By docking all assets in the Philippines, this port operator has been capturing the country’s growth and generating Uniform returns of 17%

Last year stressed how crucial trade was to the Philippine economy and it wouldn’t have been possible without the normal functioning of ports.

This port operator has been generating robust Uniform returns by capturing the country’s flourishing trade. However, as-reported metrics are only showing modest profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Philippine Markets Daily:

Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus

Powered by Valens Research

Every country wants to be economically independent or to be able to satisfy the country’s entire demand domestically. This is especially true for the production of staple foods, such as rice in the Philippines’ case.

The desire for economic independence stems from the prevalent use of trade policies for political purposes, in the form of free trade agreements, tariffs, and others.

Historically, the Philippines has been no stranger to harsh economic policies, as colonial invaders have used such methods to control the country.

More recently, we’ve been seeing the United States and China, the two largest economies and also the Philippines’ two largest trade partners, stretch their economic muscles against one another.

However, regardless of how trade wars play out, both sides are always worse off had it not began. It is estimated that the U.S. has lost 250,000 jobs due to the trade war, while China has lost $35 billion worth of exports.

People have realized that global trade is a necessity, which is why many trade organizations have been created. Additionally, it’s no longer possible for one country to single-handedly produce the billions of goods flowing in the economy each year.

Economic experts almost unanimously agree that freer trade would be beneficial for economies. A crucial factor to global trade are the countries’ ports, operated by companies like Asian Terminals, Inc. (ATI:PHL).

Asian Terminals manages many of the Philippines’ large ports and port terminals such as the Port of Manila’s South Harbor and Port of Batangas. The company provides stevedoring and arrastre services to the vessels.

On one of our Tuesday PMDs, we discussed Asian Terminals’ largest competitor, International Container Terminal (ICT:PHL), and how the competitor has been generating robust returns from its many domestic and foreign terminals.

However, unlike its competitor, Asian Terminals only operates ports in the Philippines and still plans to exclusively expand within the country. Solely depending on one country may sound like a poor strategy, but only if its growth prospects are poor.

For one, as we’ve highlighted in previous Monday Macro reports, the Philippines’ fundamentals remain strong. Though the COVID-19 pandemic is currently crippling trade, a full recovery is still likely once the pandemic ends.

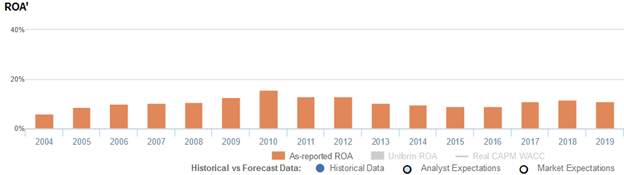

Furthermore, if Asian Terminals’ strategy were indeed inferior, then the company would have displayed historically weak performance. Looking at the firm’s as-reported metrics, this hasn’t been the case.

As-reported ROA has been at least 9% since 2005 and is standing at 11% in 2019.

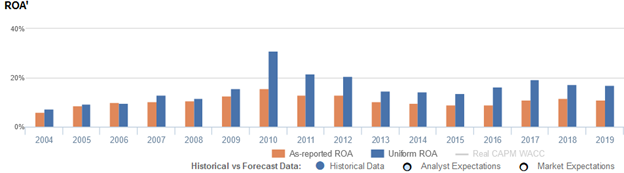

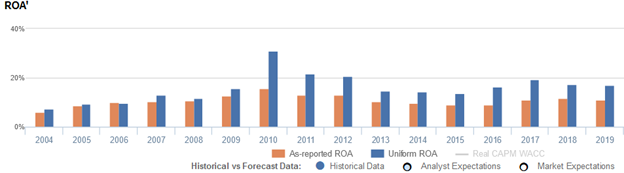

Still, when looking at Asian Terminals’ actual performance under Uniform Accounting, we see even greater profitability than what as-reported metrics suggest. Since 2010, Uniform ROA has been significantly higher, sustaining 17% returns as of 2019.

As-reported metrics understate Asian Terminals’ profitability largely because of how excess cash, among many other accounting distortions, is treated.

Oftentimes, management teams hold way more cash than operationally required, which dilutes the company’s profitability. By removing a firm’s extra cash, we see the firm’s true operating ROA.

Since 2010, Asian Terminals’ extra cash has been 13%-25% of the company’s as-reported assets, with PHP 5.0 billion of excess cash in 2019 specifically.

Removing excess cash from Asian Terminals’ assets, along with the many other necessary adjustments made, leads to a 17% Uniform ROA in 2019, substantially higher than as-reported ROA of 11%.

Asian Terminals’ earning power is stronger than you think

As-reported metrics distort the market’s perception of the firm’s historical profitability. If you were to just look at as-reported ROA, you would think Asian Terminals’ profitability has been weaker than real economic metrics have highlighted in the past thirteen years.

In reality, Asian Terminals’ true profitability has been higher than as-reported ROA since 2007. Specifically, Uniform ROA was 17% in 2019, but as-reported ROA was only 11% that year.

As-reported ROA improved from 6% in 2004 to a high of 16% in 2010, before fading to 9% levels in 2015-2016 and subsequently recovering to 11%-12% levels in 2017-2019.

Meanwhile, after expanding from 7% in 2004 to a peak of 31% in 2010, Uniform ROA fell to 14% levels in 2014-2015. Then, Uniform ROA rebounded to 19% in 2017, before compressing to 17% in 2019.

Asian Terminals’ asset turns are stronger than you think

Strength in Asian Terminals’ Uniform ROA has been driven by strong Uniform asset turns. In fact, Uniform turns have been higher than as-reported turns in each of the past twelve years.

After rising from 0.4x-0.5x levels in 2004-2011 to a high of 0.6x in 2012, as-reported asset turns declined to 0.3x in 2015 and then recovered back to 0.4x-0.5x levels from 2016-2019.

Meanwhile, Uniform turns climbed from 0.4x-0.5x levels in 2004-2009 to a peak of 0.9x in 2012, before dropping to 0.5x levels in 2013-2015 and subsequently rebounding to 0.6x-0.7x levels in 2016-2019.

Looking at the firm’s turns alone, as-reported metrics are making the firm appear to be a less asset efficient business than is accurate.

SUMMARY and Asian Terminals, Inc. Tearsheet

As the Uniform Accounting tearsheet for Asian Terminals, Inc. (ATI:PHL) highlights, the Uniform P/E trades at 9.0x, which is below corporate averages, but around its own history.

Low P/Es require low EPS growth to sustain them. In the case of Asian Terminals, the company has recently shown a 17% Uniform EPS growth.

Sell-side analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, sell-side analysts’ near-term earnings forecasts tend to have relevant information.

We take sell-side forecasts for Philippine Financial Reporting Standards (PFRS) earnings and convert them to Uniform earnings forecasts. When we do this, Asian Terminals’ sell-side analyst-driven forecast calls for a 1% and immaterial Uniform EPS growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Asian Terminals’ PHP 14.60 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 13% each year over the next three years and still justify current valuations. What sell-side analysts expect for Asian Terminals’ earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 3x the long-run corporate average, and cash flows and cash on hand are more than 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Asian Terminals’ Uniform earnings growth is well above peer averages, but the company is trading around peer average valuations.

About the Philippine Market Daily

“Tuesday Uniform Earnings Tearsheets – Philippine-listed Focus”

Some of the world’s greatest investors learned from the Father of Value Investing or have learned to follow his investment philosophy very closely. That pioneer of value investing is Professor Benjamin Graham. His followers:

Warren Buffett and Charles Munger of Berkshire Hathaway; Shelby C. Davis of Davis Funds; Marty Whitman of Third Avenue Value Fund; Jean-Marie Eveillard of First Eagle; Mitch Julis of Canyon Capital; just to name a few.

Each of these great investors studied security analysis and valuation, applying this methodology to manage their multi-billion dollar portfolios. They did this without relying on as-reported numbers.

Uniform Adjusted Financial Reporting Standards (UAFRS or Uniform Accounting) is an answer to the many inconsistencies present in GAAP and IFRS, as well as in PFRS.

Under IFRS, each company’s financial statements are rebuilt under a consistent set of rules, resulting in an apples-to-apples comparison. Resulting UAFRS-based earnings, assets, debts, cash flows from operations, investing, and financing, and other key elements become the basis for more reliable financial statement analysis.

Every Tuesday, we focus on one Philippine-listed company that’s particularly interesting from a UAFRS vs as-reported standpoint. We highlight one adjustment that illustrates why the as-reported numbers are unreliable.

This way, we gain a better understanding of the factors driving a particular stock’s returns, and whether or not the firm’s true profitability is reflected in its current valuations.

Hope you’ve found this week’s Uniform Earnings Tearsheet on a Philippine company interesting and insightful.

Stay tuned for next week’s Philippine company highlight!

Regards,

Angelica Lim

Research Director

Philippine Markets Daily

Powered by Valens Research

www.valens-research.com