Investment gurus have stressed the importance of this resource over both oil and gold

Over the past 10 years, some of the biggest investing gurus have moved away from gold and oil into another natural resource used by billions of people daily.

Only a select number of public companies service this resource, so it seems like an opportunity to generate strong returns.

As-reported metrics highlight that today’s firm has seen profitability hover around the corporate average since 2010, but Uniform accounting tells a different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Whether predicting the downfall of the modern economy or simply a return to “hard” investments, many investment gurus insist it’s important to own natural resources like gold and oil.

In recent years, certain pragmatic investors have called out gold and oil as being far less valuable than clean drinking water. Clean water is a human necessity, and due to population growth, pollution, and depleting aquifers, clean water is becoming more scarce and precious each year.

Additionally, climate change is impacting the water cycle around the world.

After successfully calling the subprime mortgage crisis, Dr. Michael Burry has been investing in water. While it seems water is plentiful, only 1% of the Earth’s water is currently potable. Moreover, 21 of the world’s 37 aquifers are depleted, with an estimated 66% of the world’s population to be living in water stressed areas by 2025.

With access to clean drinking water such an immediate concern, it’s only logical investors would turn to the companies who dominate the space. Now that water is being traded on the Chicago Board of Exchange, clean water companies should be able to fetch premium returns.

A large player driving smart solutions to water access is Xylem (XYL). Xylem works across most of the water supply chain, from pre-delivery testing all the way to post-consumption wastewater transport.

Xylem’s services are a necessity to our modern society, meaning the company should have some level of pricing power. However, over the past decade, it appears the company has barely been able to yield returns higher than its cost of capital.

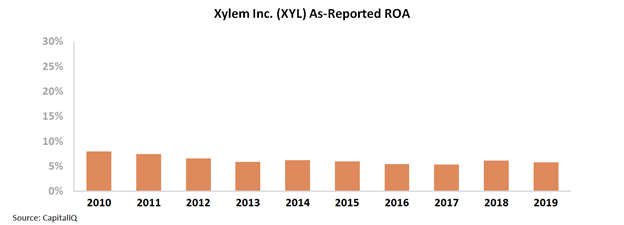

From 2010 to 2019, the company has seen its as-reported ROA slowly fade from 8% to 6%. Looking at these metrics, Xylem can just be seen as an average business that is struggling to generate earnings power.

While these weak returns could be explained by regulatory pressures or lower-than-expected demand, the reality that most investors are missing out on is that Xylem looks bad due to as-reported accounting.

Once we make the necessary Uniform Accounting adjustments to line items like goodwill, operating leases, and other distortions, we can see Xylem has in fact generated returns well above corporate average levels. By providing clean water solutions, Xylem has earned a premium return.

Over the past seven years, Uniform ROA has risen from 16% to 23%. Since 2010, Uniform ROA has remained well above corporate average returns.

When identifying this firm through the lens of Uniform accounting, it is no wonder that over the past five years Xylem has seen steady appreciation in the stock market from around $40 in 2016 to around $100 today.

While as-reported financial metrics make Xylem look like an average company without any real leverage or pricing power, Uniform Accounting helps reveal what investors like Dr. Burry already know.

Xylem offers services that will only continue to grow more important to our society, and with that, its returns are likely to stay strong in the future.

SUMMARY and Xylem’s Company Tearsheet

As the Uniform Accounting tearsheet for Xylem Inc. (XYL:USA) highlights, the Uniform P/E trades at 37.8x, which is above global corporate average valuation levels and its historical averages.

High P/Es require High EPS growth to sustain them. In the case of Xylem, the company has recently shown a 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Xylem’s Wall Street analyst-driven forecasts are 48% EPS shrinkage and 44% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Xylem’s $103 stock price. These are often referred to as market embedded expectations.

The company would need to grow its Uniform earnings by 8% per year over the next three years to justify current stock prices. What Wall Street analysts expect for Xylem’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

Furthermore, the company’s earning power is 4x the corporate average. Also, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Xylem’s Uniform earnings growth is below its peer averages, but the company is trading above peer average levels.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research

View All