This company is fighting tooth and nail out of the retail apocalypse

Though most department stores and retailers have struggled to adapt their business around online shopping during the pandemic, some have prospered throughout this process.

Unlike many discretionary clothing purchases, this shoe business is flourishing during the step-up in online shopping. Rating agencies have failed to make the distinction between its business and many other struggling ones in the same industry.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

While online shopping was steadily gaining popularity for the past ten years, it kicked into overdrive in 2020.

Many consumers were forced to do more online shopping than usual during the pandemic. The biggest hurdle for many first-timer online shoppers is simply trying it out – as we highlighted last June, online shopping adoption is fairly sticky once customers have tried it out.

This has put serious long-term pressure on in-store giants like Macy’s (M), leading many investors to be bearish on the whole retail industry.

However, investors need to be wary applying a theme such as the retail apocalypse across the entire industry. While many traditional brick-and-mortar companies will suffer, there are some names who are thriving.

For example, companies like Home Depot (HD) and Best Buy (BBY) had barn-burner years in 2020 thanks to consumers spending more money on home appliances and renovations.

One surprise success story from the retail fashion world is Caleres (CAL).

Caleres is a shoe brand conglomerate that owns retail brands like Famous Footwear and famous shoe brands such as Dr.Scholl’s. The company has already seen its stock price recover to pre-pandemic levels. In comparison to many other traditional retail companies still trading near lows, this is a bright spot in the industry.

Before the pandemic, most investors assumed Caleres would be a company that would fall under the same bucket as other apparel and department store retail businesses, which have struggled this past year.

With more people being active outdoors, combined with stimulus funding disposable income for consumers looking to make a usable purchase, Caleres has seen sales stay steady in the footwear department, especially through online portals.

That being said, major rating agencies are not paying close enough attention to Caleres’ performance to make that distinction between other retail departments.

As a result, the company receives a highly speculative B+ from S&P, with the implied assumption of a 25%+ risk of default over the next five years.

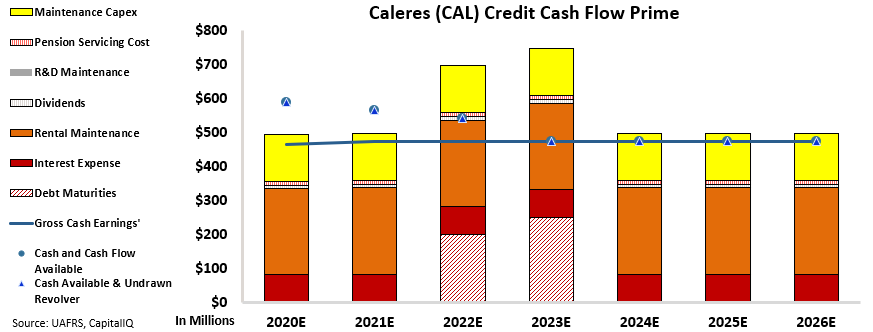

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, Caleres’ credit profile is not as bad as rating agencies make it out to be. The company’s cash flows and available cash can withstand all obligations through the end of this year. This allows Caleres to buy some time before having to refinance their debt that comes due in future years.

Valens sees the reality surrounding this company, which is far less concerning than picture rating agencies paint.

The company’s above cost-of-capital return on assets (ROA), coupled with flexibility in capex spend, shows a much safer picture.

This is why Valens rates Caleres as a safer XO credit rating, which is equivalent to BBB- from S&P.

This rating corresponds with a default rate below 2% within the next five years, a more realistic projection once making the distinction between other struggling retail department stores.

We have a much safer outlook for Caleres’ credit structure because we look at the real data, not the headlines.

SUMMARY and Caleres, Inc. Tearsheet

As the Uniform Accounting tearsheet for Caleres, Inc. (CAL:USA) highlights, the Uniform P/E trades at 21.3x, which is below the global corporate average valuation levels and its historical average valuations of 23.3x.

Low P/Es require low EPS growth to sustain them. In the case of Caleres, the company has recently shown a 67% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Caleres’ Wall Street analyst-driven forecast is a 174% and 6% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Caleres’ $23.85 stock price. These are often referred to as market embedded expectations.

Caleres is being valued as if Uniform earnings were to grow 10% per year over the next three years. What Wall Street analysts expect for Caleres’ earnings growth is above what the current stock market valuation requires in 2022, but below that requirement in 2023.

Furthermore, the company’s earning power is below the corporate average and cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividend. Together, this signals a moderate dividend and high credit risk.

To conclude, Caleres’ Uniform earnings growth is well above peer averages and the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research