Meritor Merits Investment Grade, While Equity Markets Expect ROA’ to Decrease

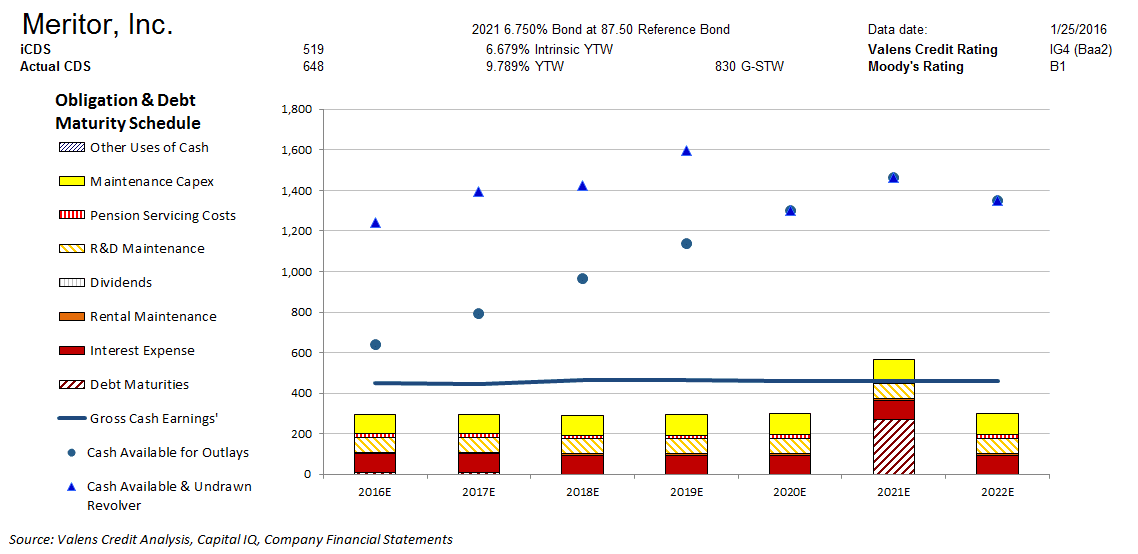

Moody’s is materially overstating the credit risk of Meritor, Inc. (NYSE:MTOR) with its B1 rating. However, Valens’ fundamental analysis highlights a much safer credit profile for MTOR. The company’s cash flows cover all their obligations through the next seven years, except for their 2021 debt headwall that their cash build can easily cover. Valens therefore rates MTOR five notches higher at an IG4 credit rating or a Baa2 using Moody’s ratings scale.

In addition, cash bond markets are grossly overstating MTOR’s credit risk, with a cash bond YTW of 9.789% relative to an Intrinsic YTW of only 6.679%. CDS markets are likewise overstating credit risk, with a CDS of 648bps versus an Intrinsic CDS of 519bps.

Equity markets share credit’s bearish outlook, with MTOR trading at a 1.3x V/A’, and a 10.7x V/E’, both at the low end of valuations since 2009. Market expectations are for ROA’ to decrease from last year’s 11% levels to 9% levels. However, the firm has been able to sustain 10%-11% ROA’ levels since 2013 and analysts project ROA’ to grow to 13% going forward. Considering low market expectations and low valuations relative to history, MTOR equity appears undervalued.

Click here to read the article in its entirety at Seeking Alpha.