Whether or not cash will remain king, this company will continue thriving

One common phrase in the finance world is “Cash is King.” While historically true, many pundits argue that digital payments and currencies might change the game.

Despite the pandemic making cash less important than it has ever been, today’s company is an important part of why cash is still a cornerstone of the financial world.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

For years, cash has been referred to as king, with investors often making remarks similar to “Cash is King.”

Despite this, in the midst of the pandemic, investors are calling cash’s importance into question. The pandemic has accelerated adoption of cashless solutions such as venmo, PayPal, and other platforms.

Cash is by no means dead though. One reason cash is so powerful has been the reduction in the cost of cash created by banks over the past decade, coupled with the adoption of ATMs.

Cash is still the most popular method of payments, as the basis for around 30% of all transactions. This means customers need to make frequent stops at ATMs to restock on their purchasing power.

ATMs allow citizens to easily access their cash. These machines also save banks money as fewer tellers are needed to give out cash.

A key company at the forefront of providing ATM services and payment vendor services is NCR Corporation (NCR).

The company dates back to the 1880s, when it was the first to mass produce cash registers. Ever since, NCR has been at the forefront of cash management and point-of-sale technology, creating everything from ATMs to self-serve check-out kiosks.

All of these automated cash procedures made banks more efficient at making and keeping money.

With its valuable services and the increased adoption of ATMs over the years, investors might suspect NCR to have a robust return on assets (ROA). The firm helped cash remain king in an asset-light manner.

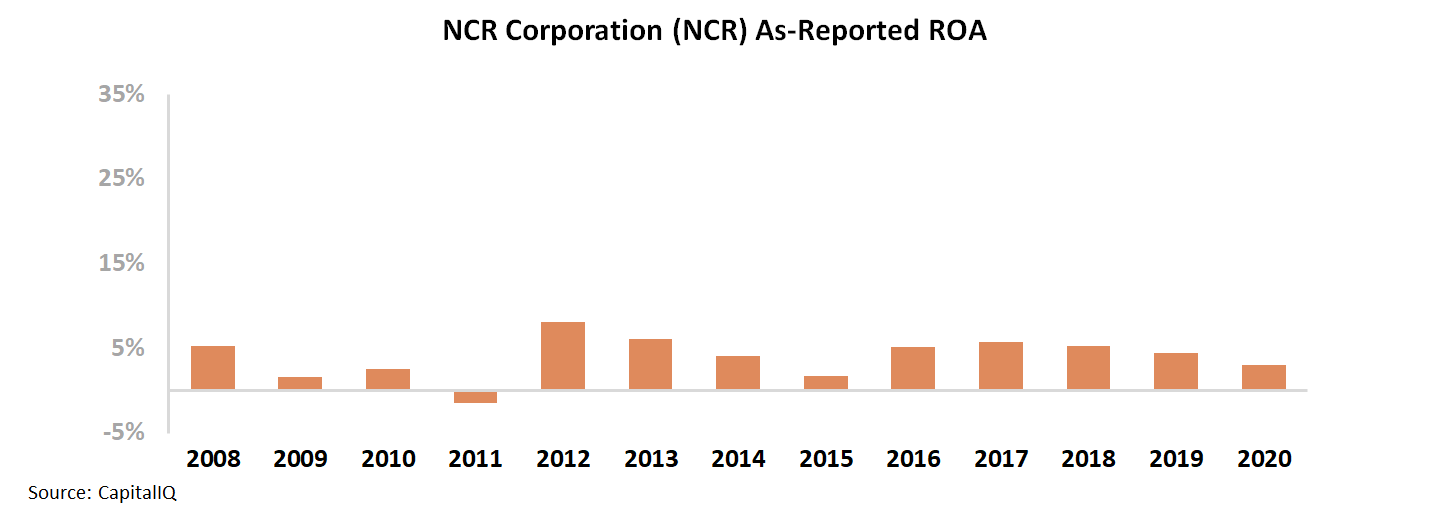

However, only looking at NCR’s as-reported data, investors would conclude the business is anything but profitable.

NCR’s ROA has been weak, making investors think the company has not offered any services banks would pay a premium for. Specifically, after expanding from 5% in 2008 to a peak of 8% in 2012, as-reported ROA has trended downward through 2020.

See for yourself below.

Additionally, with the pandemic making cash less important than it has ever been, investors might believe a company like NCR would be set up for failure.

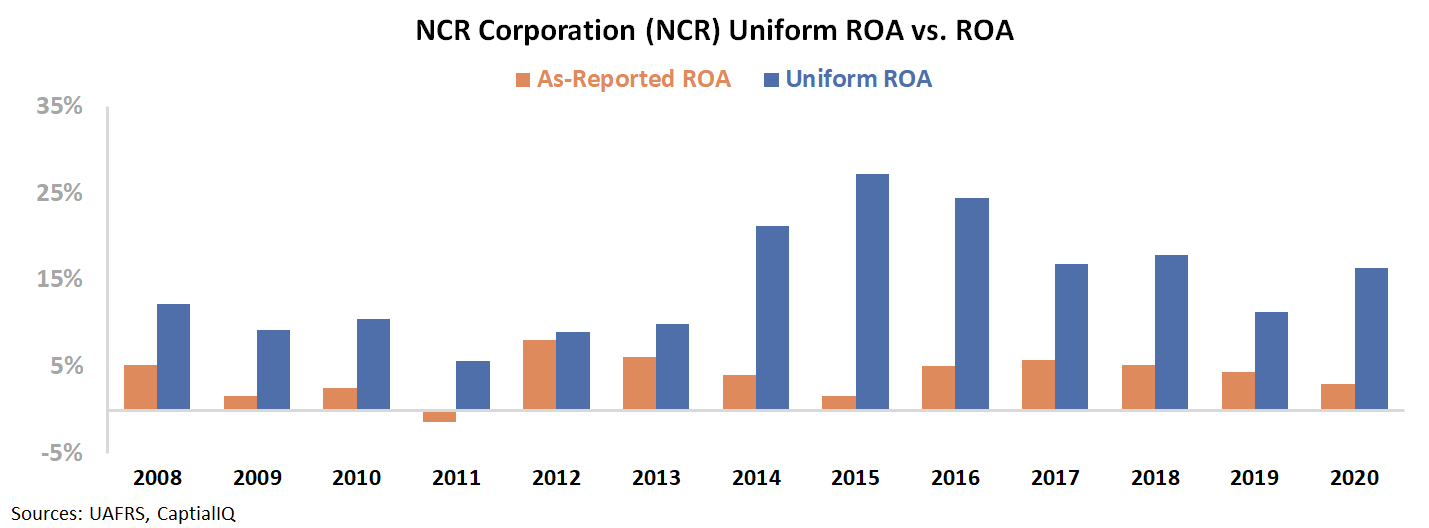

In reality, this is not an accurate picture of NCR’s performance. The firm does have higher than average returns.

When looking through a Uniform Accounting lens, it becomes clear that banks are willing to pay a premium to NCR to save money on expensive operating costs.

Specifically, Uniform ROA has not declined since 2008, but has actually expanded from 12% levels in 2008 to 16% in 2020.

As NCR offers payment processing services across the board, the firm does, in fact, add value to banks. This supports the strong history for NCR’s robust Uniform ROA levels.

Even in the current environment, Uniform ROA is likely to remain at strong levels.

Without Uniform Accounting, investors would be unsure of the value this firm has to offer, especially with the discussion revolving around the value of cash.

While the verdict is still out on whether cash will remain king, NCR has seen robust growth in Uniform returns as it continues to help banks reduce costs.

SUMMARY and NCR Corporation Tearsheet

As the Uniform Accounting tearsheet for NCR Corporation (NCR:USA) highlights, the Uniform P/E trades at 18.4x, which is below the global corporate average of 25.2x, but around its own historical average of 17.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of NCR, the company has recently shown a 63% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, NCR’s Wall Street analyst-driven forecast is a 23% EPS shrinkage in 2021, followed by a 23% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify NCR’s $35 stock price. These are often referred to as market embedded expectations.

NCR is currently being valued as if Uniform earnings were to shrink 8% annually over the next three years. What Wall Street analysts expect for NCR’s earnings growth is below what the current stock market valuation requires in 2021, but above its requirement in 2022.

Furthermore, the company’s earning power is 3x the long-run corporate average. Also, intrinsic credit risk is 380bps above the risk-free rate and cash flows and cash on hand are slightly above its total obligations—including debt maturities and capex maintenance. All in all, this signals a moderate credit risk.

To conclude, NCR’s Uniform earnings growth is in line with its peer averages, and the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research