Building a diverse set of properties helped this company become one of the biggest titans in its industry, reaching Uniform ROAs of 7%, not 5%

Having a diverse property portfolio has proven to be essential to the survival of the real estate industry, especially during this pandemic.

This property titan has been able to navigate through this unstable environment with nothing but a minor scratch on it thanks to its portfolio. However, looking at its as-reported metrics, it seems that mainly focusing on its expansion initiatives in the past hasn’t been enough to achieve above cost-of-capital returns.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

In 1968, 16-year-old Andrew Tan and his parents migrated from Hong Kong to the Philippines to start a better life. His father was able to get a job at a transistor radio factory where Andrew also spent most of his time helping and earning extra income for his family.

Through his father’s hard work, Andrew was able to study accounting in the University of the East. It wasn’t an easy feat because they didn’t have a lot of money, so he saved as much as he could and found ways to earn money in his own way.

One of Andrew Tan’s dreams was to put up a small grocery store. Little did he know that 30 years later, he would go on to become one of Forbes’ richest men in the country, owning some of the biggest and most successful Phlilippine companies to date.

Andrew Tan was able to make a name for himself by building his empire from the ground up and successfully engaging in different business industries—such as food and beverage, hospitality, and real estate. He took the lead on bringing the McDonald’s franchise to the Philippines, and he also penetrated the liquor market by introducing brandy through the creation of Emperador Inc. (EMP:PHL).

However, before putting up those big businesses, Andrew Tan had to start small. With the little capital that he had from working as an employee for years, he decided to establish his first real estate company, Megaworld Corporation (MEG:PHL).

Incorporated in 1989, Megaworld initially focused on only developing high-end residential properties and condominiums. However, after seeing a growing demand for community township developments, the company immediately jumped at the sight of the opportunity and launched its first township, Eastwood City, in 1996.

In a span of three decades, Megaworld was able to launch 26 townships, which includes Mckinley Hill and Newport City in Metro Manila. To further widen its reach, the company also developed the Mactan Newtown and Iloilo Business Park in Visayas, as well as the Davao Park District in Mindanao.

The company continued to expand by venturing into the commercial properties business. Shortly after the success of Eastwood Mall, it created Megaworld Lifestyle Malls in 2009. The commercial arm of the company currently has eight malls under its belt—consisting of Uptown Mall in BGC, Venice Grand Canal Mall in McKinley Hill, and Lucky Chinatown in Binondo, to name a few.

The firm’s expansion did not stop there.

Like Robinsons Land Corporation (RLC:PHL), Megaworld also saw an increasing demand for hotels and business process outsourcing (BPO) companies in the country. This encouraged the company to launch its office leasing arm Megaworld Premier Offices, as well as other hotel projects, which further diversified its revenue stream.

Through the years, Megaworld has developed a sense of resiliency for its business, giving it the ability to withstand several crises that occured in Philippine history, particularly the coup d’etat during Cory Aquino’s administration and the 2008 Financial Crisis.

In 2020, however, it faced a different kind of problem: the COVID-19 pandemic.

The company experienced several setbacks as the government implemented lockdown protocols that led to Megaworld’s 25% decline in consolidated revenue from PHP 31.7 billion to PHP 23.8 billion in H1 2020.

Despite facing headwinds and uncertainties, Megaworld continued to fight the pandemic head on by focusing on its recovery efforts and planned expansion projects for the year. These project launches include the Pinnacle at Iloilo Business Park, One Manhattan at the Upper East in Bacolod, and Lakefront Esplanade at Hamptons Caliraya.

Moreover, the company focused on strengthening its BPO business since the majority of Megaworld’s corporate clients still occupy around 90% of its spaces, even at the height of the lockdown. Ongoing talks of expansion deals are also underway for Metro Manila-based BPOs that are looking to open their offices in the company’s provincial townships.

Megaworld’s diversified property portfolio and its high-demand nature make it easier for the company to carry out its expansion initiatives. However, looking at as-reported metrics, it appears its growth resulted in meager profitability, with return on assets (ROAs) only reaching a peak of 5%.

In reality, thanks to the company’s focus on its portfolio expansion strategy, it has been able to achieve higher ROAs than as-reported. Uniform ROAs have been above cost-of-capital levels, reaching more than 7% in the past sixteen years.

One of the distortions between Uniform and as-reported ROAs comes from as-reported metrics failing to consider how current liabilities are factored into the ROA calculation. Traditional ROA calculations for measuring a firm’s earning power only include current and long-term assets as part of the cost of investment.

However, a company’s ability to receive goods and services in advance of payments–the current operating liabilities–ought to be factored in as well.

Current liabilities (excluding short-term debt) are necessary for operations. Items such as accounts payable, accrued expenses, and others are used to maintain the firm’s current capital position. On the other hand, long-term liabilities are mostly just used to finance the business.

If a company has a ton of cash to service its current liabilities and we only factor in its cash and not its current liabilities, it would make the company look inefficient. In reality, the company is just being responsible by building liquid assets to meet short-term obligations.

As such, net working capital (current assets – current liabilities) is used for the firm’s ROA calculation. This shows a company’s real cash management ability and thereby, its true earning power.

In the case of Megaworld, as-reported metrics’ asset base for ROA calculation is at PHP 349.6 billion in 2019, leading to a 5% as-reported ROA. However, when subtracting current operating liabilities and applying other necessary adjustments, we arrive at the company’s PHP 271.3 billion Uniform assets, resulting in a 7% Uniform ROA.

Megaworld’s earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Megaworld’s profitability has been weaker than real economic metrics have highlighted in the past sixteen years.

In reality, Megaworld’s true profitability has been higher than as-reported ROA since 2004. Specifically, Uniform ROA was 7% in 2019, but as-reported ROA was only 5% that year. Though this difference may seem small, it’s actually the difference between a profitable company and a company barely earning enough to cover its cost of capital.

After expanding from 1% in 2004 to 3%-4% levels in 2008-2016, as-reported ROA improved to 5% levels in 2017-2019.

In contrast, after declining from a peak of 9% in 2004 to 6% in 2007, Uniform ROA expanded to 8% in 2009, before compressing to 5%-7% levels through 2019.

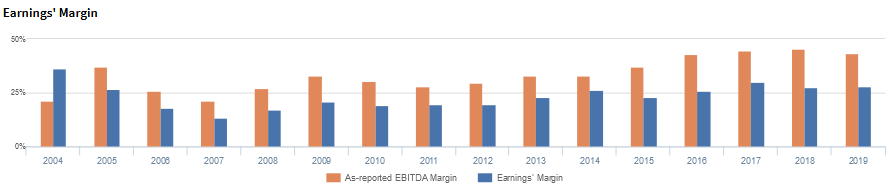

Megaworld’s earnings margin is weaker than you think

Trends in Uniform ROA have been primarily driven by trends in Uniform earnings margin.

As-reported margins improved from 21% in 2004 to 37% in 2005, before fading back to 21% in 2007 and subsequently recovering to 33% through 2009. Thereafter, as-reported margins declined to 28% in 2011 before expanding to 44%-45% levels in 2017-2019.

Meanwhile, Uniform margins declined from a peak of 36% in 2004 to a low of 13% in 2007, before compressing back to 19%-21% levels in 2009-2012 and rebounding to 30% in 2017. Since then, Uniform margins regressed to 28% in 2019.

Looking at the firm’s margins alone, as-reported metrics are making the firm appear to be a more cost efficient business than is accurate.

SUMMARY and Megaworld Corporation Tearsheet

As the Uniform Accounting tearsheet for Megaworld Corporation (MEG:PHL) highlights, it trades at a Uniform P/E of 16.2x, below the global corporate average of 25.2x, but around its historical average of 17.5x.

Low P/Es require low EPS growth to sustain them. In the case of Megaworld, the company has recently shown an 11% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Megaworld’s sell-side analyst-driven forecast calls for a 44% Uniform EPS decline in 2020 and a 46% Uniform EPS growth in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Megaworld’s PHP 4 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 6% each year over the next three years and still justify current valuations. What sell-side analysts expect for Megaworld’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is slightly above the long-run corporate average, and cash flows and cash on hand are twice its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, Megaworld’s Uniform earnings growth is in line with its peer averages, but the company is trading below peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under UAFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com