Uniform Accounting indicates this mission-critical part of the semiconductor industry is more profitable than the market realizes

Semiconductor production is a complex task, where small mistakes threaten to ruin the whole process. That’s why it’s vital to ensure production runs smoothly and the chips do not get contaminated.

Today’s firm helps semiconductor companies perform this critical function. And yet, it appears to have average returns at best. Uniform Accounting shows how profitable this firm really is.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Making semiconductor chips is a complicated process. Semiconductor producers do not make chips individually, but in large batches.

Semiconductors are made in sequence, as wires and devices on the chip are fabricated at the same time as thousands of other chips. On an assembly line, there is only a small difference in cost to produce 100 chips versus 1,000.

This means manufacturers can achieve economies of scale in production. The more chips they produce, the cheaper it becomes on a per chip basis.

This allows them to produce chips at a low cost in bulk, despite their complexity.

However, this batch production also increases the potential for large scale mistakes. Chips can be exposed to chemical contamination that effectively ruins the product. If there is any contamination, the entire batch will have to be thrown out. By contrast, smaller scale production is lower risk, but more expensive per chip.

Large-scale contamination can lead to costly mistakes, where thousands of chips might need to be thrown out after the introduction of one contaminant.

Therefore, it’s crucial to ensure the production process runs smoothly. Entegris (ENTG) is integral to the protection process.

The company makes products that purify, protect, and transport key materials used in semiconductor fabrication. It’s goal is to increase batch yields by improving contamination control. This means more semiconductors reach their end destination without having to be scrapped.

Entegris’ success is closely tied to the semiconductor industry’s success. As technology becomes increasingly complex, The company’s services are becoming even more essential.

Entegris also has a history of acquisitions, including its most recent Global Measurements purchase in July. These rollups have allowed the firm to stay ahead of semiconductor trends and expand its capabilities.

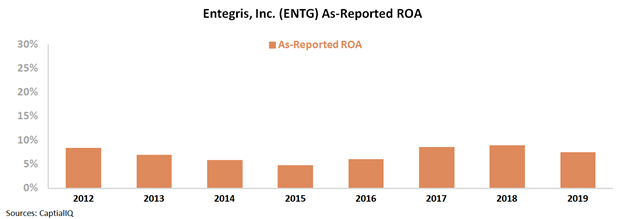

One would assume Entegris should generate a healthy return making products to prevent contamination. Yet looking at as-reported metrics, it appears the company has been unable to capitalize on the success of the semiconductor industry.

As-reported ROA has only ranged from 5% to 9% since 2012. It appears as though the firm has not benefited from the growing importance of semiconductors.

Wall Street assumed Entegris has been unable to differentiate its offerings and charge a premium for its protection of batch yields.

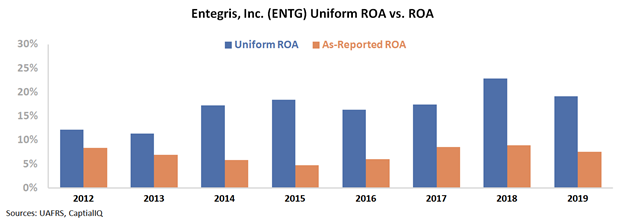

However, this picture of Entegris’ performance is not accurate. This is due to distortions in as-reported accounting, including the treatment of amortization and interest expense, among other distortions. Wall Street has missed the mark on Entegris’ profitability.

Entegris’ Uniform ROA has been double as-reported numbers since 2013. Uniform ROA also improved from 12% in 2012 to 19% in 2019, while as-reported ROA remained flat over the same period.

Entegris has leveraged its essential nature in a growing industry to generate above average returns.

Without Uniform Accounting, investors would miss the strong returns of this semiconductor protection business. They might see Entegris as a firm with average and stagnating returns instead of robust profitability.

Ultimately, Entegris should continue to benefit from tailwinds in the semiconductor industry due to its essential nature in protecting against contamination.

Importantly, this insight is not just helpful for investors to know. It’s also important for management to decide whether to reinvest in the business and take on certain projects. If they are looking at bad data, their decision making will be flawed.

SUMMARY and Entegris, Inc. Tearsheet

As the Uniform Accounting tearsheet for Entegris, Inc. (ENTG:USA) highlights, the Uniform P/E trades at 28.7x, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. In the case of Entegris, the company has recently shown an 8% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Entegris’ Wall Street analyst-driven forecast is an EPS growth of 36% and 15% in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Entegris’ $87 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow 16% per year over the next three years. What Wall Street analysts expect for Entegris’ earnings growth is above what the current stock market valuation requires in 2020, but below its requirement in 2021.

Furthermore, the company’s earning power is 3x the long-run corporate averages. Additionally, cash flows and cash on hand are 4x its obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Entegris’ Uniform earnings growth is slightly below peer averages, but the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research