Uniform Accounting gives us valuable insights on investing in the lumber trade

Sometimes the most mundane industries can create tremendous value. Today, we will look at a company in the timber and wood products industry.

The as-reported numbers make today’s stock look like a good buy at a cheap price. However, Uniform Accounting shows why that may not be the case.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

When we first founded Valens Research, one of our distribution partners was a broker dealer in New York. The broker dealer shared an office with a timber holding company.

I remember wondering at the time why people had an interest in investing in the timber space… it just seemed so boring. Like any other commodity, lumber lacked differentiation and any other compelling qualities.I remember wondering at the time why people had an interest in investing in the timber space… it just seemed so boring. Like any other commodity, lumber lacked differentiation and any other compelling qualities.

However, given how large the timber industry is, I knew there had to be a reason some of the smartest traders were found in the market.

First, I learned the average American uses the equivalent of a 100-foot tree every year. We use lumber in a range of products that supports constant demand. Americans use trees in furniture, paper products, for smoking meats, and even building fires at home.

In addition, many investors fail to consider the qualities that make timber such a powerful asset.

Timber investors own a “hard” asset, which means it’s a tangible resource that can be directly sold. Unlike other hard assets including gold, copper, and oil, as timber produces cash flows, the value of the business doesn’t fall.

Once an oil well or a metals mine is depleted, it’s gone forever. Meanwhile, timber companies can simply plant new trees and start over.

In addition, the value of unharvested timber increases every year. Larger trees yield more wood, which encourages investors to sit on growing supply.

Timber’s renewable nature makes it a more attractive investment than other hard assets.

Resolute Forest Products (RFP) is a major player in the forest products industry. The firm mainly leases forests in Canada with a small portion of its timber production being fully-owned. Its operations span the full length of timber and wood products from timber harvesting to paper production.

Resolute owns and operates various pulp plants, sawmills, and paper mills to turn its timber into tissue, wood products, kraft paper, and a host of other paper products.

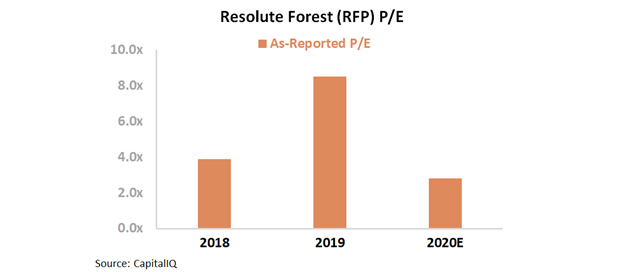

While Resolute doesn’t own all of its timber supply, it has a strong relationship with the Canadian government. In essence, it has a stable, renewable asset base to power all of its operations. investors might be attracted to such a stable business with a 2.5x as-reported P/E ratio. On paper, it appears as though it is a consistent business model for a cheap price.

However, this is not the case. The way GAAP treats special items, among other distortions, is making the company appear to be profitable.

Uniform Accounting shows the firm has a negative P/E ratio. In other words, the company is burning invested capital every year. The Uniform P/E for Resolute is currently -22.5x. While investors already know forestry is a relatively low return industry, a company losing money is far worse.

Uniform Accounting is able to show Resolute is not as attractive of an investment as it looks at first sight. Rather than a smart investment into a cheap company, Resolute is a value trap investors should avoid.

SUMMARY and Resolute Forest Products Inc. Tearsheet

As the Uniform Accounting tearsheet for Resolute Forest Products Inc. (RFP:USA) highlights, the Uniform P/E trades at -22.5x, which is below the global corporate average valuation levels and its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Resolute Forest Products, the company has recently shown a 168% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Resolute Forest Products’ Wall Street analyst-driven forecast is an EPS growth of 46% in 2020 and no growth in 2021.

Furthermore, the company’s earning power is below corporate average. Additionally, cash flows and cash on hand will fall short of its total obligations—including debt maturities and capex maintenance. Together, this signals a high credit risk.

To conclude, Resolute Forest Products’ Uniform earnings growth is well above peer averages. However, the company is trading significantly below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research