Moody’s Continues To Disregard Valeant’s Safer, Investment Grade Credit, While Equity Markets Expect Material ROA’ Compression

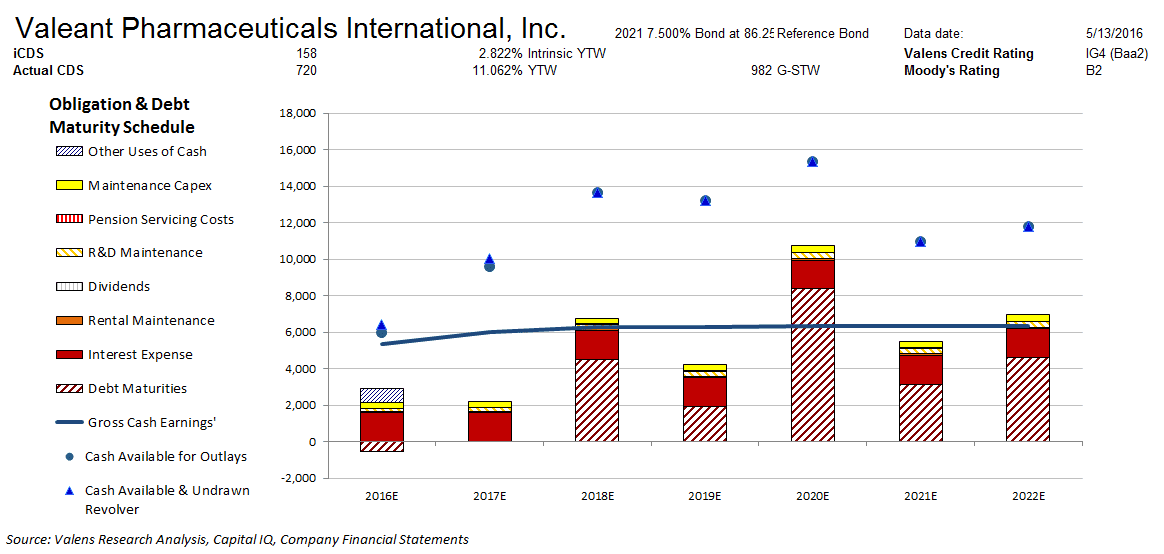

Moody’s is materially overstating the credit risk of Valeant Pharmaceuticals International, Inc. (TSX:VRX) with its B2 rating. Our fundamental analysis highlights a much safer credit profile for VRX, whose strong cash flows cover all operating obligations going forward. Moreover, their healthy liquidity profile would allow them to service all obligations including debt maturities. We therefore rate VRX six notches higher at an IG4 credit rating, or a Baa2 equivalent using Moody’s ratings scale.

Meanwhile, credit markets are grossly overstating credit risk with a CDS of 720bps relative to an Intrinsic CDS of 158bps, and a cash bond YTW of 11.062% relative to an Intrinsic YTW of 2.822%.

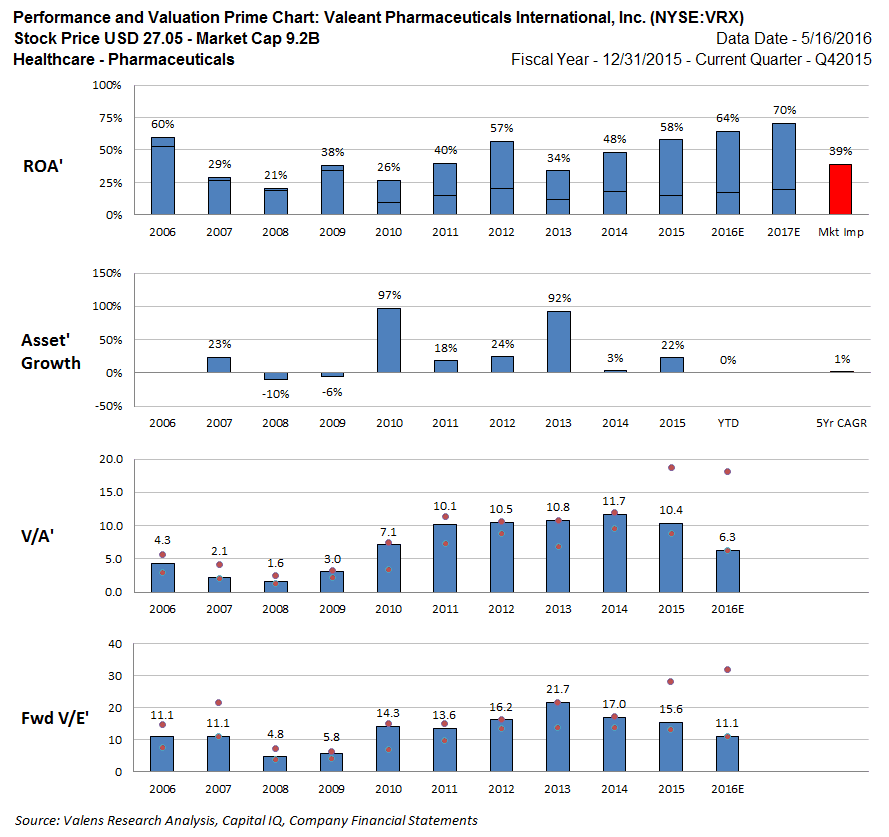

On the other hand, VRX is trading at an 11.1x V/E’, which is at the low end of recent valuations. The market expects a material ROA’ compression from 2015 levels of 58% to 39%, with 1% Asset’ growth going forward. Multiples for VRX materially declined following allegations of fraud, and have continued to compress as the company has come under fire due to their late 10-K filing and subsequent restatement. If the allegations of fraud are found to be unwarranted, there would be material potential equity upside even with potential drug price legislation.

Click here to read the article in its entirety at Seeking Alpha.