Uniform Accounting shows what’s cooking for Newell Brands during the pandemic

We’ve mentioned time and time again how At-Home Revolution companies are winning during the pandemic. Products for your home are selling like hotcakes.

As-reported metrics would have you believe today’s company has poor returns despite being a great At-Home Revolution candidate, but true UAFRS (Uniform) based analysis shows the firm’s real profitability.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The “At-Home Revolution” is changing consumer trends and habits. We saw this when the pandemic began and people began baking bread and other treats. With people stuck at home and many restaurants closed, baking and cooking have been a great way to pass the time.

To accomplish all this cooking, people need the proper supplies. Not only are the ingredients important, the correct machinery and storage equipment are musts. Because of this, there has been increased demand for storage containers and machines like air fryers, the exact types of products Newell Brands (NWL) sells.

Newell is a diversified company with dozens of brands in its portfolio. Under its Appliances and Cookware segment, it owns brands like Oster, Calphalon, and Crockpot. With these brands, Newell offers most of what any home cook or baker needs to finish their recipes.

Additionally, the firm owns a number of brands under its Food segment, including Rubbermaid, FoodSaver, and Sistema. All of these brands help customers store their food in an efficient manner and for extended periods of time.

Combined, these two segments present a one-stop-shop for consumers looking to cook during the pandemic.

In addition, these segments are not the only ones bolstered by the pandemic. Newell also owns a number of brands students use in school. These include Elmers, Paper Mate, and Sharpie.

Given how many students are taking classes remotely, it’s no surprise back-to-school spending jumped this year. Students need all their supplies at home and can’t rely on borrowing supplies from a teacher or classmate.

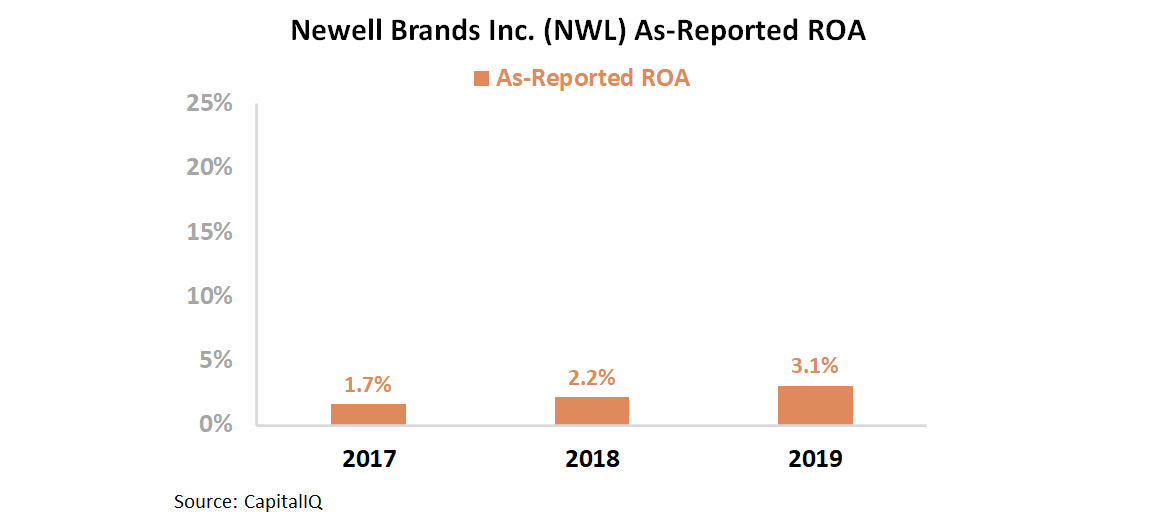

Due to its portfolio, it looks like Newell is primed to benefit from the At-Home Revolution. However, investors may be wary of the firm because of its as-reported returns. According to as-reported ROA, the firm appears to have returns below cost-of-capital levels.

Over the past three years, as-reported ROA has been stuck between 2% and 3%. Because of this, investors might not think increased demand from the pandemic will help the firm see returns rise above the cost of capital.

However, this is an inaccurate depiction of the firm’s performance. GAAP accounting is both understating the firm’s earnings and overstating net assets. This is due to GAAP’s treatment of line items like goodwill and interest expense, among other distortions.

Uniform Accounting shows Newell has had robust returns over the past three years, well in excess of corporate averages, let alone the firm’s cost of capital.

Newell has been able to take advantage of its diversified portfolio, which has helped it sustain consistent and high returns even as consumer habits have changed. Since the firm operates across a number of home-centered product lines including Outdoor, Home Fragrance, Home Security, Food, Appliance, and Commercial, it has substantial tailwinds this year and in the future.

Newell’s Uniform ROA has been strong in the last three years, ranging between 16% and 23% in 2017-2019. Furthermore, the firm is set to take advantage of tailwinds from the coronavirus pandemic.

Uniform Accounting is able to show how Newell Brands has taken advantage of its large portfolio. Additionally, the pandemic is providing tailwinds to a number of the firm’s segments. With the end to the pandemic still likely months away, more baking and online school may continue to benefit the firm well into 2021.

SUMMARY and Newell Brands Inc. Tearsheet

As the Uniform Accounting tearsheet for Newell Brands Inc. (NWL:USA) highlights, the Uniform P/E trades at 14.5x, which is below global corporate average valuation levels and its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Newell, the company has recently shown a 43% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Newell’s Wall Street analyst-driven forecast is a 4% EPS decline in 2020, followed by a 16% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Newell’s $21 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 7% for each of the next three years and still justify current stock prices. What Wall Street analysts expect for Newell’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x corporate averages. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a high credit and dividend risk.

To conclude, Newell’s Uniform earnings growth is in line with peer averages, but the company is below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research