer products industry. The conversation was long before Alibaba was perceived to be the Amazon (AMZN) of Asia that could blow investors away.

My colleague was most impressed by the company’s scale. He was excited at his prior job by how Alibaba could help source basic supplies his company needed, such as chemicals and simple plastic parts, in volumes, with quality.

For any manufacturing company, supply chain management and low-cost sourcing are imperative for improving profitability levels.

Part of the way US corporations have been able to steadily boost profitability over the past 20 years has been a total focus on optimizing supply chains. It is also what has enabled inflation to remain so low across the world in the past 20-30 years.

US corporate profitability has ridden a steady tailwind as globalization has increased over that period. As Chinese weavers got more expensive, production moved to Bangladesh. As fabrication got too expensive in China or Taiwan, it moved to Southeast Asia.

However, the easy gains may now be behind us, as globalization appears to be in reverse. No longer are tariffs declining and supply chains getting further afield; the world is starting to look more questioningly at globalization.

This means companies may be looking to bring sourcing and supply chains back to their home country or make other tough decisions that could impact their bottom lines negatively.

This consolidation of production risks being expensive, leading to margin compression, so an even more laser-focused attention on optimizing supply chain costs will be essential for companies to continue to deliver earnings growth.

Any company who can assist in this process stands to benefit. One software firm that does is Coupa (COUP), which offers a platform to allow companies to manage their supply chain and sourcing. The all-in-one business platform also aids companies in analyzing each step of the supply chain to make it more efficient.

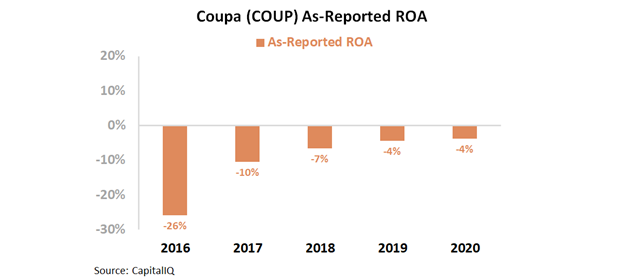

Similar to Splunk (SPLK), one would expect a company offering such an important solution to have exceptionally high profitability. However, as-reported metrics make Coupa appear unprofitable.

As-reported return on assets (ROA) has been negative each of the past five years and was -4% this past fiscal year.

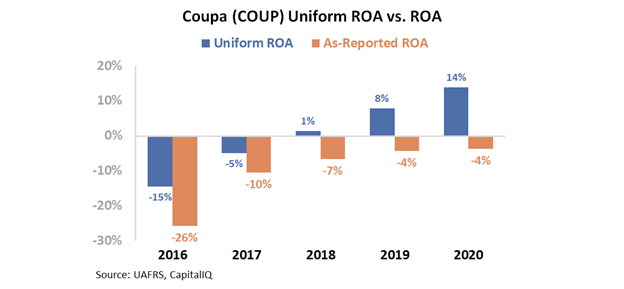

However, this picture of Coupa’s performance is inaccurate, pulled down by distortions in as-reported accounting. Due to GAAP’s treatment of stock option and R&D expenses, among other distortions, the market has been misled on the success of this firm.

Uniform Accounting shows a growing firm with a positive ROA, reaching a high of 14% this past year. As questions about supply chains have grown, demand for Coupa’s offerings has also risen.

However, understanding if a company is undervalued is not just about understanding a company’s real historical profitability, it is necessary to see what analysts and the market are expecting Coupa to do in the future. To evaluate the market’s expectations for the firm, we can use the Embedded Expectations Framework.

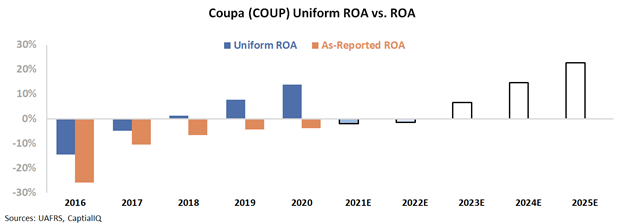

The chart below explains the company’s historical corporate performance levels, in terms of ROA (dark blue bars) versus what sell-side analysts think the company is going to do in the next two years (light blue bars) and what the market is pricing in at current valuations (white bars).

Analysts are expecting the firm to see lower profitability levels in the coming two years. In the short run, some businesses are freezing investments in Coupa’s software because of poor macroeconomic conditions. This will adversely affect the firm; however, Coupa has the potential to continue seeing returns expand in the long-term.

The market appears to see this, and is expecting Coupa to improve its ROA to 23% by 2025. This would be an all-time high for Coupa, and the firm will need to grow rapidly to reach this level of profitability.

That being said, the company has already been able to expand ROA impressively the past several years. And as we’ve seen with other software firms, as a company gains critical mass, returns can expand impressively. As the need for Coupa’s software expands, these expectations, while high, are not necessarily unreasonable.

Ultimately, Uniform Accounting shows the true strength of Coupa’s business. Coupa’s intuitive software application can help businesses become more efficient and cut costs. The strength of its product has pushed Uniform ROA to improve in recent years. The question now is, can Coupa sustain this improvement once the pandemic is behind it?

Without Uniform Accounting, investors would miss the recent positive inflection in Coupa’s profitability, and because of that, would misunderstand whether high expectations are even achievable. Although the market’s expectations for Coupa are steep, if the firm is able to continue its recent trend of profitability improvement, it may be an attractive investment.

Coupa Software Incorporated Embedded Expectations Analysis – Market expectations are for continued Uniform ROA expansion, and management is confident about client support, sales, and acquisitions

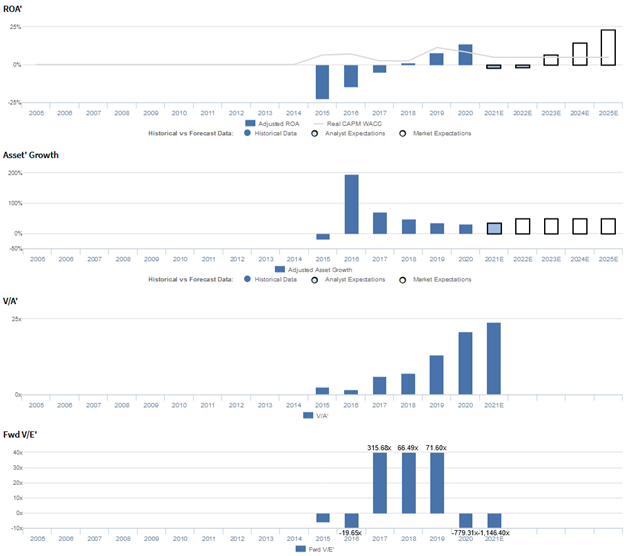

COUP currently trades at a historical high relative to Uniform assets, with a 23.9x Uniform P/B (V/A’). At these levels, the market is pricing in expectations for Uniform ROA to expand from 14% in 2020 to 23% in 2025, accompanied by 51% Uniform asset growth going forward.

However, analysts have bearish expectations, projecting Uniform ROA to collapse to 2% in 2022, accompanied by 36% Uniform asset growth.

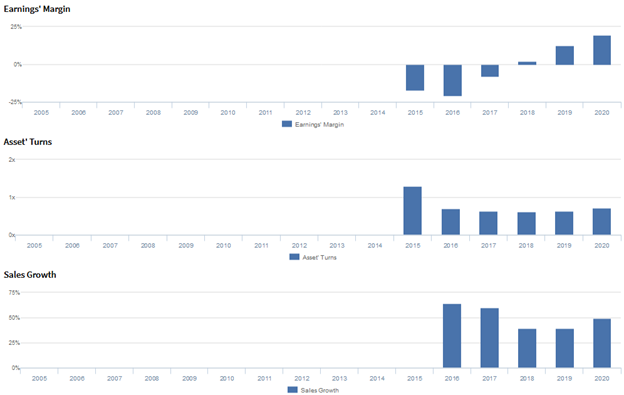

Historically, as a start-up business spend management platform, COUP has seen consistently improving profitability. After ranging at negative levels from 2015-2017, Uniform ROA inflected positively to 1% in 2018 before expanding to a peak of 14% in 2020.

Meanwhile, due to its asset-light nature, Uniform asset growth has been robust and positive in each of year since 2016, while ranging from 30%-71%, excluding 195% growth in 2016, due to the firm’s IPO.

Performance Drivers – Sales, Margins, and Turns

Improvements in Uniform ROA have been driven by improving Uniform earnings margins, accompanied by stable Uniform asset turns.

After ranging at negative levels from 2015-2017, Uniform margins inflected positively to 2% in 2018 before expanding to a high of 19% in 2020.

Meanwhile, Uniform turns fell from 1.3x in 2015 to 0.7x in 2016, before stabilizing at 0.6x-0.7x levels through 2020.

At current valuations, the market is pricing in expectations for continued Uniform margins expansion and for Uniform turns to climb to a new peak.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2020 earnings call highlights that management is confident that their client GOJEK is utilizing the Coupa platform to support their Asian expansion and that Volkswagen Group Australia (VGA) is leveraging them to maximize preapproved contract-backed spending.

In addition, they are confident that sales discussions over phone and video conferences have been effective, that the Yapta acquisition fits well with their M&A strategy, and that they are continuing to build their business and deliver on stakeholder commitments through the pandemic.

However, management may lack confidence in their ability to sustain their revenue growth rate, and they may be exaggerating their agile operating model and the value of their subscription approach to clients hoping to gain visibility, control, and agility.

Furthermore, they may have concerns about their comprehensive platform changes, the interfaces between the power user application and transactional engine, and the impact of the coronavirus on their net spending growth.

Additionally, they may be overstating Coupa Pay’s ability to take advantage of every payment rail within a single interface and leverage customers’ existing bank relationships in one platform, and they may be exaggerating the priority businesses place on digital transformation initiatives.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for COUP than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate COUP’s margins, a key driver of profitability. For instance, as-reported EBITDA margin was -12% in 2020, substantially lower than Uniform earnings margin of 19%, making COUP appear to be a much weaker business than real economic metrics highlight.

Moreover, since inception, as-reported EBITDA margin has remained at negative levels through 2020, while Uniform margins inflected positively in 2018, distorting the market’s perception of the firm’s historical profitability.

SUMMARY and Coupa Software Incorporated Tearsheet

As the Uniform Accounting tearsheet for Coupa Software Incorporated (COUP:USA) highlights, the Uniform P/E trades at -1,146.4x, which is well below the global corporate average valuation levels and its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Coupa Software, the company has recently shown a 77% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Coupa Software’s Wall Street analyst-driven forecast is a 227% EPS shrinkage in 2021, followed by a 6% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Coupa Software’s $248 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow by 61% each year over the next three years. What Wall Street analysts expect for Coupa Software’s earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 2x corporate average. However, cash flows are above their total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Coupa Software’s Uniform earnings growth is below its peer averages. Also, the company is trading well below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research