This company has had a high-yield grade from S&P since its IPO, but the market disagrees. Uniform Accounting uncovers who is right

This company issued debt a year after its IPO and in the six years since, S&P has remained adamant that it is a high-yield name.

However, the credit markets disagree, and yields on this firm’s debt have ranged from just 2% to 4%, while other high yield credits have reached north of 6%, 7%, or even 8% recently.

Are the markets missing something or is S&P giving an incorrect view of the firm? Uniform Accounting helps us clear up the picture.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Roughly a year after its IPO in late 2013, Twitter issued $1.4bn in convertible debt. It wanted to raise capital without immediately diluting shareholders, with share prices that were still around IPO prices after a year.

After issuing the debt, the firm was sitting on roughly $3.6bn in cash, and was about to close its second straight year of positive operating cash flows.

These metrics didn’t matter to S&P, who rated Twitter a high-yield, BB- credit.

S&P saw a firm with deeply negative net income, no interest coverage ratio to speak of, and debt/equity ratios that reached over 40% for a startup. Regardless of cash balances, or the positive cash flows, S&P saw bad as-reported bottom line numbers, and Twitter got the high-yield stamp.

Fast forward to six years later…

Today, Twitter revenues are 5x greater than they were in 2013. The company has a comfortably-positive bottom line. Cash on hand sits at $7.6bn. Free cash flow is over $500mn.

However, S&P still thinks the name is a risk. Its rating for Twitter is just BB+, either high-end high yield or crossover, depending on how one thinks about the ratings.

It’s possible S&P thinks Twitter’s 2.0x interest coverage ratio is too thin for a risky company or its 47% debt/equity ratio is too high for a tech company that has seen market capitalization fall recently.

Maybe S&P is looking at the company’s debt yield of 3%-4%, compared to the firm’s ~2% return on assets (ROA), and thinking this positioning is unsustainable.

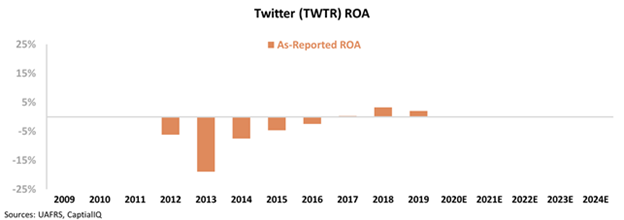

After all, as-reported ROA fell last year, after finally inflecting positively in 2017 and 2018:

Twitter does appear to be an operational risk at first glance, if they can’t get returns above the cost of capital.

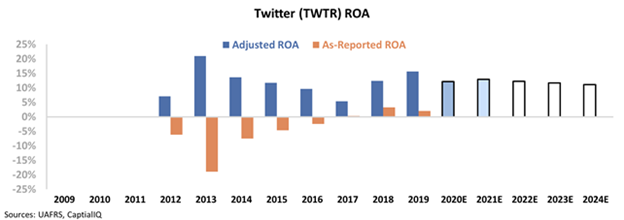

But what S&P is missing is that returns are actually above the cost of capital, comfortably so, once accounting distortions are removed.

When Uniform Accounting adjustments are applied, it is clear Twitter actually has an ROA well into double-digit territory, at 14% in 2019.

The firm not only has positive cash flows, but adjusted gross earnings actually reached $1.9bn last year, well over what the as-reported numbers show.

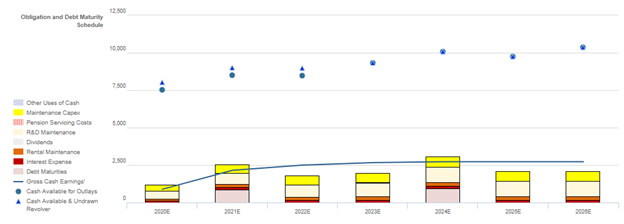

And when looking at the actual obligations of the firm, as Valens does using our Credit Cash Flow Prime, not just debt ratios, it is clear Twitter should have no issues servicing their obligations:

Not only does Twitter’s massive cash balance afford it significant operating flexibility, but cash flows alone should be sufficient to service not just debt obligations, but nearly all obligations in each year going forward.

In the years Twitter does have large debt obligations, 2021 and 2024, the firm would only need to slightly cut capex, or could dip into its deep pockets to service cash flow shortfalls.

TWTR has been an investment-grade name under the Valens framework in every year since it first issued debt as a result. A framework looking at true cash flows relative to obligations, as opposed to just looking at bad as-reported data, and debt ratios that don’t look at the term structure of debt, highlights a much safer name.

Clearly the market has agreed, as Twitter’s debt has yielded just 2%-4% over the last few years, in line with large investment-grade peers. With most high-yield names yielding 4%, 6%, or even 7%+, it’s obvious the market doesn’t view Twitter in the same light, and recognizes S&P’s rating isn’t reflective of the company’s real outlook.

Maybe someday S&P and the rest of the traditional credit rating agencies will catch on…

Rating Agencies Continue to Overlook TWTR’s Credit Risk Despite Its Robust Recovery Rate and Sizable Market Capitalization

Credit markets are grossly overstating credit risk with a cash bond YTW of 3.978%, relative to an Intrinsic YTW of 1.358% and an Intrinsic CDS of 65bps. Meanwhile, Moody’s is overstating credit risk with its Ba2 rating four notches lower than Valens’ IG4+ (Baa1) credit rating.

Fundamental analysis highlights that TWTR’s cash flows should comfortably exceed all operating obligations going forward. In addition, the combination of the firm’s cash flows and ample cash on hand should comfortably exceed all obligations through 2025, including material debt maturities of $869mn in 2021 and $948mn in 2024.

Furthermore, the company’s robust 450% recovery rate on unsecured debt and sizable market capitalization should facilitate easy access to credit markets to refinance, if necessary.

However, Incentives Dictate Behavior™ analysis highlights mixed signals for creditors. TWTR’s compensation framework should drive management to focus on top-line growth and margins. However, the compensation framework does not punish management for overleveraging the firm’s balance sheet to finance growth, potentially limiting cash flows available to service obligations.

Furthermore, CEO Dorsey has elected to forego any compensation since 2015, indicating he may not be incentivized to pursue the same objectives as the rest of management. That said, members of management are not well compensated in a change in control scenario, indicating they are unlikely to accept a buyout or pursue a takeover of the company, limiting event risk for creditors.

Moreover, most management members are material holders of TWTR equity relative to their annual compensation, indicating they may be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q4 2019 earnings call (2/6) highlights that management is confident about new user engagement and that they want to help consumers realize the benefits of a more personalized experience. However, they may have concerns about development speed issues, their data licensing business, and advertising revenues.

Moreover, they may lack confidence in their ability to improve the onboarding experience and add new timeline discovery features, and they may be exaggerating their focus on broadening their services, and their ability to help connect advertisers with consumers.

Operational sustainability, ample cash on hand, and a robust recovery rate suggest that credit markets and Moody’s are overstating credit risk. As such, a tightening of credit spreads and a ratings improvement are both likely going forward.

SUMMARY and Twitter, Inc. Tearsheet

As the Uniform Accounting tearsheet for Twitter, Inc. (TWTR:USA) highlights, the company trades at a 49.7x Uniform P/E, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es only require high EPS growth to sustain them. That said, in the case of Twitter, the company has recently shown a 28% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Twitter’s Wall Street analyst-driven forecast projects a 78% shrinkage in earnings in 2020 followed by a growth of 230% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $33 per share. These are often referred to as market embedded expectations.

In order to meet the current market valuation levels for Twitter, the company would just have to have Uniform earnings grow by 7% each year over the next three years.

Wall Street analysts’ expectations for Twitter’s earnings growth are above what the current stock market valuation requires in 2021.

Meanwhile, Twitter’s Uniform earnings growth is below peer average levels, yet the company is still trading above peer valuations.

In addition, the company’s earnings power is 2x corporate averages. Furthermore, total obligations—including debt maturities, maintenance capex, and dividends—are above total cash flows, but intrinsic credit risk is 100bps above the risk-free rate, signaling an average risk to its dividend or operations.

To summarize, Twitter is expected to see above average Uniform earnings contraction in 2020, which is expected to rebound in 2021. Therefore, as is warranted, the company is trading below peer valuations.

Best regards,

Joel Litman

Chief Investment Strategist

at Valens Research