Uniform Accounting shows that once this firm monetizes its massive asset base, returns could double, bullish for the bonds and equity

This firm has a massive asset on the books that has dragged down returns recently. However, it is in a prime position to monetize that asset and see returns get back to prior levels, or over double where they are now.

As-reported financials miss that though, and don’t see how high this company’s cash flow ceiling is, leading creditors to overstate risk.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

We often talk with clients about distinguishing between “operating”and “non-operating” assets. All show up on the as-reported balance sheet, but it can distort our view of a company’s real profitability if the majority of assets aren’t used in operations.

One poster child for “non-operating” asset adjustments is Apple.

As we discussed yesterday, the company generates so much money at such high margins from selling iPhones, AirPods, and other hardware that it cannot possibly find enough profitable projects to use up all of its extra cash.

Inherently, companies need some level of cash to keep their businesses running. After that, we consider any leftover money to be “excess cash.” One of our major adjustments under Uniform Accounting is to remove excess cash and non-operating assets from the balance sheet, since these don’t reflect a company’s real profitability.

We instead include those as a separate asset that an investor gets when he or she buys stock in the business.

Because of Apple’s nearly $200 billion in cash and non-operating investments alone, ROA for the firm can look as much as 5 times smaller than it actually is.

But Apple is far from the only company impacted by non-productive assets pulling down returns…

DISH Network (DISH) has been another great example.

However, DISH’s non-productive asset isn’t “non-operating” like Apple’s cash. We can’t comfortably remove it from DISH’s balance sheet saying it isn’t really an operating asset, since it’s an asset the business plans to use.

It just isn’t productive…yet.

While the company is most known for its satellite TV offering, it also owns a large portion of wireless spectrum that currently isn’t generating returns. DISH bought the licenses, but hasn’t built a business to use the spectrum.

Back in 2013, DISH attempted to buy Sprint (S) to enter the wireless provider business. While the attempt was unsuccessful, DISH has continued spending much of its excess cash on wireless spectrum.

At this point, DISH’s portfolio of largely unused wireless spectrum is worth nearly $20 billion. The company figured it would be able to enter the wireless provider space or sell the spectrum to another provider, but neither has happened.

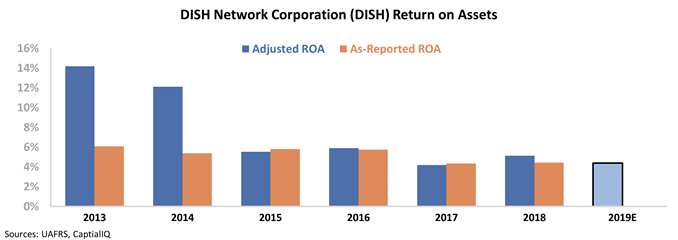

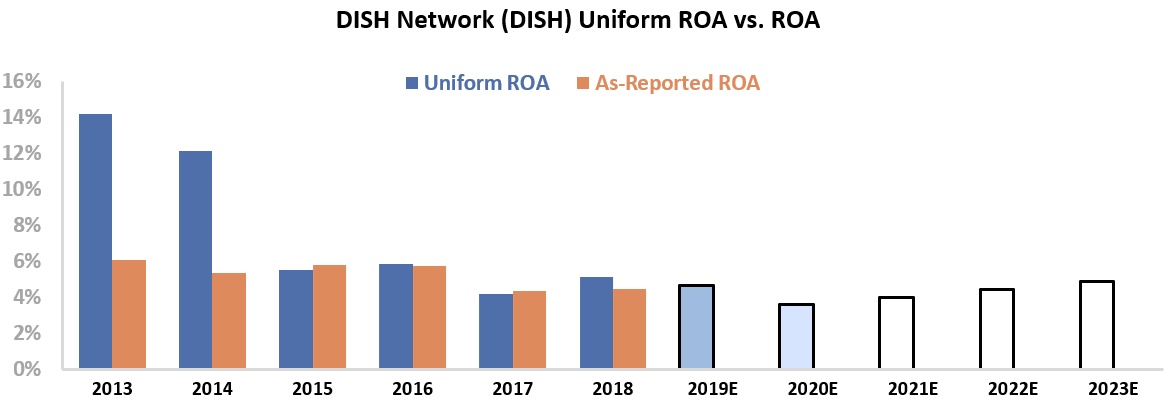

As a result, the firm has seen returns fall by half from 2013-2014 levels:

However, not all hope is lost. As part of Sprint and T-Mobile’s (TMUS) ongoing merger, DISH has agreed to acquire certain assets from both businesses to become another major wireless carrier.

When this happens, DISH will finally be able to monetize all of the wireless assets that are currently collecting dust on its balance sheet.

This may lead returns back to historical levels.

Using as-reported financials would lead one to believe that returns don’t have much room to rebound, as returns are largely at levels seen since 2013. But under Uniform Accounting, it is clear that when the firm is able to monetize these assets, returns could double or more.

Credit investors who are looking at DISH’s as-reported financials see a company with loads of debt and poor cash flows that have little room to improve. That’s why the company’s bonds had been yielding over 5% before wider credit concerns caused yields to rise above 8%.

However, it’s clear that there is plenty of room for improvement, and if DISH can navigate the next few years, there should be little risk to its status as a going concern.

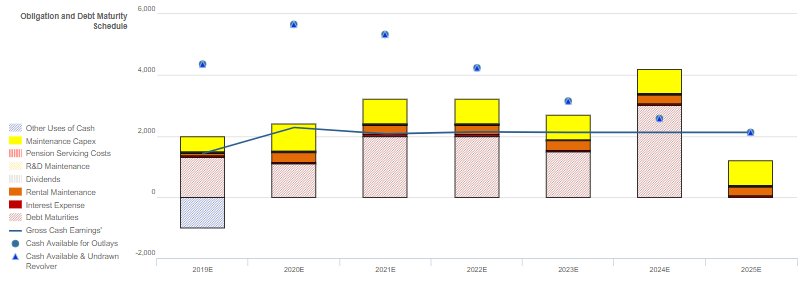

Looking at the firm’s cash flows and obligations going forward, it has the liquidity to service obligations through 2023. More importantly, that whale of a wireless asset on its balance sheet gives it more than enough asset backing to refinance its debt as needed.

These factors are part of the reason we think the company’s bonds are much safer than they initially appear.

Given the liquidity and potential for refinancing, it is clear that DISH has more than enough time to work on monetizing its new assets.

Should cash flows return to historical levels, understated by as-reported financials, there is no doubt the firm will be able to remain a going concern. As a result, credit markets and ratings agencies are clearly overstating risk currently, giving investors an opportunity.

DISH’s Operational Sustainability and Healthy Liquidity Indicate Tighter Bond Spreads Going Forward

Credit markets are materially overstating credit risk, with a cash bond YTW of 5.399% relative to an Intrinsic YTW of 2.899% and an Intrinsic CDS of 119bps.

Furthermore, Moody’s is overstating DISH’s fundamental credit risk, with its Ba3 rating three notches lower than Valens’ XO (Baa3) rating.

Fundamental analysis highlights that DISH’s cash flows would fall short of operating obligations in each year going forward until 2024.

Although, the combination of the firm’s cash flow and cash on hand should be sufficient to cover all obligations including debt maturities until 2024, when the firm faces a significant $3 billion debt headwall.

Though they will need to refinance to avoid a liquidity crunch, the firm has several years to improve operations and ample flexibility to temporarily reduce capex to service all obligations through 2025.

Furthermore, DISH’s robust 180% recovery rate and sizable market capitalization should allow them to access credit markets to refinance.

Incentives Dictate Behavior™ analysis highlights mixed signals for credit holders. DISH’s compensation framework should drive management to improve all three value drivers, which should lead to Uniform ROA expansion and greater cash flows available for servicing obligations.

Moreover, management members have no change-in-control compensation, indicating that they are not well-incentivized to accept a buyout or pursue a sale of the company, reducing event risk.

However, other than Chairman Ergen, management members are not material holders of DISH equity relative to their annual compensation, meaning they may not be well-aligned with shareholders for long-term value creation. In addition, the Ergen Family owns a large portion of DISH’s outstanding common stock shares, and they may be able to steer the company in any direction they choose.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (11/7) highlights that management may be concerned about the profitability impact of Disney’s contract termination, and they may lack confidence in their ability to reduce their capex spend through cloud adoption.

Furthermore, they may be downplaying the impact of seasonality on the growth of Sling, and they may lack confidence in their ability to continue driving customer adoption of their portfolio.

Given DISH’s operational sustainability, current cash liquidity, and robust recovery rate, credit markets and Moody’s are overstating the firm’s fundamental credit risk.

As such, a tightening of credit spreads and a ratings improvement are likely going forward.

SUMMARY and DISH Network Corporation Tearsheet

As the Uniform Accounting tearsheet for DISH Network Corporation (DISH) highlights, the company trades at a 34.1x Uniform P/E, which is above global corporate average valuation levels and its historical average valuations.

High P/E’s only require high EPS growth to sustain them. That said, in the case of DISH, the company has recently shown a 33% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, DISH’s Wall Street analyst-driven forecast declines by 11% into 2019, which will further decline by 29% in 2020.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $19 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for DISH, the company would just have to have Uniform earnings grow by 4% each year over the next three years.

Wall Street analysts’ expectations for DISH’s earnings growth are far below what the current stock market valuation requires in 2019 and 2020.

In addition, DISH’s Uniform earnings growth is in line with peer average levels, while the company is trading above peer valuations.

Meanwhile, the company’s earnings power is in line with corporate averages, signaling an average risk to its dividend or operations.

To summarize, DISH is expected to see below average Uniform earnings growth in 2019, which is expected to decline further in 2020. Furthermore, the company is trading above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research